Contents

Variety increases complexity 1

1 Introduction 2

2 Overview 8

3 Scope 15

4 Classification of share-based payment

transactions 49

5 Classification of conditions 66

6 Equity-settled share-based payment transactions

with employees 81

7 Cash-settled share-based payment transactions

with employees 144

8 Employee transactions – Choice of settlement 161

9 Modifications and cancellations of employee

share-based payment transactions 177

10 Group share-based payments 208

11 Share-based payment transactions with

non-employees 257

12 Replacement awards in a business combination 268

13 Other application issues in practice 299

14 Transition requirements and unrecognised

share-based payments 317

15 First-time adoption ofIFRS 320

Appendices

I

Key terms 333

II Valuation aspects of accounting for

share-based payments 340

III Table of concordance between IFRS 2 and this

handbook 374

Detailed contents 378

About this publication 385

Keeping in touch 386

Acknowledgements 388

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Variety increases

complexity

In October 2018, the International Accounting Standards Board (the Board)

published the results of its research project on sources of complexity in applying

IFRS 2 Share-based Payment.

The Board concluded that no further amendments to IFRS 2 are needed. It felt the

main issues that have arisen in practice have been addressed and there are no

significant financial reporting problems to address through changing the standard.

However, it did acknowledge that a key source of complexity is the variety

and complexity of terms and conditions included in share-based payment

arrangements, which cannot be solved through amendments to the standard.

Therefore, the core principles of the standard are likely to remain unchanged for the

coming years.

This updated handbook aims to help you apply IFRS 2 in practice and explains

the conclusions that we have reached on many interpretative issues. It’s based

on actual questions that have arisen in practice around the world and includes

illustrative examples and journal entries to elaborate or clarify the practical

application of IFRS 2.

We hope this handbook will help you apply the complex accounting and valuation

requirements of this standard to share-based payment transactions.

Kim Heng

Anthony Voigt

KPMG’s global IFRS employee benefits leadership team

KPMG International Standards Group

2 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1 Introduction

1.1 Background

Historically, the range of specific requirements for the accounting for share-based

payments in national GAAPs has been diverse. Some countries have a relatively

long tradition of accounting for share-based payments. For example, in the US,

APB 25 Accounting for Stock Issued to Employees was issued in 1972, and in

2005 was superseded by ASC Topic 718 Compensation – Stock Compensation

(formerly known as FAS 123(R)). In Canada, HB 3870 Stock-Based Compensation

and Other Stock-Based Payments has been in effect for a number of years and

contains recognition requirements for share-based payment transactions. In

contrast, some countries in the EU still have no requirements for the recognition

and measurement of share-based payment transactions in place for entities not

required to apply IFRS Standards

®

.

IFRS 2.BC29–BC60 Share-based payments were first observed in the 1960s, primarily in the US.

Consequently, the history of international requirements for the accounting for

share-based payments is relatively short compared with other areas of accounting.

The development phase of these requirements internationally was accompanied

by controversial discussions about whether the recognition of cost for share-based

payments that are settled in own equity instruments is justified at all – i.e. whether

such accounting would meet the objectives of financial reporting. Some argued

that transactions settled in equity are transactions between the shareholders and

the third party, rather than between the entity and the third party. Some people

still express concerns about accounting entries that result in a debit to expense

and a credit to equity.

Previously, IAS 19 Employee Benefits contained disclosure requirements for

equity compensation issued to employees, but there were no recognition or

measurement requirements in IFRS for such transactions before the publication

of IFRS 2 Share-based Payment. The first milestone in the development of today’s

standard was in July 2000 when the G4+1, which included the predecessor of

the Board, the International Accounting Standards Committee (IASC), issued a

discussion paper on the topic. The debates resulted in mandatory requirements

for share-based payment transactions – i.e. IFRS 2 – being issued in 2004.

Modifications to address practice issues continue to the date of this publication.

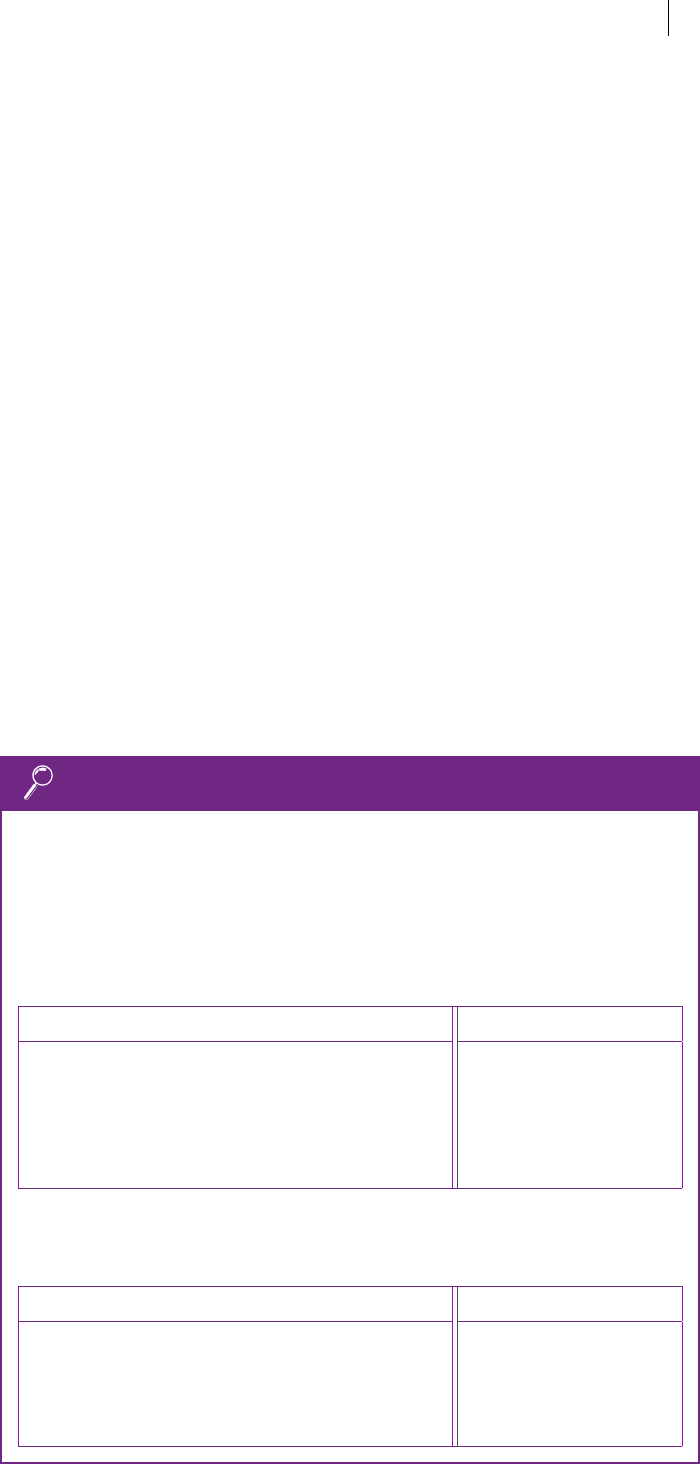

Document

1

Issued

Effective for annual

periods beginning

on or after

Discussion paper Accounting for

Share-based Payment

July 2000

-

Exposure draft ED 2 Share-based

Payment

7 November 2002

-

IFRS 2 Share-based Payment 19 February 2004

1 January 2005

IFRIC 8 Scope of IFRS 2

2

12 January 2006

1 May 2006

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Document

1

Issued

Effective for annual

periods beginning

on or after

IFRIC 11 IFRS 2 – Group and

Treasury Share Transactions

2

2 November 2006

1 March 2007

Amendments Vesting Conditions

and Cancellations

17 January 2008

1 January 2009

Improvements to IFRSs 2009 16 April 2009

1 July 2009

Amendments Group Cash-

settled Share-based Payment

Transactions

18 June 2009

1 January 2010

Amendments within the Annual

Improvements Project 2010

6 May 2010

1 July 2010

Amendments within the Annual

Improvements to IFRSs 2010–

2012 Cycle

12 December 2013

1 July 2014

Amendments Classification and

Measurement of Share-based

Payment Transactions

20 June 2016

1 January 2018

Notes

1. Besides the pronouncements listed in the table, IFRS 2 has been amended as a

consequence of amendments to other standards, principally the revised version of IFRS 3

Business Combinations issued in 2008, which itself was amended by the Improvements

to IFRSs 2010. Other standards, including IFRS 10 Consolidated Financial Statements,

IFRS11 Joint Arrangements and IFRS 13 Fair Value Measurement issued in May 2011, and

IFRS 9 Financial Instruments issued in July 2014, have also made minor consequential

amendments to IFRS 2.

