A DISCUSSION PAPER FROM

5 April 2018

NETFLIX

IN CANADA

BINGE-WATCHING! TAX ISSUES!

REGULATORY UNCERTAINTY!

©

benchart/Shutterstock.com

i

Table of contents

Introduction .................................................................................................................................... 1

A slightly embarrassing Canadian launch … appears to have had

little impact on the rapid growth of Netflix in Canada ................................................................ 2

Netflix: Finding the Canadian numbers ........................................................................................ 3

Netflix subscribers and revenues in Canada .................................................................................. 3

What we know about Netflix subscribers in Canada ..................................................................... 6

Demographics ................................................................................................................................. 6

Do Netflix subscribers also subscribe to cable or satellite TV? .................................................... 9

Netflix subscribers in Canada, by province ................................................................................. 10

A taxing question: Netflix and sales taxes .................................................................................... 10

“No Netflix tax” and competitive advantage ................................................................................ 13

Broader implications for public policy ........................................................................................... 13

List of figures

1. Estimated and projected yearly average number of Netflix subscribers in Canada,

2011, and 2016 to 2020 .................................................................................................................. 5

2. Estimated and projected Netflix revenue in Canada, 2011, and 2016 to 2020 ....................... 5

3. Percentage of Canadians 15+ subscribing to Netflix, 2016, by age groups .............................. 7

4. Percentage of Canadians 15+ subscribing to Netflix, 2016, by home language ....................... 7

5. Percentage of Canadians 15+ subscribing to Netflix, 2016, by age groups and

selected home languages ................................................................................................................ 8

6. Percentage of Canadians 15+ subscribing to Netflix, 2016, by age groups and gender .......... 8

7. Percentage of Canadians 15+ subscribing to Netflix, 2016, by personal income groups ........ 9

8. Percentage of Canadians 15+ subscribing to cable or satellite TV and/or

subscribing to Netflix, 2016 ........................................................................................................... 10

9. Percentage of Canadians 15+ subscribing to Netflix, 2016, by province, indicating

whether or not those Netflix subscribers also subscribed to cable or satellite TV ....................... 11

10. Potential GST, and potential provincial sales tax revenue, if applied to Netflix’s

estimated and projected revenue in Canada, 2016 to 2o2o (in millions of dollars) ..................... 12

© 2018 Communications Management Inc. / E-mail: [email protected]

1

Introduction

Since it was introduced in Canada on September 22, 2010, Netflix has grown to the point where

it now is present in almost half of Canadian households. In a 2017 filing with the CRTC, Corus

Entertainment Inc. used data from Numeris to demonstrate that, by Fall 2016,

1

in primetime

viewing by Canadians 25-54, Netflix exceeded the time spent with CTV, Global, or CBC.

2

And, in

Fall 2017, Solutions Research Group found that English-speaking Canadians ranked Netflix as

one of their top five TV brands.

3

Along with that commercial success has come a series of debates about how Netflix should be

treated in relation to the Canadian broadcasting/programming services against which it

competes – not only other streaming services,

4

but also conventional TV broadcasting, specialty

and pay television, and the distribution platforms that deliver those services.

By the time the 2015 Canadian federal election was held, Netflix had become an issue, with the

then-Conservative government proclaiming “no Netflix tax”, and, in the 2015 campaign, the

other two major parties also promising not to tax the U.S. streaming service. Since the 2015

election, the new Liberal government has maintained that Conservative policy.

Yet the rallying cry for a tax-free Netflix has been subject to a number of interpretations and

justifications. Some have argued that it should be interpreted as meaning that Netflix should

not have to pay into program production funds to support Canadian producers.

5

Others have

argued that it means that Netflix should not – or could not – be required to pay federal or

provincial sales taxes. And, most recently, Canada’s Prime Minister, Justin Trudeau, stated that

the Conservative policy has been maintained because the current Liberal government “doesn’t

want to hurt Canadian taxpayers”.

6

The purpose of this discussion paper is not to argue, per se, with the decisions not to levy

program spending requirements or sales taxes on Netflix. Rather, our purpose is twofold:

1. First, to attempt to quantify Netflix’s size in Canada (in terms of subscribers and

revenues), and to provide more detail on who subscribes to the service, by age, by

language, by income, and by province; and

2. Second, to discuss Netflix in public policy terms – not only whether the different

treatment for Netflix is fair to Netflix’s Canadian competitors, but also (and perhaps even

more important) the fact that Netflix is an indicator of a rapidly-changing television

system, for which a very different regulatory approach will be required in the future.

