Department of Defense

Financial Management Functional Strategy

for Fiscal Years 2020-2024

Version 4.0

June 2020

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

2

Table of Contents

Executive Summary ........................................................................................................................ 5

FM Strategic Outcomes: .......................................................................................................... 5

FM Functional Strategy Goals:................................................................................................ 5

Introduction ..................................................................................................................................... 8

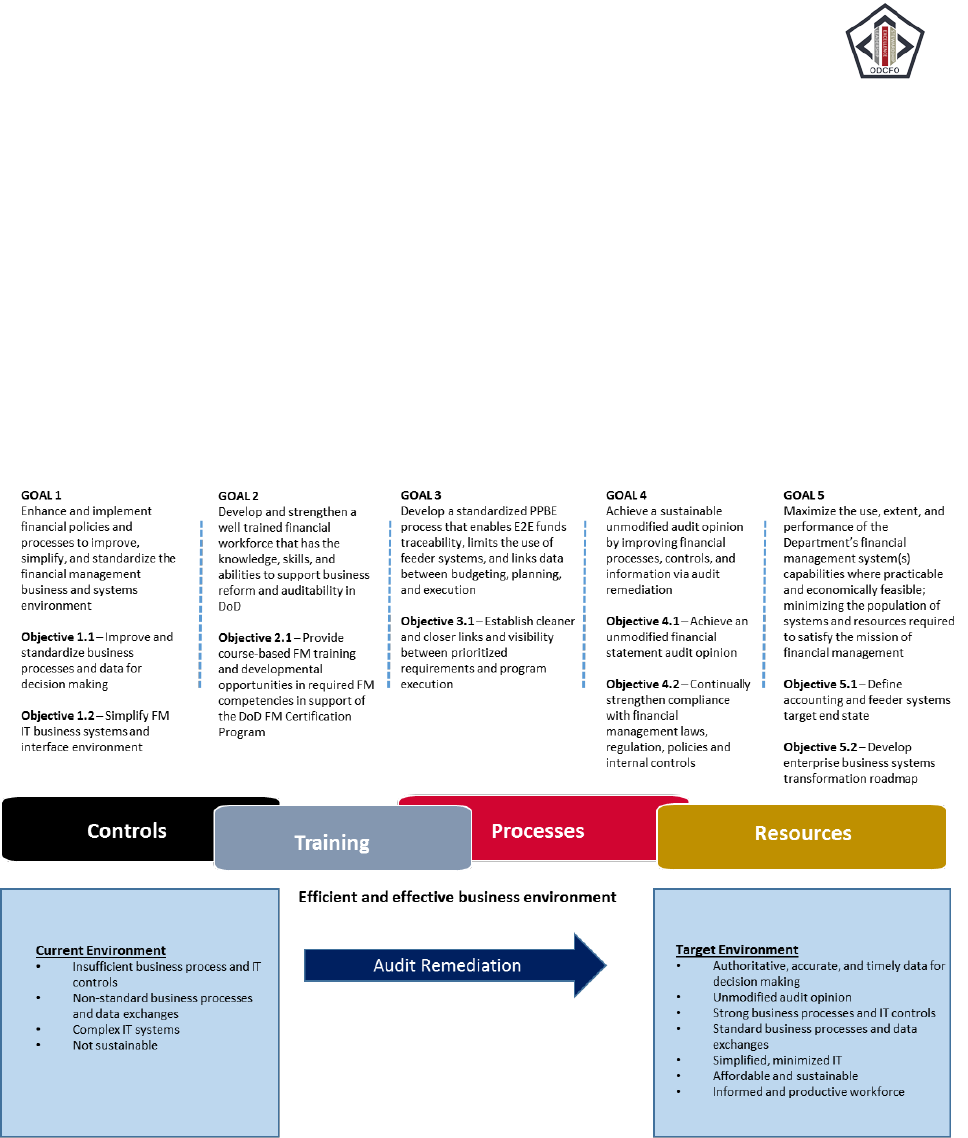

Section 1. Goals and Objectives ................................................................................................... 11

GOAL 1 – Continue to enhance and implement financial policies and processes to improve,

simplify, and standardize the FM business and systems environment ...................................... 12

Objective 1.1 – Improve and standardize business processes and data for decision making 12

Objective 1.2 – Simplify FM IT business systems and interface environment ..................... 13

GOAL 2 – Develop and strengthen a well-trained financial workforce that has the knowledge

skills, and abilities to support business reform and auditability in DoD. ................................. 15

Objective 2.1 – Provide course-based FM training and developmental opportunities in

required FM competencies in support of the DoD FM Certification Program. .................. 157

GOAL 3 – Develop a standardized PPBE process that enables E2E funds traceability and data

linkage between planning, budgeting, and execution ............................................................. 188

Objective 3.1 – Establish clearer and closer links between prioritized requirements and

program execution ................................................................................................................. 19

GOAL 4 – Achieve a sustainable unmodified audit opinion by improving financial processes,

controls, and information via audit remediation ....................................................................... 20

Objective 4.1 – Achieve an unmodified financial statement audit opinion . Error! Bookmark

not defined.