2. IFRIC 8 and IFRIC 11 were withdrawn by the amendments Group Cash-settled Share-

based Payment Transactions issued in June 2009.

IFRIC 8 addressed the issue of whether IFRS 2 applies to share-based payment

transactions in which the entity cannot specifically identify some or all of the

goods or services received. Places where this issue arose included South Africa,

where such payments were being made to historically disadvantaged individuals

as a result of Black Economic Empowerment schemes.

IFRIC 11 addressed the issue of whether transactions in which the entity chooses

or is required to buy equity instruments from another party should be accounted

for as equity-settled or as cash-settled. It further addressed the issue of how

to account for a transaction in the separate or individual financial statements of

a subsidiary, if the equity instruments of the parent are granted either by the

parent or by the subsidiary. For those countries applying IFRS 2 to separate

financial statements of parents and subsidiaries, the interpretation also contained

an important decision by the IFRS Interpretations Committee (formerly the

International Financial Reporting Interpretations Committee (IFRIC)) that recharges

between group entities should not be taken into account in determining the

classification of a share-based payment transaction.

1 Introduction 3

1.1 Background

4 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS 2.64 Both interpretations were withdrawn by the amendments Group Cash-settled

Share-based Payment Transactions, which provided expanded guidance for

group share-based payments, in particular for cash-settled share-based payment

transactions, and incorporated the guidance from IFRIC 8 and IFRIC 11 into IFRS 2.

In December 2004, the Interpretations Committee issued a draft interpretation

D11 Changes in Contributions to Employee Share Purchase Plans, in which it

aimed to resolve the issue of how to account for employee share purchase plans

(ESPPs) when an employee ceases to contribute or changes from one ESPP

to another. An example of transactions in which these issues arose are those

related to the UK’s save as you earn share-based payment scheme, in which

employees invest part of their salary to buy the entity’s shares at a discounted

price. Commentators responded to the Interpretations Committee that the attempt

to interpret IFRS 2 to resolve the issue was unlikely to be successful without

a change in the standard. The Interpretations Committee and the Board agreed

that the standard before those amendments did not address the accounting

for conditions that did not relate to the employee’s service and as a result the

amendments Vesting Conditions and Cancellations were issued early in 2008,

following an exposure draft issued early in 2006. The amendments changed the

definition of vesting conditions and introduced specific accounting requirements

for non-vesting conditions.

Annual Improvements to IFRSs 2010–2012 Cycle clarified the definition of ‘vesting

conditions’ by separately defining a ‘performance condition’ and a ‘vesting

condition’. They also amended the definition of a ‘market condition’ and addressed

circumstances in which an award is conditional on both a service condition and a

specified performance target.

Classification and Measurement of Share-based Payment Transactions –

Amendments to IFRS 2 were issued in relation to certain types of share-based

payment transactions. In particular, the amendments clarified the accounting

for: (a) the effects of vesting and non-vesting conditions on the measurement of

cash-settled share-based payments; (b) share-based payment transactions with a

net settlement feature for withholding tax obligations; and (c) a modification to the

terms and conditions of a share-based payment that changes the classification of

the transaction from cash-settled to equity-settled.

In addition to the matters that the Interpretations Committee has taken on to

its agenda, there have been a number of instances in which it has declined to

take issues related to the accounting for share-based payments on to its agenda

(see the table below). Although these agenda decisions do not form part of the

Board’s authoritative guidance in terms of paragraph 11 of IAS 8 Accounting

Policies, Changes in Accounting Estimates and Errors, they have been influential in

increasing the understanding of IFRS 2.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

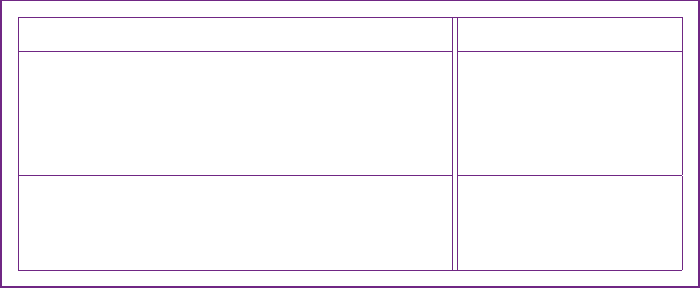

Interpretations Committee’s agenda

decision IFRIC update

Handbook

reference

Employee share loan plans November 2005 6.5.20

Cash alternative not share-based May 2006 3.5.20, 8.2.50

Determining grant date May 2006 6.3.30, 8.2.40

Post-vesting transfer restrictions November 2006 6.6.10

Incremental fair value November 2006 9.2.30

Accounting for employee benefit trusts November 2006 10.6.20

Vesting and non-vesting conditions September 2010 N/A

1

Settlement contingent on future events January 2010 4.6

Share-based payment awards settled

net of tax withholdings

September 2010/

November 2010/

March 2011/

March 2013

2

4.4.40

Modification of a share-based payment

from cash-settled to equity-settled

May 2011/March

2013

2

9.2.30

Accounting for reverse acquisitions that

do not constitute a business

March 2013 3.5.60

Timing of the recognition of inter-

company recharges

May 2013 10.4

Price difference between the

institutional offer price and the retail

offer price for shares in an initial public

offering

July 2014 N/A

Notes

1. The Interpretations Committee recommended the noted vesting and non-vesting

conditions for consideration in a future agenda proposal for IFRS. Theissue was

included in the 2010–12 cycle of annual improvements. A final amendment was issued

in December 2013 and is effective for annual periods beginning on or after 1July 2014

(see5.3.10).

2. In March 2013, the Interpretations Committee had recommended that share-based

payment awards settled net of tax withholdings and modifications of a share-based

payment from cash-settled to equity-settled be taken on by the Board as a narrow-

scope amendment project. Classification and Measurement of Share-based Payment

Transactions – Amendments to IFRS 2, issued in June 2016 and effective for annual

periods beginning on or after 1 January 2018, addressed these issues.

In many respects, the requirements for the accounting for share-based payments

under IFRS 2 are aligned with those of the related US GAAP standard SFAS 123R

Share-Based Payment (ASC 718 Compensation – Stock Compensation).

However, there are still numerous differences, not only in detail but also in basic

requirements. For a description of the more significant differences in requirements

between IFRS 2 and ASC Topic 718, see Chapter 4.5 ‘Share-based payments’ in

our publication IFRS compared to USGAAP.

1 Introduction 5

1.1 Background

6 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Share-based payments, in practice, appear in endless variations and often their

design is influenced by national tax law and/or company law. IFRS 2 is neither

intended nor able to provide detailed guidance for every scenario. However, IFRS 2

is one of the few standards that provide explicit guidance for separate financial

statements.

1.2 Reasons for granting share-based

payments

A ‘share-based payment’ is either a payment in equity instruments of the entity to

the supplier (including employees) of goods or services to the entity; or a payment

in cash or other assets for amounts that are based on the value of the equity

instruments of the entity.

Payments in equity instruments are called ‘equity-settled share-based payments’;

payments in cash or other assets that are based on the value of the equity

instruments of the entity are called ‘cash-settled share-based payments’.

Why does an entity choose to pay in equity instruments or to pay amounts based

on the value of an equity instrument, rather than a fixed cash amount? There are

several reasons, including those set out below.

1.2.10 Principal-agent theory

One of the major reasons for granting share-based payments is based on the

principal-agent theory

1

. This theory focuses on the conflict of interests between

the shareholders (principals) and management or other employees (agents).

According to this theory, the agents pursue not only the interests of the

shareholders (to maximise enterprise value) but also their own interests, which

may not necessarily be the same.