1

As will be outlined later in this discussion paper, by the end of 2016, Netflix was being received in about

6.4 million Canadian households.

2

Corus Entertainment Inc., Phase I Comments, December 1, 2017, in response to Broadcasting Notice of

Consultation CRTC 2017-359.

3

Greg O’Brien, “Primetime online: Canadian Netflix users now watching more than 90 minutes a day”,

Cartt.ca, January 10, 2018.

4

Streaming services are often also called “over-the-top” or OTT services.

5

Netflix has not been required to pay into production funds or spend a regulated level of revenues on

Canadian content. However, in September 2017, the Minister of Canadian Heritage announced that

Netflix had agreed to spend $500 million over the next five years on Canadian production. A number of

industry participants have criticized that agreement for a lack of specific details, and because it allows

Netflix to spend a lower percentage on Canadian production than is required of Canadian broadcasters.

6

Morgan Lowrie (Canadian Press), “Trudeau stands by decision not to include tax on foreign online

businesses in federal budget”, Toronto Star, March 1, 2018 [accessed at www.thestar.com].

2

A slightly embarrassing Canadian launch …

As reported in the Toronto Star on September 23, 2010, Netflix’s launch in Canada had

some unexpected drama, as it was revealed that the crowd gathered to welcome the

announcement included actors paid by the streaming service.

7

… appears to have had little impact on the rapid growth of Netflix in

Canada:

Less than a year after its launch, on August 4, 2011, Netflix announced it had signed up its

millionth subscriber in Canada. That customer, Amanda Bell James, of Flin Flon, Manitoba,

was awarded a lifetime membership.

8

7

“Netflix offers ‘phenomenal deal’”, Toronto Star, September 23, 2010, p. B1.

8

“Netflix Surpasses 1 Million Members Milestone in Canada”, Netflix media release, August 4, 2011.

3

Netflix: Finding the Canadian numbers

As noted above, Netflix was introduced in Canada on September 22, 2010, and, at that point,

Canada was the first country outside the U.S. where Netflix offered the service. For a brief

period of time, it was possible to follow the growth of Netflix in Canada through Netflix’s

quarterly financial statements, since Canada was the only country in the “International”

category. However, that only lasted until September 12, 2011, when Netflix began rolling out its

service to many other countries. After that, Netflix did not publicly reveal its results for Canada.

However, since then, there have been periodic surveys of Netflix’s growth in Canada, from

sources like the CBC’s Media Technology Monitor (MTM) and from survey firms like Solutions

Research Group (SRG).

Fortunately, an additional major survey by Statistics Canada now can be added to those useful

reports. In the last five months of 2016, Statistics Canada conducted one of its periodic General

Social Surveys (GSS), and included a number of questions on Canadians’ use of technology,

including Netflix.

9

The survey covered persons 15+, and had a sample size of 19,609, so it is large enough to

produce custom tabulations of Netflix-related data by province, age, gender, language, income,

and a number of other variables. A summary of those custom tabulations is presented on the

following pages.

10

The GSS data also provide a useful benchmark for estimating the actual number of Netflix

subscribers in Canada at the end of 2016, which can then form a base for future projections, and

for estimates of Netflix’s revenue in Canada.

We have summarized the data in three sections:

1. Netflix subscribers and revenues in Canada, with projections to 2020;

2. What we know about Netflix subscribers in Canada;

3. A taxing question: Netflix and sales taxes.

Netflix subscribers and revenues in Canada

Based on the results of Statistics Canada’s 2016 GSS, 44.8 per cent of Canadians subscribed to

Netflix in the last part of 2016. (This is very close to the Fall 2016 finding from MTM that 44 per

cent of Canadians were Netflix subscribers.)

While the GSS data were based on persons 15+, the survey parameters were set so that there was

only one respondent per household. Thus, we believe that applying the percentage to the

number of households in Canada would provide a reasonable estimate of the number of Netflix

households in the last part of 2016.