Objective 4.2 – Continually strengthen compliance with financial management laws,

regulations, policies, and internal controls ............................. Error! Bookmark not defined.

GOAL 5 – Maximize the use, extent, and performance of the Department’s Defense Business

System(s) capabilities where practicable and economically feasible; minimizing the population

of systems and resources required to satisfy the mission of the FM community, to include

increased cooperation and coordination among business system owners to facilitate timely and

effective transformation………………………………………………………………………..24

Objective 5.1 - Define Accounting and Feeder System Target End State………………….24

Objective 5.2 - Develop Defense Business Systems Transformation Roadmap……………26

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

3

Section 2. Financial Management Enterprise Initiatives ......................................................... 27

1. ADVANA .......................................................................................................................... 29

2. USSGL/SLOA/SFIS Compliance .................................................................................... 321

3. Fund Balance with Treasury (FBWT) – Cash Accountability and Traceability ............. 362

4. Intragovernmental Transactions (IGT) ............................... Error! Bookmark not defined.

5. Property ............................................................................................................................ 377

6. Journal Vouchers (JVs) ...................................................................................................... 39

7. Financial Management Information Technology Systems Environment .......................... 40

8. Funds Distribution ............................................................................................................. 42

9. Cost Management .............................................................................................................. 43

10. Planning, Programming, Budgeting and Execution Process Standards ......................... 44

Procure-to-Pay Standards ..................................................................................................... 44

11. DoD FM Certification Program (DFMCP) .................................................................... 46

12. DATA Act ...................................................................................................................... 47

Conclusion .................................................................................................................................. 488

Appendix A – List of Terms ....................................................................................................... A-1

Appendix B – List of Acronyms ................................................................................................. A-4

List of Figures

Figure 1 – FM Data-First Agile Approach ..................................................................................... 6

Figure 2 – FM Functional Strategy ................................................................................................. 7

Figure 3 – Target Approach ........................................................................................................... .9

Figure 4 – FM Data-First Approach ............................................................................................ .10

Figure 5 – FM Functional Strategy Goals and Objectives ............................................................ 11

Figure 6 – “Notional” Defense Business Systems Transformation Roadmap…………………...27

Figure 7 – Financial Mangement Target Equation………………...…………………………….29

Figure 8 – Notional Standard Processes and Data ........................................................................ 41

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

4

List of Tables

Table 1 - ADVANA (formerly, Universe of Transactions) Overview ............................................. .30

Table 2 – United States Standard General Ledger Overview/Standard Line of Accounting/

Standard Financial Information Structure .................................................................................... .31

Table 3 – Fund Balance with Treasury CASH Overview ............................................................ .35

Table 4 – Intragovernmental Transactions Overview .................................................................. .37

Table 5 – Property Overview ....................................................................................................... .38

Table 6 – Journal Vouchers Overview......................................................................................... .39

Table 7 – Financial Management Information Technology Systems Overview ......................... .42

Table 8 – Funds Distribution Overview....................................................................................... .43

Table 9 – Cost Management Overview ........................................................................................ 43

Table 10 – Planning, Programming, Budget, and Execution Standards Overview ..................... .45

Table 11 – DoD Financial Management Certification Overview ................................................ .46

Table 12 – DATA Act Overview ................................................................................................. .47

Published by the Business Process and Systems Modernization Office, Office of the Deputy

Chief Financial Officer, Office of the Under Secretary of Defense, U.S. Department of

Defense.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

5

Executive Summary

The Office of the Under Secretary of Defense (Comptroller) (OUSD(C)) is the principal

organization tasked with reform to build a simplified, standardized, and data-driven target

financial management (FM) environment. This reform aligns with the National Defense Strategy

and supports leadership’s drive for the Department of Defense (DoD) to become more

productive, effective, and streamlined.