To align the interests of principal and agent, or shareholders and employees

(including management), and to mitigate the conflict, employees are granted

share-based payments as part of their remuneration package. In this way, both the

employees and the shareholders participate in value increases.

Based on the principal-agent theory, share-based payments are often granted to

employees under the condition that the employees provide future services and

that one or more specified service or performance targets are met. Therefore, the

employees are motivated to make an effort to achieve the target in order to benefit

from the share-based payment.

In these cases, the employee becomes unconditionally entitled to the share-based

payment if and when the conditions are met – i.e. if the employee provides their

service to the entity and any performance target is met.

To achieve this alignment of interests, the form of settlement does not matter

because share-based payments settled either in equity instruments or in cash

that is based on the value of the equity instruments have the same motivational

effect. In our experience, whether entities prefer equity-settled or cash-settled

share-based payments may depend on various items, including entity-specific

circumstances (e.g. whether the entity is listed) and jurisdiction-specific

circumstances (e.g. tax deductibility and transferability of shares).

1. See Michael C Jenson and William H Meckling: ‘Theory of the Firm, Managerial Behaviour,

Agency Costs, and Ownership Structure’, in Journal of Financial Economics 3 (October 1976),

pages305–360.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

1.2.20 Reward for past services

Share-based payments are also granted for past services – e.g. to acknowledge

good services of an employee by giving them a participation in the entity (e.g. free

or discounted shares). In this case, the share-based payment would be granted

without the condition to provide future services – i.e. the share-based payment

vests immediately.

1.2.30 Other reasons

Another important reason for granting equity-settled share-based payments is

to receive goods or services without affecting the entity’s liquidity. This form of

remuneration is often found in high-growth industries – e.g. the hi-tech area. It is

also used to preserve cash.

1.3 Key terms and abbreviations

1.3.10 Abbreviations

The following abbreviations are used in this publication.

BSM Black-Scholes-Merton

DCF Discounted cash flows

EBITDA Earnings before interest, tax, depreciation and amortisation

EPS Earnings per share

ESPP Employee share purchase plan

IPO Initial public offering

SARs Share appreciation rights

References in the left-hand column identify the relevant paragraphs of the

standards or other literature (e.g. ‘IFRS 2.IG5’ is paragraph 5 of IFRS 2 illustrative

guidance). References to Interpretations Committee decisions are also indicated

(e.g. ‘IU 11-06’ is IFRIC Update November 2006).

1.3.20 Key terms

IFRS 2 uses numerous technical terms, most of which are defined in Appendix A

of the standard. Please see Appendix I for a list of key terms that are used in

the handbook.

1 Introduction 7

1.3 Key terms and abbreviations

8 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2 Overview

2.1 IFRS 2 at a glance

Handbook

reference

Key points

Chapter

reference

Section 3

– In a share-based payment transaction, an entity

receives goods or services in exchange for

consideration in the form of equity instruments, or

cash or other assets for amounts that are based on

the price (or value) of equity instruments.

– Goods or services received in a share-based

payment transaction are measured at fair value.

Goods are recognised when they are obtained and

services are recognised over the period over which

they are received.

2.2.10

Section 4

– Share-based payments are classified based on

whether the entity’s obligation is to deliver its own

equity instruments (equity-settled) or cash or other

assets (cash-settled).

2.2.20

Section 5

– Conditions that determine whether and/or when

the entity receives the required services are

classified as vesting or non-vesting conditions.

– Vesting conditions are subdivided into service,

market and non-market performance conditions.

– Non-vesting conditions are also subdivided into

several categories.

2.2.30

Section 6

– For equity-settled transactions, an entity recognises

a cost and a corresponding entry in equity.

– Measurement is based on the grant-date fair value

of the equity instruments granted.

– Market and non-vesting conditions are reflected

in the initial measurement of fair value, with no

subsequent true-up for differences between

expected and actual outcome.

– The estimate of the number of equity instruments

for which the service and non-market performance

conditions are expected to be satisfied is revised

during the vesting period such that the cumulative

amount recognised is based on the number of

equity instruments for which the service and non-

market conditions are ultimately satisfied.

2.2.40

Section 7

– For cash-settled transactions, an entity recognises

a cost and a corresponding liability.

– The liability is remeasured, until settlement date,

for subsequent changes in fair value.

2.2.50

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Handbook

reference

Key points

Chapter

reference

Section 8

– Grants in which the counterparty has a choice

of settlement are accounted for as compound

instruments. Grants in which the entity has a

choice of settlement are classified as either equity-

settled share-based payments or cash-settled

share-based payments, depending on the entity’s

ability and intent to settle in shares.

2.2.60

Section 9

– Modification of a share-based payment results in

the recognition of any incremental fair value but

not any reduction in fair value. Replacements are

accounted for as modifications. Cancellation of

a share-based payment results in acceleration of

vesting.

2.2.70

Section 10

– A share-based payment in which the receiving

entity and the settling entity are in the same group

from the perspective of the ultimate parent and

which is settled either by an entity in that group

or by an external shareholder of any entity in that

group is a group share-based payment and is

accounted for as such by both the receiving and

the settling entities.

2.2.80

Section 11

– Equity-settled transactions with non-employees

are generally measured based on the fair value of

the goods or services received.

2.2.90

Section 12

– IFRS 3 Business Combinations provides guidance

about the accounting for replacement of awards

held by the acquiree’s employees.

2.2.100

Section 13

– Accounting for share-based payments can have

interactions with income taxes, EPS calculation,

hedging and events after the reporting period.

2.2.110

Section 14

– There are specific transition requirements for

existing IFRS users.

2.2.120

Section 15

– There are specific transition requirements for first-

time adopters of IFRS.

2.2.120

2 Overview 9

2.1 IFRS 2 at a glance

10 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2.2 General principles

2.2.10 Scope and basic principles

In share-based payment transactions, an entity receives goods or services from a

counterparty and grants equity instruments (equity-settled share-based payment

transactions) or incurs a liability to deliver cash or other assets for amounts that

are based on the price (or value) of equity instruments (cash-settled share-based

payment transactions) as consideration.

The following transactions are not in the scope of IFRS 2:

– transactions with counterparties acting as shareholders rather than as suppliers

of goods or services;

– transactions in which a share-based payment is made in exchange for control of

a business; and

– transactions in which contracts to acquire non-financial items in exchange for a

share-based payment are in the scope of the financial instruments standards.

For further discussion of scope issues, see Section 3.

A ‘counterparty’ can be an employee or any other party (see 2.2.90).

The term ‘equity instrument’ is defined in IFRS 2 without reference to IAS 32

Financial Instruments: Presentation, and it appears that classification under IAS 32

is not relevant (see 3.5.20).

Goods or services received in a share-based payment transaction are measured at

fair value.

Goods are recognised when they are obtained and services are recognised over

the period over which they are received.

2.2.20 Classification of share-based payment transactions

Share-based payment transactions are classified based on whether the entity’s

obligation is to deliver its own equity instruments (equity-settled) or cash or other

assets (cash-settled). An intention or requirement to buy own equity instruments in

order to settle a share-based payment does not affect classification.

Awards requiring settlement in a variable number of equity instruments to a

specified value are classified as equity-settled.

Grants of equity instruments that are redeemable mandatorily or at the

counterparty’s option are classified as cash-settled, without consideration of intent

or probability. Grants of equity instruments that are redeemable at the entity’s

option are classified based on the entity’s intent and past practice of settling in

shares or cash.

For further discussion of classification of share-based payment transactions as

either equity-settled or cash-settled, see Section4.

2.2.30 Classification of conditions

Share-based payment transactions, in particular those with employees, are often

conditional on the achievement of conditions. IFRS 2 distinguishes between

vesting conditions and non-vesting conditions as follows.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Vesting

condition

A condition that determines whether an entity receives services that entitle

the counterparty to receive cash, other assets or equity instruments of the

entity. A vesting condition is either a service condition or a performance

condition.

Service condition Performance condition

Vesting condition that requires

the counterparty to complete a

specified period of service during

which services are provided to the

entity.

If the counterparty, regardless

of the reason, ceases to provide

services during the vesting period,

then it has failed to satisfy the

condition.

The service requirement can be

explicit or implicit.