9

The survey time period can be viewed as a “status report” for the last half of the 2016 calendar year. In

terms of broadcast fiscal years ending August 30

th

, it can also be viewed as covering the last month of the

2016 broadcast fiscal year, and the first four months of the 2017 broadcast fiscal year.

10

Please note that Statistics Canada’s 2016 General Social Survey covered the 10 provinces, but did not

include the three territories. Unless otherwise noted, the “Canada” totals shown in subsequent charts are

based on those 10-province totals.

4

We estimate that there were about 14.3 million households in Canada in 2016.

11

If we take 44.8

per cent of that number, then it appears reasonable to estimate that there were about 6.4 million

Canadian households with Netflix near the end of 2016. By combining that number with the

results of other surveys, we can further estimate that the average number of Netflix subscribers

in Canada during 2016 was 5.7 million.

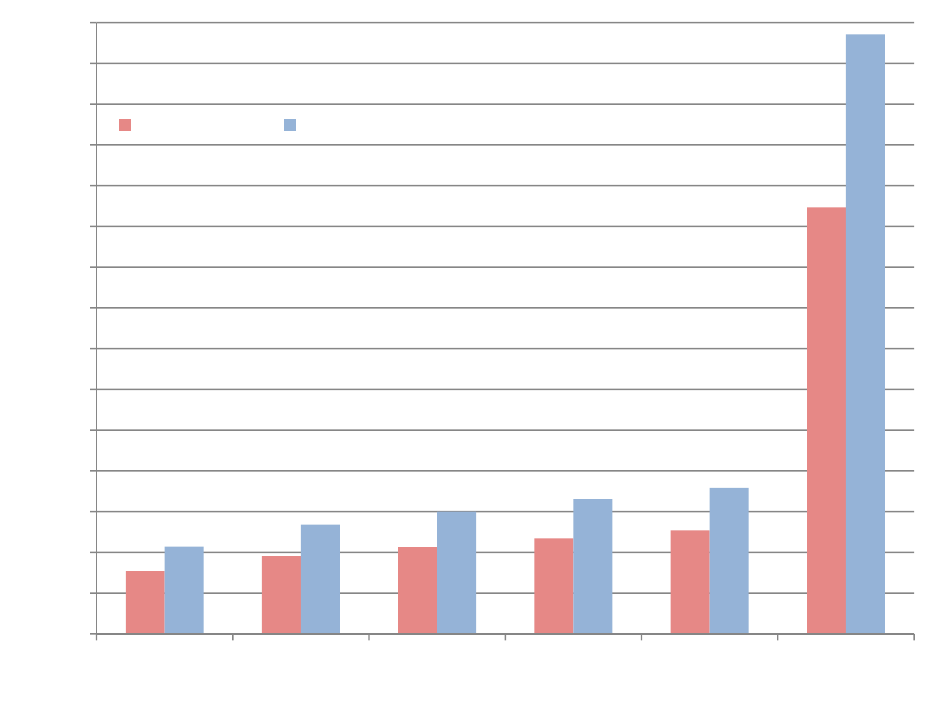

That represents more than a six-fold growth since 2011. Can that growth rate be maintained?

We would suggest that, after a period of such rapid growth, the growth rate will most likely slow

in coming years, and we believe there are two main reasons: First, as a service becomes more

widespread, it is difficult to maintain initial growth rates; and, second, because additional

streaming services are expected to be introduced into the Canadian market.

Our estimates and projections (to 2020) for the number of Netflix subscribers in Canada are

summarized in Figure 1.

In terms of Netflix’s Canadian revenues, we believe some of the recent estimates have overstated

that revenue. For example, the CRTC, in its Communications Monitoring Report 2017, has

provided an estimate of $766 million for Netflix’s revenue in Canada in 2016.

12

Other estimates

have been derived by simply multiplying an estimate of six million or so Netflix subscribers by

the current (or then-current) monthly rate.

But two important factors need to be considered:

1. Annual revenue should be based on the average number of subscribers in the year, not

just at one point in time; and

2. The average revenue per subscriber will likely be lower than the published rate, because

of promotional/introductory offers, old rates “grandfathered” for some time after a new

rate is introduced, and churn.