For the first time in history, the Department conducted a full financial statement audit in FY

2018, and now more recently, the subsequent audit in FY 2019. The financial statement audits

resulted in findings from many different functional areas, and the remediation of these findings

will be a significant part of the Department’s FM improvement strategy and an accelerator for

achieving a target environment that is data-driven, standards-based, technology-enabled,

affordable, secure, and auditable.

Rooted in fiscal accountability and financial improvement, the DoD FM Functional Strategy FYs

2020-2024 will lead to strategic outcomes essential for meeting the Department’s national

security mission.

FM Strategic Outcomes:

• Stewardship and public trust of taxpayer funds through transparency

• Audit corrective action sustainability

• Strengthened mission capabilities

• Authoritative, accurate, and timely information for decision making

• Informed, trained, and productive workforce

• Affordable and secure Financial Management environment

• Robust internal control environment which will support and sustain an unqualified audit

opinion

The following five goals are written to facilitate the strategic outcomes.

FM Functional Strategy Goals:

• GOAL 1 – Continue to enhance and implement financial policies and processes to

improve, simplify, and standardize the FM business and systems environment.

• GOAL 2 – Develop and strengthen a well-trained financial workforce that has the

knowledge skills, and abilities to support business reform and auditability in DoD.

• GOAL 3 – Develop a standardized planning, programing, budget and execution (PPBE)

process that enables end-to-end (E2E) funds traceability, limits the use of feeder systems,

and links data between planning, budgeting, and execution.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

6

• GOAL 4 – Achieve a sustainable unmodified audit opinion by improving financial

processes, controls, and information via audit remediation.

• GOAL 5 – Maximize the use, extent, and performance of the Department’s Defense

Business System(s) (DBS) capabilities where practicable and economically feasible;

minimizing the population of systems and resources required to satisfy the mission of the

FM community, to include increased cooperation and coordination among business

system owners to facilitate timely and effective transformation.

The approach to achieving the goals of the FM Functional Strategy complements the

Department’s audit remediation strategy. Both strategies place the FM community at the focal

point for not just policy and financial reporting, but also operational, performance, and risk

management. To meet this demand, the FM community must consider expanding its “business

partnering” opportunities within DoD and federal government, whereby the focus is upon

improving strategic and operational decision-making reliant upon data and analytics. Business

partnering is more so collaboration and potential leveraging of current and future capabilities that

should align with one or more of the five stated goals. Twelve FM Enterprise Initiatives are

underway to improve, standardize, and simplify existing processes and systems and establish a

foundation for accurate, reliable, and timely data.

By working to implement the FM Enterprise Initiatives and achieve the FM Functional Strategy

goals, the FM community will transform to a data-first culture and add significant strategic value

to DoD decision-making. A “data first” culture places strong emphasis upon aggregation and

cultivation of prioritized data and analytics needed by leadership and staff to manage the

organizational business environment in achieving its defined goals and objectives. Figure 1

shows the data-first approach. By better leveraging the power of data, FM leaders can help

transform the organization’s ability to predict outcomes, plan, and respond appropriately. Not

only will this radically enhance enterprise decision-making, it will significantly increase the FM

function’s ability to contribute strategic value to the Department.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

7

Figure 1 – FM Data-First Approach

The FM Functional Strategy, depicted in Figure 2, offers FM direction and guidance for the

Principal Staff Assistants (PSAs), Military Departments (MILDEPs) and Other Defense

Organizations (ODOs) as the Department builds for the future. It also provides a foundation on

which to base FM investment decisions that support the FM strategic outcomes.

Figure 2 – FM Functional Strategy

PSAs, MILDEPs, and ODOs should use the FM Functional Strategy during planning and

implementation to ensure:

• A shared vision of FM across the Department that is consistent with DoD’s vision,

mission, and business goals.

• Alignment of FM initiatives with business and audit priorities.

• Dissemination of knowledge about FM-related critical issues and solutions.

• Compliance with DoD’s process and data requirements through strong governance and

informed decision-making.

• Achievable FM milestones that incrementally advance the Department to achieve its

target environment.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

8

• Effective implementation of Corrective Action Plans (CAPs) aligned with the FM

Functional Strategy that produce sustainable results.

• Reduction of FM legacy, antiquated systems unable to support audit requirements.

• Reduction of point-to-point interfaces to minimize complexity and risk.

• Integrates with respective PSA functional strategy initiatives.