Vesting condition that requires

the counterparty to complete

a specified period of service

and specified performance

target(s) to be met while services

arerendered.

A performance target can be one

of the following conditions.

– Market condition: If it is based

on the price (or value) of the

entity’s equity instruments –

e.g. achieving a certain share

price target.

– Non-market performance

condition: If it is based on the

entity’s operations or activities

– e.g. achieving a certain profit

target.

Non-

vesting

condition

A condition other than a vesting condition that determines whether a

counterparty receives the share-based payment – e.g. counterparty’s

choice of participation in a share purchase programme by paying monthly

contributions.

For further discussion of classification of conditions, see Section 5.

2.2.40 Equity-settled share-based payments with employees

Equity-settled share-based payment transactions with employees require indirect

measurement and each equity instrument granted is measured on its grant date.

The impacts of any market conditions and non-vesting conditions are reflected

in the grant-date fair value of each equity instrument. Any service or non-market

performance condition is not reflected in the grant-date fair value of the share-

based payment. Instead, an estimate is made of the number of equity instruments

for which the service and non-market performance conditions are expected to

be satisfied. The product of this estimate – i.e. grant-date fair value per equity

instrument multiplied by the number of equity instruments for which the service

and non-market performance conditions are expected to be satisfied – is the

estimate of the total share-based payment cost. This cost is recognised over the

vesting period, with a corresponding entry in equity. The cost is recognised as an

expense or capitalised as an asset if the general asset-recognition criteria in IFRS

are met. If the payment is not subject to a service condition, then it is recognised

immediately.

2 Overview 11

2.2 General principles

12 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Subsequent to initial recognition and measurement, the estimate of the number of

equity instruments for which the service and non-market performance conditions

are expected to be satisfied is revised during the vesting period. The cumulative

amount recognised at each reporting date is based on the number of equity

instruments for which the service and non-market performance conditions are

expected to be satisfied. Ultimately, the share-based payment cost is based on

the number of equity instruments for which these conditions are satisfied. No

adjustments are made in respect of market conditions – i.e. neither the number of

instruments nor the grant-date fair value is adjusted if the outcome of the market

condition differs from the initial estimate.

Subsequent to initial recognition and measurement, the manner of adjustment for

non-vesting conditions depends on whether there is choice within the condition.

Failure to satisfy the following conditions results in accelerated recognition of

unrecognised cost:

– non-vesting conditions that the counterparty can choose to meet: e.g. paying

contributions towards the purchase (or exercise) price on a monthly basis, or

complying with transfer restrictions; and

– non-vesting conditions that the entity can choose to meet: e.g. continuing the

plan.

A non-vesting condition that neither the entity nor the counterparty can choose to

meet (e.g. a target based on a commodity index) has no impact on the accounting

if it is not met – i.e. there is neither a reversal of the previously recognised cost nor

an acceleration of recognition.

For further discussion on accounting for equity-settled share-based payments, see

Section 6.

2.2.50 Cash-settled share-based payments with employees

Cash-settled share-based payment transactions are measured initially at the fair

value of the liability and are recognised as an expense or capitalised as an asset if

the general asset recognition criteria in IFRS are met. If the payment is subject to

a vesting condition, then the amounts are recognised over the vesting period. At

each reporting date until settlement date, the recognised liability is remeasured at

fair value with changes recognised in profit or loss. Remeasurements during the

vesting period are only recognised to the extent that services have been received

– e.g. on a time-proportionate basis. If the payment is not subject to a vesting

condition, then it is recognised immediately. For further details, see Section 7.

2.2.60 Employee transactions with a choice of settlement

Some share-based payment transactions provide one party with the choice

of settlement in cash or in equity instruments. If the entity has the choice of

settlement, then the transaction is classified as an equity-settled or a cash-

settled share-based payment transaction, depending on whether the entity has a

present obligation to settle in cash. A ‘present obligation to settle in cash’ exists,

for example, if the entity has a past practice or a stated policy of settling in cash.

If the counterparty has the choice of settlement, then the entity has granted a

compound instrument comprising a debt component and an equity component.

For further details, see Section 8.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

2.2.70 Modifications and cancellations of employee transactions

Modifications of an equity-settled share-based payment arrangement are

accounted for only if they are beneficial. If the fair value of the equity instruments

granted has increased as a result of a modification to their terms and conditions,

then the incremental fair value at the date of modification is recognised in

addition to the grant-date fair value. Modifications that are not beneficial to

the counterparty do not affect the amount of the share-based payment cost

recognised. However, reductions in the number of equity instruments granted are

accounted for as cancellations.

Cancellations by the entity or by the counterparty are treated as an acceleration

of vesting, requiring any unamortised compensation cost to be recognised

immediately. If an entity grants new equity instruments to replace cancelled equity

instruments, then this cancellation and replacement may be accounted for in the

same way as a modification.

For further discussion on modifications and cancellations of employee

transactions, see Section 9.

2.2.80 Group share-based payments

A share-based payment in which the receiving entity, the settling entity and the

reference entity are in the same group from the perspective of the ultimate parent

is a group share-based payment transaction from the perspective of both the

receiving and the settling entities. In a group share-based payment transaction in

which the parent grants a share-based payment to the employees of its subsidiary,

the share-based payment is recognised in the consolidated financial statements

of the parent, in the separate financial statements of the parent and in the

financial statements of the subsidiary. Recharge arrangements do not affect the

classification of the share-based payment arrangement, but may be accounted for

by analogy to share-based payments. For further details, see Section 10.

2.2.90 Share-based payments with non-employees

Equity-settled share-based payment transactions with non-employees are generally

measured at the fair value of the goods or services received (direct measurement),

rather than at the fair value of the equity instruments granted at the time when

the goods or services are received. If in rare cases the fair value of the goods

or services received cannot be measured reliably, then the goods or services

received are measured with reference to the fair value of the equity instruments

granted (indirect measurement). For further details, see Section 11.

2.2.100 Replacement awards in a business combination

IFRS 3 provides guidance about the accounting for replacements of awards held by

the acquiree’s employees (acquiree awards) in a business combination when the

acquirer:

– is obliged to issue share-based payment replacement awards (replacement

awards); or

– chooses to replace awards that expire as a result of the business combination.

To the extent that the replacement awards relate to past service, they are included

in the consideration transferred; to the extent that they require future service,

they are not part of the consideration transferred and instead are treated as post-

combination remuneration cost. If they relate to both past and future service,

then the market-based measure (see Chapter 12.1) of the replacement awards is

allocated between consideration transferred and post-combination cost.

2 Overview 13

2.2 General principles

14 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS 3 also includes guidance for equity-settled acquiree awards that the acquirer

chooses not to replace (unreplaced awards). Such unreplaced awards are part of

the non-controlling interests in the acquiree at the date of acquisition.

For further discussion of replacement awards in a business combination, see

Section 12.

2.2.110 Other application issues

The interaction between IFRS 2 and other standards can be difficult. The

interaction with some of those standards – e.g. IFRS 3 – is addressed in IFRS 2.

Some aspects of the interactions with IFRS 3 are covered in Section12. However,

there are some other standards that are not addressed specifically in IFRS 2 but

which raise questions on the interaction with IFRS 2. These include IAS 12 Income

Taxes

, IAS 33 Earnings per Share and IAS 10 Events after the Reporting Period. The

issue of whether hedge accounting can be applied is also a common question.

For further guidance on some common issues arising in practice, see Section 13.

2.2.120 Transition requirements, unrecognised share-based payments

and first-time adoption of IFRS

IFRS 2 has been effective since 1 January 2005. For a discussion of the general

transition requirements, see Section 14; and for a discussion of the transition

requirements for first-time adopters of IFRS, see Section15.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3 Scope

Overview

– In a share-based payment transaction, an entity receives goods or services

in exchange for consideration in equity instruments or in cash or other assets

for amounts that are based on the price (or value) of equity instruments.

– If the fair value of the identifiable goods or services received appears to be

less than the fair value of the share-based payment, then circumstances may

indicate that unidentifiable goods or services have been received.

– Except in group arrangements, share-based payments are either in the form

of equity instruments of the entity or in cash or other assets for amounts that

are based on the price (or value) of the equity instruments of the entity.