Thus, in October 2015, Netflix changed the rate for its “standard” package to $9.99 per month,

but existing subscribers were still charged the old rate ($8.99) well into 2016. We have not used

$9.99 per month as the effective rate for 2016; instead, we assumed an average effective rate of

$9.00 per month, as a way of accounting for the factors noted above. In our projections, we

then assumed an increase of 50 cents per month in the effective rate for each of the subsequent

years.

13

Using this methodology, combined with the subscriber data, we estimate Netflix’s revenue in

Canada in 2016 at $615.6 million, rising to $1,016.4 million in 2020. Our estimates and

projections for Netflix’s revenue in Canada are summarized in Figure 2.

Text continues on page 6 …

11

These data are based mainly on the household estimates from Statistics Canada’s 2016 Survey of

Household Spending.

12

CRTC, Communications Monitoring Report 2017, p. 146.

13

It should also be noted that Netflix had another Canadian rate increase in August 2017, when the rate

for its “standard” package was increased to $10.99 per month.

5

1.EstimatedandprojectedyearlyaveragenumberofNetflixsubscribersinCanada,2011,

and2016to2020

2.EstimatedandprojectedNetflixrevenueinCanada,2011,and2016to2020

900,000

5,700,000

6,700,000

7,100,000

7,450,000

7,700,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2011E 2016E 2017E 2018P 2019P 2020P

$74,000,000

$615,600,000

$763,800,000

$852,000,000

$938,700,000

$1,016,400,000

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

$800,000,000

$900,000,000

$1,000,000,000

$1,100,000,000

2011E 2016E 2017E 2018P 2019P 2020P

6

What we know about Netflix subscribers in Canada

In this section, we present a number of tables drawn from Statistics Canada’s 2016 General

Social Survey (GSS). As noted above, the survey was conducted in the last five months of 2016.

It had a sample size of 19,609, and covered persons 15+ in Canada’s 10 provinces.

Demographics

In Figures 3 to 7, we have summarized data from the 2016 GSS for a number of demographic

factors as they may relate to whether or not a person might be a Netflix subscriber.

Figure 3 summarizes Netflix subscribers by age group. As indicated in Figure 3, the percentage

subscribing to Netflix is highest in the youngest age group, slightly lower (but still higher than

the overall percentage) in the next two age groups, and then declines with age.

Figure 4 compares Netflix subscription percentages by home language, and indicates clear

differences for English, French, and those with non-official home languages.

14

Figure 5 combines data for age groups and home language, and indicates that, in the youngest

age group, those with French or non-official home languages have significantly higher Netflix

subscribing percentages than others in the same language group, which might foretell future

growth in those language groups.

15

Figure 6 summarizes data on Netflix subscribers by age group and gender, and shows, overall, a

slightly higher percentage of females subscribing to Netflix than the percentage of male

subscribers.

Figure 7 summarizes data on Netflix subscribers by personal income.

16

Text continues on page 9 …

14

In Figures 4 and 5, the term “non-official language(s)” encompasses “non-official language or multiple

non-official languages”.

15

The question of whether patterns of media use by younger groups can be seen as a predictor of future

trends has been discussed for many years. For example, almost 40 years ago, in 1979, Statistics Canada

published a paper that documented that readership of daily newspapers was lower for persons under 30,

and then noted: “We must remember that people under thirty constitute the group of Canadians who

did not experience the pre-television era. All of them spent even their earliest childhood in the presence

of a television. Today we must ask whether TV is actually in the process of replacing the newspaper as

we have known it, or whether, as they grow older, these young people will turn to the newspapers and,

following in their parents’ footsteps, become regular readers of news, editorials, financial reports and

articles on household matters.” (Yvon Ferland, “The Canadian and his Newspaper,” Canadian Statistical

Review. July 1979, p. xii.)

16

Please note that, in the 2016 GSS survey, income data were based on incomes in 2015.