– Certain group arrangements in which either another group entity or a

shareholder of a group entity is involved are also considered share-based

payment transactions (see Section10).

– Equity instruments are defined in IFRS 2; the definition may be different from

classification as equity under IAS 32 Financial Instruments: Presentation.

– The following transactions are not in the scope of IFRS 2:

- transactions with counterparties acting as shareholders rather than as

suppliers of goods or services;

- transactions in which a share-based payment is made in exchange for

control of a business; and

- share-based payment transactions in which the entity receives or

acquires goods or services under a contract within the scope of financial

instruments standards.

3 Scope | 15

16 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.1 Definition of a share-based payment

IFRS 2.2 A share-based payment is accounted for under IFRS 2 if it meets the definition of

a share-based payment transaction and the transaction is not specifically scoped

out of the standard. For transactions that are outside the scope of IFRS 2, see

Chapter3.4.

IFRS 2.A The standard does not contain a stand-alone definition of a share-based payment

but provides a complex two-step definition using the terms ‘share-based

payment arrangement’ and ‘share-based payment transaction’. The definitions are

as follows.

A ‘share-based payment arrangement’ is an agreement between the entity (or

another group entity or any shareholder of any group entity) and another party,

including an employee, that entitles the other party to receive:

a.

cash or other assets of the entity for amounts that are based on the price

(or value) of equity instruments (including shares or share options) of the

entity or another group entity; or

b. equity instruments (including shares or share options) of the entity or

another group entity, provided that the specified vesting conditions are

met.

A ‘share-based payment transaction’ is a transaction in which the entity:

a. receives goods or services from the supplier of those goods or services,

including an employee, in a share-based payment arrangement; or

b. incurs an obligation to settle the transaction with the supplier in a share-

based payment arrangement when another group entity receives those

goods or services.

IFRS 2.A, 10.A In defining a share-based payment arrangement, a ‘group’ is defined as a parent

and its subsidiaries as set out in IFRS 10 Consolidated Financial Statements. This

determination is made from the perspective of the reporting entity’s ultimate

parent. The requirement to treat transactions involving instruments of another

entity as share-based payments applies only to transactions involving equity

instruments of a group entity (see 10.1.30).

IFRS 2.3A These definitions are complex because they include not only share-based

payments that involve the reporting entity and the supplier, but also those that

involve other group entities or shareholders. This handbook distinguishes between

the following types of share-based payment transactions:

1. share-based payment transactions that involve only the supplier of goods or

services and the reporting entity – i.e. the reporting entity receives the goods or

services and settles the transaction in its own equity instruments or in a payment

based on its own equity instruments; and

2. share-based payment transactions that involve the supplier, the reporting entity

and at least one other group entity or a shareholder of any group entity (group

share-based payment transactions).

Scope issues for the first type of share-based payment transactions are illustrated

in this section; additional scope issues that arise in group share-based payment

transactions are discussed in Chapter10.1.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

For a discussion of the basic features of a share-based payment, see Chapter 3.3,

and for a consideration of the various scope exceptions see Chapter3.4. For the

application of the definitions and exceptions in practice, see Chapter 3.5.

3.2 Determining whether transaction is share-

based payment transaction in scope of

IFRS 2

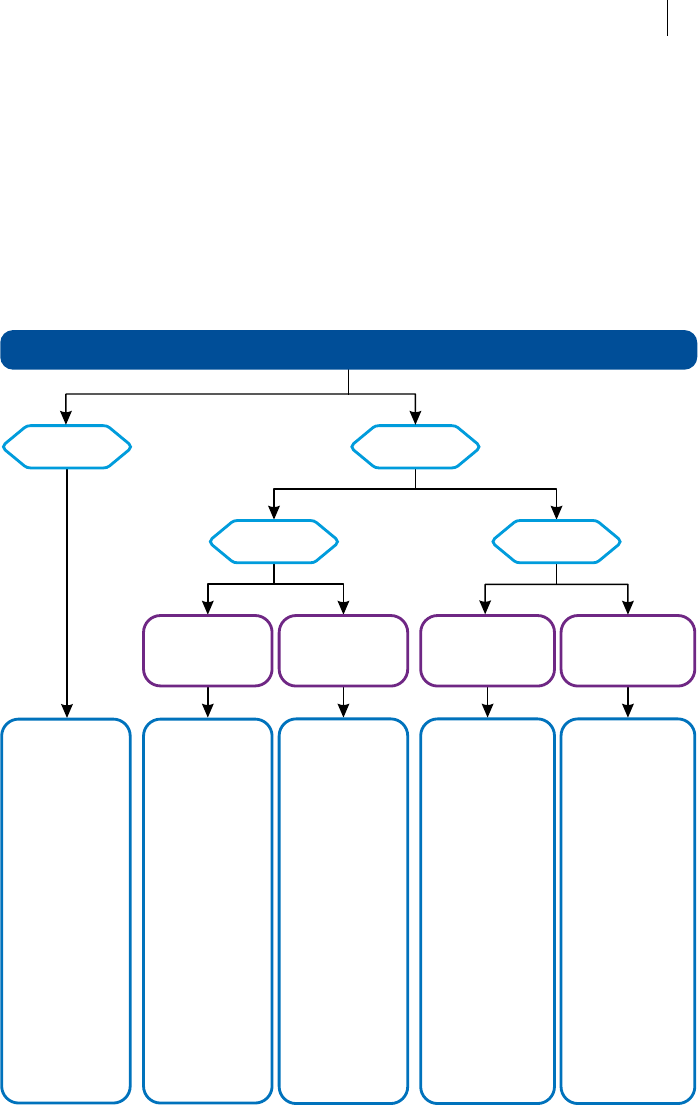

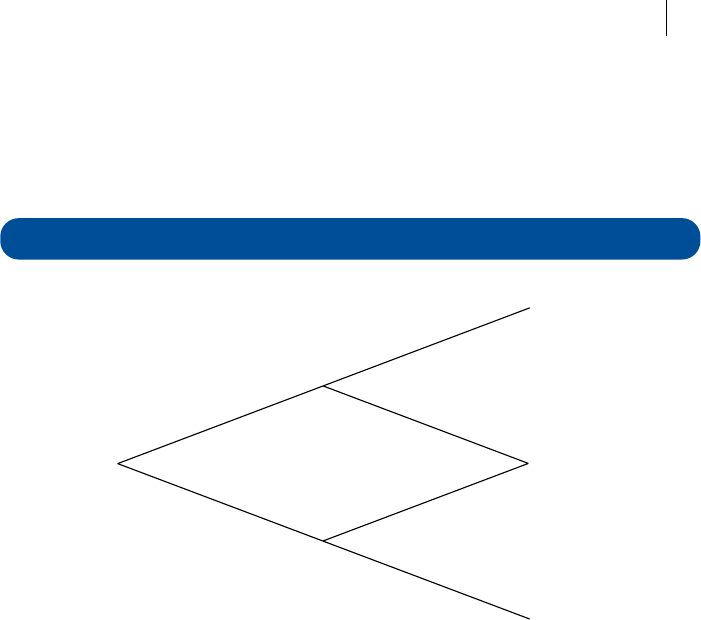

The following flowchart illustrates the steps to analyse whether a transaction is

a share-based payment transaction in the scope of IFRS 2. This analysis covers

transactions that involve only the supplier of goods and services and the reporting

entity – i.e. the reporting entity receives the goods or services and settles the

transaction in its own equity instruments or a payment based on its own equity

instruments. The reporting entity can be a group or a separate legal entity. Scope

issues in group arrangements are discussed in Chapter 10.1.

No

Ye s

Ye s

Does the counterparty act in its

capacity as a shareholder?

(See )3.4.20

No

No

Ye s

Ye s

No

The transaction is a

share-based payment transaction

in the scope of IFRS 2.

The transaction is not a

share-based payment transaction

in the scope of IFRS 2.

No

No

Ye s

Ye s

Does the reporting entity

receive identifiable

goods or services?

(See )3.3.20

Do circumstances indicate

that the reporting entity receives

unidentifiable goods or services?

(See )3.3.20

Is the consideration ‘share-

based’– i.e. either in equity

instruments of the reporting entity

or in a payment in cash or other

assets based on such equity

instruments? (See )3.3.30

Does the transaction meet the

definition of a business combination?

(See )3.4.30

Are the goods or services

acquired in a contract that is

accounted for as a financial

instrument? (See )3.4.40

3 Scope 17

3.2 Determining whether transaction is share-based payment transaction in scope of IFRS 2

18 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

If a transaction is a share-based payment transaction in the scope of IFRS 2,

then the next step is to determine the classification of the transaction as either

equity-settled, cash-settled or a transaction in which one party has the choice

of settlement (see Section 4). Further steps include determining whether the

counterparty is an employee or a non-employee (see Chapter 11.1).

If a transaction is in the scope of IFRS 2, then the requirements of the standard

specify both the initial and the subsequent accounting for the equity instruments

issued or liability incurred, including requirements for planned and unplanned

repurchases of vested shares. For the impact of the intent to repurchase on the

classification of a share-based payment, see 4.5.30 and for accounting for the

repurchase of a share-based payment see 9.3.20.

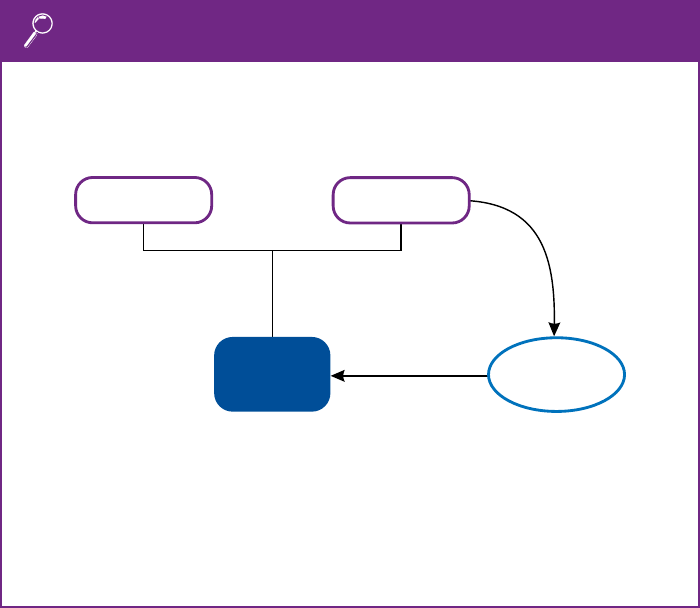

Sometimes arrangements involve entities that are outside the reporting entity.

Service

90%

100%

100%

10%

Ultimate Parent UP

Parent P

SubsidiaryS

E

(Subsidiary of S)

Employees

Non-controlling

shareholder

In this diagram, if Subsidiary S is the reporting entity and Parent P grants its own

equity instruments to the employees of S or if S grants equity instruments of P to

its own employees, then from the perspective of S’s financial statements this is a

share-based payment arrangement involving an entity outside the reporting entity.

This is because P is not part of the reporting entity when S prepares its financial

statements. Share-based payment arrangements that involve entities outside the

reporting entity are referred to as ‘group share-based payment arrangements’ if

the other entity is, from the perspective of Ultimate Parent UP, in the same group

as the reporting entity. For guidance on these arrangements, see Section 10.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.3 Basic features of share-based payment

transactions

3.3.10 Introduction

This chapter addresses only scope issues that arise in share-based payment

transactions that do not involve other group entities or shareholders. Therefore, all

transactions discussed in this chapter can be described as follows.

A transaction in which the entity receives goods or services in an arrangement

that entitles the supplier to receive equity instruments of the entity, or cash or

other assets of the entity, for amounts that are based on the price (or value) of

equity instruments of the entity.

Reporting

entity

or

Supplier of goods

or services

Own equity instruments

Payment in cash or

other assets based on

price (or value) of own

equity instruments

Goods or services

3.3.20 Goods or services

Definition of goods or services

The most common goods or services received in exchange for a share-based

payment are employee services. However, services received can be provided by

parties other than employees – e.g. consultancy services. For a discussion of the

definition of employees, see Chapter 11.1.

IFRS 2.5 Goods can include inventories, consumables, property, plant and equipment,

intangible assets and other non-financial assets.

Identification of goods or services

IFRS 2.14–15 Goods or services may be either received when a share-based payment is granted

or expected to be received in the future.

IFRS 2.2, 13A, BC18A–BC18D, IG5A–IG5D An entity may grant a share-based payment without any specifically identifiable

goods or services being received in return. In the absence of specifically

identifiable goods or services, other circumstances may indicate that goods or

services have been received or will be received (see 11.2.40).

IFRS 2.IG5D.Ex1 An example in which no goods or services are identifiable but unidentifiable goods

or services are received are many share-based payments made to historically

disadvantaged individuals under South Africa’s Black Economic Empowerment

(BEE) initiative.

3 Scope 19

3.3 Basic features of share-based payment transactions

20 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 3.3.1 – Unidentifiable goods or services in a share-based

payment under a South African BEE scheme

In response to the BEE government policy, Company S, a South African

company, transfers shares to Company B, which is owned by historically

disadvantaged individuals. The shares are issued for zero consideration.

S cannot identify any specific goods or services received in consideration for

this transfer because B is not required to do anything in return for the shares.

However, by meeting certain requirements of the BEE policy, S will benefit by

improving its ability to tender for government contracts. IFRS 2 illustrates that

these benefits represent unidentifiable goods or services received in exchange

for the share-based payment and bring the arrangement into the scope of

IFRS 2.

IFRS 2.13A In other cases, there may be specifically identifiable goods or services received in

exchange for the share-based payment. If the identifiable consideration received

appears to be less than the fair value of the equity instruments granted or liability

incurred, then typically this indicates that other consideration (i.e. unidentifiable

goods or services) has also been (or will be) received (see 11.2.40). This issue

is relevant in share-based payment transactions with non-employees when the

goods or services are measured directly at their fair value.

Goods or services from a supplier

IFRS 2.4 The goods or services received or to be received by the entity need to be provided

by the counterparty in its capacity as a supplier of goods or services. If the goods

or services are provided by a counterparty in its capacity as a shareholder, then the

transaction is not a share-based payment transaction (see 3.5.10).

3.3.30 Consideration in form of share-based payment

IFRS 2.A In its basic form, a share-based payment transaction requires the entity to settle

the transaction by either transferring its own equity instruments or making a

payment in cash or other assets for amounts that are based on the price (or value)

of its equity instruments.

IFRS 2.A Depending on the type of consideration to be paid, the payment is referred to as

either an equity-settled or a cash-settled share-based payment (see Section4).

Before classification is considered, it is necessary to consider what constitutes an

equity instrument under IFRS 2 in order to decide if a transaction is in the scope of

the standard.

Definition of equity instruments

IFRS 2.A An ‘equity instrument’ is a contract that evidences a residual interest in the assets

of an entity after deducting all of its liabilities. The most common examples of

equity instruments used for share-based payments are ordinary shares and written

call options, or warrants issued over ordinary shares (share options). An equity

instrument for the purposes of IFRS 2 can include redeemable shares.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

A share-based payment might involve granting preference shares or shares of one

class of ordinary shares in circumstances in which there is more than one class of

ordinary shares. In both of these cases, the instrument granted may be a right to a

residual interest in an entity and therefore be equity.

IFRS 2.31, BC106–BC110, IAS 32.15, IFRIC 2 Although in most cases it will be clear whether an instrument meets the IFRS 2

definition of an equity instrument, in some cases this determination may require

further consideration, because the instrument might be classified differently under

IAS 32. Under IAS 32, some instruments issued in the legal form of shares may be

classified as liabilities. However, these instruments might still be considered to be

equity instruments in the context of a share-based payment. For example, IFRS 2

demonstrates that a grant of a redeemable equity instrument is viewed as a

payment based on an equity instrument and in the scope of the standard, although

the redeemable equity instrument would in some cases be classified as a financial

liability under IAS 32. For a more detailed discussion of this issue, see 3.5.20.

Equity instruments of the entity

IFRS 2.A The basic definition of a share-based payment arrangement refers to equity

instruments of the entity (see Chapter 3.1).