7

3.PercentageofCanadians15+subscribingtoNetflix,2016,byagegroups

4.PercentageofCanadians15+subscribingtoNetflix,2016,byhomelanguage

0%

10%

20%

30%

40%

50%

60%

70%

80%

Allpersons

15+

15‐24 25‐34 35‐44 45‐54 55‐64 65+

0%

10%

20%

30%

40%

50%

60%

Allpersons

15+

English French Non‐official

language(s)

Englishand

French

Englishand

non‐official

language

Frenchand

non‐official

language

English,

Frenchand

non‐official

language

8

5.PercentageofCanadians15+subscribingtoNetflix,2016,

byagegroupsandselectedhomelanguages

6.PercentageofCanadians15+subscribingtoNetflix,2016,byagegroupsandgender

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Allpersons

15+

15‐24 25‐34 35‐44 45‐54 55‐64 65+

Alllanguages English French Non‐officiallanguage(s)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Allpersons

15+

15‐24 25‐34 35‐44 45‐54 55‐64 65+

Allpersons Female Male

9

7.PercentageofCanadians15+subscribingtoNetflix,2016,bypersonalincomegroups

Do Netflix subscribers also subscribe to cable or satellite TV?

There has been considerable discussion in recent years about the degree to which “over-the-top”

(OTT) or streaming services, like Netflix, have contributed to “cord-cutting” or “cord-shaving” –

the reduction, in whole or in part, of subscriptions to cable or satellite TV services.

As can be seen from Figure 8, the 2016 GSS found that 76.2 per cent of respondents reported

subscribing to satellite or cable TV, while 44.8 per cent of respondents reported subscribing to

Netflix. Figure 8 also indicates the percentages for those who subscribed to both, to cable

and/or satellite TV without Netflix, or to Netflix without cable and/or satellite TV.

17

17

Statistics Canada’s 2016 GSS asked respondents if they subscribed to “cable or satellite” TV, and, as

noted above, and in Figure 8, 76.2 per cent responded in the affirmative. In addition to “cable” TV as it

was traditionally understood, many Canadians subscribe to television packages through “telco TV”/IPTV,

which offers similar services. All three types of services are considered “broadcasting distribution

undertakings” (BDUs) by the CRTC. To check whether the 2016 GSS data are representative of the BDU

market, we compared the 2016 GSS results with 2016 data from the CRTC and from Statistics Canada’s

2016 Survey of Household Spending (SHS). According to the CRTC, in 2016, BDU subscriptions in

Canada totaled about 11.1 million, which would be about 78 per cent of households. Statistics Canada’s

2016 SHS produced similar totals. (The SHS also found that about one per cent of Canadian households

subscribed to more than one type of BDU.) On the basis of those benchmarks, we believe the 2016 GSS

“cable and satellite” TV data provide a reasonable representation of Canadians subscribing to BDUs for

television.

0%

10%

20%

30%

40%

50%

60%

70%

Allpersons15+

Lessthan$20,000

$20,000‐$39,999

$40,000‐$59,999

$60,000‐$79,999

$80,000‐$99,999

$100,000‐$119,999

$120,000+

10

8.PercentageofCanadians15+subscribingtocableorsatelliteTV

and/orsubscribingtoNetflix,2016

Netflix subscribers in Canada, by province

In Figure 9, we have summarized the data for the percentage subscribing to Netflix in each

province, and also indicated the breakdown for subscribers with and without cable or satellite

TV. Not surprisingly, the lowest percentage is in Quebec, which is a reflection of the language-

related data noted above.

A taxing question: Netflix and sales taxes

As noted above, the phrase “No Netflix tax” has come to include not levying GST or provincial

taxes on the monthly Netflix subscription fee, although the most recent (March 27, 2018)

Quebec Budget did indicate an intention to apply Quebec’s provincial sales tax to Netflix and

other similar services.

By relating the percentages in Figure 9 to the number of households, we can derive a reasonable

estimate of the number of Netflix-subscribing households in each province. We can then also

estimate the revenue that Netflix receives from each province, and project those revenues

forward as a proportion of the overall projections for Netflix in Canada.

44.5%of

Canadians

hadcableor

satelliteTV,

butDID

NOThave

Netflix

31.7%ofCanadians

hadcableor

satelliteTVAND

alsohadNetflix

13.1%ofCanadians

hadNetflix,butDID

NOThavecableor

satelliteTV

TotalwithcableorsatelliteTV:76.2%

TotalwithNetflix:44.

8

%

11

9.PercentageofCanadians15+subscribingtoNetflix,2016,byprovince,indicating

whetherornotthoseNetflixsubscribersalsosubscribedtocableorsatelliteTV

The next step is to apply the GST, plus the provincial portion of the Harmonized Sales Tax

(HST) or the provincial sales tax (PST) to those revenues for each of the provinces. (Alberta has

no provincial sales tax, so only the GST would apply in that province.)