IFRS 2.B50, 10.A What constitutes an equity instrument ‘of the entity’ is an issue of particular

interest in consolidated financial statements. In the consolidated financial

statements, equity instruments of the entity comprise the equity instruments of

any entity that is included in the group – i.e. the parent and its subsidiaries.

Basis of cash payments

IFRS 2.A If the entity does not settle in its own equity instruments but in a payment of

cash or other assets, then the amount is a share-based payment if it is based on

the price (or value) of its equity instruments (or the equity instruments of another

entity in the same group).

IFRS 2.IG19 A common example of a cash payment based on the price (or value) of an equity

instrument of the entity is when an entity grants SARs. SARs entitle the holder

to receive a cash payment that equals the increase in value of the shares from a

specified level over a specified period of time – e.g. from grant date to settlement

date. In this case, the counterparty directly participates in changes of the value

of the underlying equity instrument and, accordingly, the cash payment is based

on the price (or value) of the equity instrument. Another common example of a

cash-settled share-based payment is a payment based on the value of an equity

instrument at a specific date – e.g. vesting date or settlement date – rather than on

the increase in value.

Sometimes it is difficult to assess whether the cash payment is based on the price

or value of the equity instrument. For a more detailed discussion of the distinction

between a cash payment that ‘depends on’ vs one that ‘is based on’ the price or

value of the equity instrument, see 3.5.20.

3 Scope 21

3.3 Basic features of share-based payment transactions

22 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

The following are basic scope examples that illustrate the analysis of the basic

features of share-based payments in determining whether a transaction is in the

scope of IFRS 2.

Scenario

In or out

of scope

of IFRS2? Rationale

Entity B grants 10 shares to its

employees provided that they remain

in service for the next 12 months.

In This is an equity-settled share-

based payment. The employees

will receive the shares of B if they

provide the required period of

service to the entity.

Entity C grants employees a cash

bonus equal to C’s share price

growth provided that they remain in

service over the next 12 months.

In This is a cash-settled share-based

payment. C has an obligation to pay

cash based on the change in share

price to the employees who provide

the required service; this award is

also known as an SAR.

Entity E’s share price is 120. E

awards a cash bonus of 120 to

employees, payable in one year to

those who remain in service during

the next 12 months.

Out This is not a share-based payment.

Although the payment to the

employees is linked to the delivery

of service from the employees, the

payment is not based on the share

price of E. For example, if the share

price increases or decreases over

the period, the employees would

still receive the 120. The award is

considered an employee benefit

in the scope of IAS 19 Employee

Benefits.

Entity D awards a cash bonus of 500

to employees, payable in one year to

those who remain in service if D’s

share price exceeds a price of 10 per

share during the next 12months.

Out This is not a share-based payment.

Although D has an obligation if the

share price-related target is met

and the employees provide the

required services, the amount of the

payment is not based on the share

price of D. The award is considered

an employee benefit in the scope of

IAS19.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.4 Transactions outside scope of IFRS 2

3.4.10 Introduction

IFRS 2.4–6 The following transactions are not share-based payment transactions in the scope

of IFRS 2:

1. the counterparty acts in its capacity as a shareholder (see 3.4.20);

2. the reporting entity issues a share-based payment as consideration for the

acquisition of a business (see 3.4.30); and

3. the reporting entity issues a share-based payment as consideration for a contract

to acquire a non-financial item that is in the scope of the financial instruments

standards (see 3.4.40).

Transactions under (1) do not meet the definition of a share-based payment

transaction. Transactions under (2) and (3) do meet the definition of a share-based

payment transaction, but are excluded from the scope of IFRS 2 by specific scope

exceptions.

3.4.20 Counterparty acts in its capacity as shareholder

IFRS 2.4 Transactions with employees or other parties in their capacity as shareholders are

outside the scope of IFRS 2.

IFRS 2.4 If employees or other parties who are also shareholders participate in a transaction

with the entity, then it may be difficult to determine in which capacity they act: as

suppliers of goods or services to the entity or as shareholders of the entity. If all

shareholders have been offered the right to participate in a transaction, then this is

an indication that the employees or other parties do not act as suppliers of goods

or services but as shareholders.

IFRS 2.5–6 Transactions in which equity instruments of an entity are issued in return for

financial instruments of equal fair value are outside the scope of IFRS 2.

Example 3.4.1 – Shares at a discount/shareholder acts as an

employee

As a reward for past services, Company B offers to sell shares at a discount of

10% of their market price to all of its employees, but not to shareholders who

are not employees. There are no conditions attached to the shares other than

paying the subscription price. Employee E, who is a shareholder of B, purchases

such a share.

In this example, E is acting in its capacity as an employee, because the shares

are not offered to all of B’s shareholders, but only to B’s employees. This

transaction is in the scope of IFRS 2, because the share discount is granted to

the employee in return for services.

3 Scope 23

3.4 Transactions outside scope of IFRS 2

24 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Example 3.4.2 – Shares at a discount/employee acts as a

shareholder

Company C makes a rights issue to all of its shareholders in which shares are

offered at a discount of 10% of their market price. There are no conditions attached

to the shares other than paying the subscription price. Employee E, who is a

shareholder of C, purchases such a share.

In contrast to Example 3.4.1, in this example E is not acting as an employee

but as a shareholder. This is because the benefit of the discount is offered to all

of C’s shareholders. Therefore, the transaction is not a share-based payment

transaction in the scope of IFRS 2.

3.4.30 Acquisition of a business

IFRS 2.5 The following paragraphs illustrate the scope exception in IFRS 2 that addresses

share-based payment transactions in which a business is acquired: in a business

combination between third parties; in a transaction between entities under

common control; and on the formation of a joint venture.

Business combinations between third parties

IFRS 2.5, BC23–BC24D, 3.A Share-based payment transactions in which the entity acquires net assets in a

business combination as defined in IFRS 3 Business Combinations are outside

the scope of IFRS 2. This is because IFRS 3, which applies to the issue of shares

in connection with a business combination, is the specific standard applicable to

such transactions.

Example 3.4.3 – Own shares in exchange for control (business

combination)

Company B

(reporting entity)

CompanyT

(target)

Company S

(supplier)

Own shares

Shares in T

Company B acquires a controlling interest in Company T from Company S by

delivering its own shares in exchange for shares in T.

T meets the definition of a

business and B controls T from that point forward.

In this example, because the shares are issued in a business combination in

exchange for control of the acquiree (T), the transaction is not in the scope of

IFRS 2 but is instead in the scope of IFRS 3.

The conclusion would be the same if, instead of B acquiring all of the shares

of T, B acquired all of the net assets of T constituting the business in return for

delivering B’s own shares to S.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

IFRS 2.5, 3.52(b) In a business combination, equity instruments are often issued to the previous

owners of the acquiree in exchange for control. If equity instruments are issued

to previous owners of the acquiree who are also employees of the combined

entity, then a question arises about whether the transaction with the employees

is in exchange for control or in exchange for continued employee services. If the

shares issued are part of the consideration transferred in exchange for control,

then they will be accounted for under IFRS 3. To the extent that the shares issued

are granted to the employees in their capacity as employees – i.e. for continuing

services – they are accounted for under IFRS 2. For further guidance on this issue,

see Section 12.

Business combinations under common control

IFRS 2.5 IFRS 2’s scope excludes all business combination transactions, whether or not

those transactions are in the scope of IFRS 3.

Example 3.4.4 – Combination of entities under common control

Shares in T

CompanyT

(target)

Own shares

Ultimate Parent

UP

Company S2

(reporting entity)

Company S1

(supplier)

Company S2 acquires a controlling interest in Company T from Company S1,

by delivering its own shares in exchange for shares of T. S1 and S2 are both

subsidiaries of Ultimate Parent UP – i.e. they are under common control. T

meets the definition of a business.

IFRS 2.5 Because both T and S2 are ultimately controlled by UP both before and after the

business combination, the transaction is neither in the scope of IFRS 2 nor in

the scope of IFRS 3.