The results are summarized in Figure 10, which estimates the potential sales tax revenue from

Netflix subscriptions for the years 2016 to 2020, and then also derives the cumulative amounts

over the five-year period.

As indicated in Figure 10, had the various sales taxes applied to Netflix subscriptions in 2016,

the federal government would have realized an estimated $30.8 million in GST revenue, and the

provincial governments would have realized an estimated total of $42.8 million, for an overall

total of $73.6 million.

Over the five year period (2016-2020), the cumulative total potential is estimated at $209.3

million in GST revenue, and $294.3 million in provincial HST

18

or sales tax revenues, for a total

of $503.6 million – just over half a billion dollars.

In setting out these estimates, we are not necessarily suggesting that those taxes should or

should not be levied; rather, we are attempting to quantify the value of the differential between

the treatment of competing services (Netflix vs. Canadian competitors) within the same relevant

market.

18

“Provincial HST” refers to the provincial portion of the combined tax, in those provinces that have

adopted the Harmonized Sales Tax. For example, in Ontario, the federal portion of the HST is 5 per cent

(the GST rate) and the provincial portion is 8 per cent.

44.8%

54.4%

58.5%

54.6%

52.4%

47.1%

23.5%

49.8%

55.0%

56.9%

59.2%

0%

10%

20%

30%

40%

50%

60%

70%

Canada BC AB SK MB ON QC NB NS PE NL

Withcableorsatellite Withoutcableorsatellite

12

10.PotentialGST,andpotentialprovincialsalestaxrevenue*,ifappliedtoNetflix’s

estimatedandprojectedrevenueinCanada,2016to2020(inmillionsofdollars)

*ProvincialsalestaxrevenueisbasedonestimatingtheNetflixrevenueineachprovinceineachoftheyears,and

thenapplyingtheeffectiveratesforeachprovince’sprovincialsalestax(PST)ortheprovincialportionofthe

HarmonizedSalesTax(HST).For2016and2017,theratesare

thoseineffectinthoseyears(andtakeintoaccount

anyratechangesduringthoseyears).For2018,2019,and2020,ratesarethoseineffectatthebeginningof2018.

TheGSTdataarebasedonthecurrentGSTrateandthetotalsforthe10provinces(asnotedabove,

Statistics

Canada’s2016GeneralSocialSurveydidnotincludethethreeterritories).

__________________________________________________________________

As outlined in the section titled “‘No Netflix tax’ and competitive advantage”, on the next page,

the different treatment of competitors creates a structural imbalance within the Canadian

television system.

To the extent that it is argued that sales taxes should not be levied on Netflix and other similar

services, then it would seem only logical to consider removing those taxes from their Canadian

competitors – the online services, of course, but possibly also cable- and satellite-delivered

services, which are part of the same competitive market.

30.8

38.2

42.6

46.9

50.8

209.3

42.8

53.6

60.0

66.2

71.7

294.3

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

300

2016E 2017E 2018P 2019P 2020P 2016‐2020

(Cumulative)

$million

GSTpotential ProvincialHSTorPSTpotential‐‐allprovincescombined

13

“No Netflix tax” and competitive advantage

As of this date, only Quebec has announced an intention to levy its provincial sales tax on

Netflix within the province.

To the extent that a non-Canadian video service is exempt from sales taxes (federal and/or

provincial), it creates a structural marketplace advantage in favour of the tax-exempt

service, and against its Canadian competitors – not only streaming services, but all video

services for which consumers pay some or all of the cost.

Let's look at a practical example, using a hypothetical total consumer cost of $10 per

month, and the Ontario HST rate of 13%.

If a consumer is willing to pay $10 a month for an online video service, she can get the

service from a tax-exempt provider for that amount, and the tax-exempt provider will

receive the entire $10.

She can also get the service from a Canadian provider, but if the spending is to be kept

constant at $10 a month, then the Canadian provider will only receive $8.85; the remaining

$1.15 goes to HST ($8.85+13%=$10.00).

That means that, for every $10, the tax-exempt provider has an advantage of $1.15, and that

advantage can be used in a number of ways, including:

1. Higher profits for that non-Canadian provider;

2. More spending on programming, to make that non-Canadian service even more

attractive to consumers; and/or

3. Flexibility to offer discounts from time to time, to help increase subscriber totals.

Broader implications for public policy

Given the focus that has been created by the “No Netflix tax” debate, there is a possibility that

some might view Netflix only through the lens of tax issues. That would be a mistake.

The way public policy evolves to deal with Netflix has implications far beyond just taxes, because

Netflix is but one high profile example of a series of changes that are using technology to remake

the economics of television. Common sense and fairness demand that the tax issues be resolved,

but public policy should also be looking farther ahead to deal with future structural change.

In 2014 and 2015, we set out the view that television is evolving away from its traditional

structure, and towards what might be called “e-commerce for programs”.

19

19

See:

http://media-cmi.com/downloads/A_12_word_template_for_the_future_of_television_011414.pdf;

and: http://media-cmi.com/downloads/CMI_Discussion_Paper_Digital_Divides_082015.pdf.

14

__________________________________________________________________

Netflix is an important part of that trend, and it has impacts well beyond the current debate on

taxes for digital services.

At the beginning of this discussion paper, we noted that, by Fall 2016, in primetime viewing by

Canadians 25-54, Netflix exceeded the time spent with CTV, Global, or CBC. Those kinds of

audience impacts are not limited to Canada.

The U.K. television market is one of the largest in the world, and the BBC is one of the largest

public broadcasters in the world. Yet, on March 8, 2018, The Telegraph reported:

The BBC is no longer a dominant force in television, the Corporation’s second-in-

command has admitted, in the face of an onslaught from the “creative and financial

firepower” of US tech giants.

20

Later in March 2018, both The Times and The Guardian reported that the BBC’s latest annual

plan had revealed that young people are spending more time watching Netflix than all BBC

television.

21

20

Christopher Williams, “BBC no longer a dominant force in television, says deputy director-general”, The

Telegraph, March 8, 2018 [accessed online at www.telegraph.co.uk].

21

Mark Sweney, “Younger viewers now watch Netflix more than the BBC, says corporation”, The

Guardian, March 28, 2018 [accessed online at www.theguardian.com/media]; Matthew Moore, “Young

watching more Netflix than BBC”, The Times, March 29, 2018 [replica edition].

15

In the U.K., the audience displacement is seen as a threat to the continued ability to produce

national (U.K.) content. In the U.S., concerns have also been expressed about the impact of

audience displacement on the advertising market.

On February 15, 2018, a report at MediaPost.com was headlined: “Netflix Costs TV Nets Billions

In Lost Ad Revenue”. According to the report:

An analysis in nScreenMedia estimates Netflix has taken anywhere from $3 billion

to $6 billion per year off the table in TV advertising revenue as a result of the

viewing on its platform. In the past, such viewing would have gone to ad-supported

TV networks.

22

It is possible, of course, that part of that Netflix viewing was also coming from television that

was not ad-supported, so the actual revenue reduction might have been somewhat lower. The

general point, however, is valid – viewing time and revenues are being displaced from the old

structure of television.

At the most fundamental level, Canadian public policy should use the rapid growth of Netflix as

a signal to change two important components of how we deal with broadcasting policy in

Canada:

1. How we define markets; and

2. How we measure markets.

Going forward, broadcast markets – and media markets generally – will have to be defined to

include all of the sources that consumers might use to access information and entertainment,

and the way we regulate those components that fall within Canadian jurisdiction will have to

evolve to take that into account. To do otherwise would be to leave our regulatory mechanisms

in the position of regulating more and more of less and less – the application of regulatory

obligations that made sense when broadcasting was an oligopoly, but are no longer realistic

when competition is unlimited and borderless.

Equally, crafting the right regulatory responses will require better tools and better statistics for

measuring the entirety of the relevant markets for information and entertainment.

Ultimately, after all of the data are analyzed, the way Canadian public policy deals with Netflix

is, at its core, about two things – fairness … and the future of television in Canada.

22

Wayne Friedman, “Netflix Costs TV Nets Billions In Lost Ad Revenue”, February 15, 2018,

TelevisionNewsDaily [accessed at www.mediapost.com].