3 Scope 25

3.4 Transactions outside scope of IFRS 2

26 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

Contribution of business on formation of joint venture

IFRS 2.5, BC24A–BC24D, 3.2(a) A transaction in which an investor contributes a business as part of the formation

of a joint venture in the scope of IFRS 11 Joint Arrangements in return for shares in

an entity is not in the scope of IFRS 2. Like business combinations under common

control, these transactions are excluded from the scope of IFRS 3 and they are

also outside the scope of IFRS 2.

Example 3.4.5 – Contribution of a business on the formation of a

joint venture

Investor P1

Joint VentureJV

(reporting entity)

Sinhares JV

Business

Investor P2

Joint Venture JV, the reporting entity, is a joint venture of Investor P1 and

Investor P2. On its formation, JV issues shares to P1 as consideration for the

contribution of a business.

Because the shares are issued as consideration for a business contributed on

the formation of a joint venture, the transaction is not a share-based payment

transaction in the scope of IFRS 2 from the perspective of JV.

If, instead, the net assets contributed by an investor do not constitute a business,

then the scope exception in IFRS 2 does not apply. As a result, such transactions

are in the scope of IFRS 2.

Other transactions outside the scope of IFRS 2

In our view, the exclusion from IFRS 2 for business combinations extends beyond

business combination transactions as defined in IFRS 3, and we believe that the

following transactions are also outside the scope of IFRS 2:

– acquisition of non-controlling interests after control is obtained, because IFRS 10

is generally the specific standard applicable to the transaction;

– acquisition of associates, because IAS 28 Investments in Associates and Joint

Ventures is the specific standard applicable to the transaction; and

– acquisition of a joint controlling interest in a joint venture, because IAS 28 is the

specific standard applicable to the transaction.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.4.40 Commodity contracts

IFRS 2.6, BC25–BC28, 9.2.4 IFRS 2 includes a scope exception for contracts to acquire non-financial items

that are in the scope of the financial instruments standards. Under the financial

instruments standards, contracts to acquire non-financial items are required to be

accounted for as financial instruments in some circumstances even if the contract

is settled with a share-based payment. These contracts include those that fall

directly in the scope of IFRS 9 Financial Instruments and those that meet the own-

use exemption but are designated as at fair value through profit or loss. For a more

detailed discussion of this issue, see Chapter 7.1 of the 15th Edition 2018/19 of our

publication Insights intoIFRS.

Example 3.4.6 – Commodity contracts for own use

On 23 July Year 1, Company B purchases 100 tonnes of cocoa beans in

exchange for 100 shares of B. Both delivery and exchange will occur on

28 February

Year 2. As a chocolate producer, B enters into the contract for the

purpose of receiving delivery in order to process the cocoa beans; its purpose

does not change and ultimately B receives the cocoa beans for its own use.

B expects to receive the delivery for its own use, so the contract is not in the

scope of IFRS 9 (unless it is designated as at fair value through profit or loss)

and therefore the scope exception in IFRS 2 does not apply. Therefore, the

transaction is in the scope of IFRS 2, because B receives goods (i.e. cocoa

beans) in exchange for a share-based payment.

Conversely, if B’s purpose in entering into the contract were not for its own

use (e.g. B intends to resell the cocoa beans to earn a dealer’s profit), then the

transaction would be accounted for under IFRS 9 and the scope exception in

paragraph 6 of IFRS 2 would apply.

3.4.50 Share-based payments that are not payments for goods or

services

IFRS 2.3A, BC22 IFRS 2 excludes from its scope those transactions that are clearly for a purpose

other than payment for goods or services supplied to the entity receiving them.

In our view, the requirement for the transfer of, or a cash payment based on,

equity instruments for another purpose is a high threshold. We believe that any

requirement for continued employment should be considered persuasive evidence

that transfers of, or cash payments based on, equity instruments to employees

are not clearly for another purpose and are share-based payments in the scope

of IFRS 2.

Example 3.4.7 – Grants by a shareholder clearly for a purpose other

than payment for goods or services supplied to the entity

Company B has a shareholder S. S transfers 100 shares in B to his child,

who is employed by B, as part of S’s advance planning for inheritance of S’s

investments. There are no service or other conditions attached to the grant.

The share grant is not classified as a share-based payment transaction in

the scope of IFRS 2 from B’s perspective because the grant of shares is not

consideration for services supplied to the entity. The transfer would have taken

place irrespective of whether S’s child was employed by B.

3 Scope 27

3.4 Transactions outside scope of IFRS 2

28 | Share-based payments – IFRS 2 handbook

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

3.5 Scope issues in practice

3.5.10 Share-based payment vs shareholder transaction

In some transactions, it will be clear that the counterparties are acting in their

capacity as shareholders. An example is when the entity grants all existing

shareholders of a particular class of equity instruments the right to acquire

additional equity instruments at a discount (see Example3.4.2).

IFRS 2.4 IFRS 2 does not limit situations in which the counterparty acts in its capacity as a

shareholder to transactions in which all existing shareholders are granted the same

rights and restrictions. In particular, if the counterparty buys the equity instruments

at fair value, then it can appear as if the counterparty has paid the same amount

as any other (new) shareholder would have paid. Distinguishing a share-based

payment from a shareholder transaction can be difficult if the counterparty

buys the equity instruments at the same amount as other shareholders (see

Example3.5.8 and A2.100 ‘Complex capital structures’).

IFRS 2.IG17 The implementation guidance to IFRS 2 discusses employee share purchase plans

and illustrates the application of the standard to those transactions in which there

is a discount on purchase or that contain option features. If an employee share

purchase plan does not appear to fall under this guidance, then it may be difficult

to determine whether the employee acts in the capacity of a shareholder or of a

supplier of goods or services. For further discussion of employee share purchase

plans, see 3.5.40.

Factors that in our view may be relevant in determining whether a purchase of

shares is in the scope of IFRS 2 include the following:

– the plan specifies that the realisation of a benefit is subject to future services;

and

– the plan includes buy-back terms that do not apply to non-employee shareholders.

For example, an employee may buy a share at a price that appears to be fair value,

but may be required to sell the share back at the lower of fair value at the date of

sale and the amount paid if they leave before a specified date.

In another example, senior management of entities owned by private equity funds

sometimes buy equity instruments with vesting being conditional on an exit event

(e.g. an IPO or a sale of the entity).

The following analysis considers each of the indicators above in relation to such

transactions.

– The arrangement contains a benefit that is subject to future services, because

the employee can benefit from future increases in the value of the shares only

by providing services for the specified period or by being employed when a

specified (e.g. exit) event occurs.

– There is an apparent inconsistency in these arrangements between the

proposition that the purchase of the shares is at fair value and the inclusion of

a requirement to sell the shares back at the lower of fair value and purchase

price. This requirement is, in effect, a right that allows the entity to reacquire the

shares in a transaction that has a positive value to the entity and has a negative

value to the employee. If the amount paid was the fair value of a share without

this condition, then the employee appears to have overpaid in buying the share;

the amount of the potential overpayment is the negative value of the entity’s

right to reacquire the shares. If the requirement to sell back was not imposed

on non-employee shareholders, then this may call into question the validity of

the assertion that the purchase was at fair value in the first place.

© 2018 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.

If applying these indicators results in the conclusion that a share purchase is

a share-based payment, then a second issue is whether there is any cost to

recognise if the transaction appears to be at fair value. Even if there is no cost to

recognise – e.g. because the purchase price is equal to the grant-date fair value of

the equity instruments granted – then in our view the disclosure requirements of

IFRS 2 still apply.

However, in certain cases it may be difficult to determine that the purchase price

is equal to the grant-date fair value of the equity instruments. This is particularly

challenging if the shares purchased by the employee are issued by an unlisted

entity with a complex capital structure – e.g. in some private equity transactions.

An entity may have multiple classes of shares. Sometimes the evidence that the

employee’s share purchase is at fair value is with reference to purchases of other

shares by non-employee shareholders. Difficulties can arise in allocating the fair

value of an entity between classes of equity instruments if the non-employee

shareholder transaction used as a reference involves more than one class (e.g.

ordinary and preference shares) but the employee only buys one class (e.g.

ordinary shares). This is because the buyers of more than one class of equity

instrument benefit from their investment differently from buyers of a single

class. If there are multiple classes of shares, then the complex capital structure

valuation guidance in A2.100 may be relevant in deciding if the amount paid by the

employee is below fair value.