Introduction

The Department of Defense provides combat- military

forces needed to deter war and protect the security of the

nation. To accomplish this mission, the National

Defense Strategy defines three lines of effort. The FM

Functional Strategy aligns with the first and third lines

of effort. The first line of effort aims to restore readiness

to defeat enemies and achieve sustainable outcomes that

protect the American people and our vital interests. The

third line of effort, to reform the Department’s business

practices for greater performance and affordability, aims

to remedy what the Defense Strategy describes as DoD’s

“increasingly unresponsive” environment by

transitioning to a “culture of performance where results

and accountability matter.” It charges the DoD to:

• Deliver performance at the speed of relevance,

• Organize for innovation,

• Drive budget discipline and affordability to

achieve solvency,

• Streamline rapid, iterative approaches from development to fielding, and

• Harness and protect the National Security Innovation Base.

The OUSD(C) is leading DoD’s workforce management transformation as well as the reform of

FM operations into a more standardized and simplified target environment. The DoD FM

Functional Strategy for FY 2020-2024 defines the goals, objectives, and related enterprise

initiatives for achieving a data-driven, standards-based, technology-enabled, affordable, secure,

and auditable systems environment.

The OUSD(C) also leads the annual full financial statement audits, which began in FY 2018.

The audits—likely the largest audits ever undertaken—resulted in findings that DoD leaders are

using to prioritize and focus remediation work. Audit remediation of systems and processes is

foundational to DoD FM evolving from a transactional focus to a value-adding, strategic focus.

END STATE VISION:

Achieve a target FM environment that

is data-driven, standards-based,

technology-enabled, affordable,

secure, and auditable.

FINANCIAL MANAGEMENT

MISSION:

Develop and defend budgets; shape

and provide oversight of FM policy

and operations; strengthen the FM

workforce; maintain a simplified and

standardized FM environment; and

support the mission of the DoD in a

manner that is legal, effective, and

efficient.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

9

Figure 3 shows how the target approach to achieving the FM Functional Strategy complements

the Department’s audit remediation strategy and incrementally builds on audit successes.

Figure 3 – Target Approach

The focus on remediating audit findings will accelerate FM reform by standardizing and

improving information at all levels of data management and governance as shown in Figure 4.

By better leveraging the power of data, FM leaders can help transform FM ability to predict

outcomes, plan, and respond appropriately. Actionable data intelligence will radically enhance

Department-wide decision-making and significantly increase FM’s contribution to the overall

National Defense Strategy.

Strengthen the Foundation (FY 2020)

* Achieve compliance with USSGL/SLOA/SFIS

standards

* Finalize data strategy

* Continue shift to annual audit culture and

remediation (NFR and CAP tracking and resolution)

Strengthen the Surroundings (FY 2021-2023)

* Fix critical feeder/reporting systems

* Aggressively sunset legacy systems

* Implement direct treasury disbursing, intra-governmental

transactions, cash accountability, and procure-to-pay

“handshakes” initiatives

* Reduce point to point interfaces (via DoD Global data

Exchange (GEX) or Application Program Interfaces (APIs)

* Automate processes (e.g. robotics)

* Implement big data and analytics technologies

Build to the Future (FY 2024+)

* Enable interoperability between systems

* Manage via financial management, performance

management, risk management, and cost management

analytics

* Standardize shared service environment

* Strengthen the foundation of audit and internal

controls best business practices

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

10

Figure 4 – FM Data-First Approach

The FM Functional Strategy was developed to meet the needs and requirements of multiple

audiences including FM executives, analysts, and system program managers. The

recommendations are based on rigorous analysis, including consultation with other federal

agencies, benchmarking against leading commercial practices, and results of multiple pilot

efforts currently underway in the DoD. The strategy addresses specific material weaknesses and

critical issues that adversely affect the way the Department conducts business. It also provides

direction and guidance to the MILDEPs and ODOs for portfolio-based investments, the DoD’s

FM vision over the next five years, and a prioritized focus on remediating audit findings to

achieve an unmodified audit opinion.

Section 1 of the FM Functional Strategy defines five high-level goals and expected business

outcomes of achieving each goal. Supporting objectives add focus to each goal. Actions the

Department must take to meet each objective and possible success indicators are also described.

Related FM Enterprise Initiatives, such as improving cost management, are listed for each

objective. Section 2 of this strategy presents a more detailed overview of each of the 12 FM

Enterprise Initiatives. A list of terms and acronyms are included in Appendix A and B.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

11

Section 1. Goals and Objectives

Today’s FM community faces myriad challenges from leveraging data and information to make

critical investment decisions to making progress toward achieving an unmodified audit opinion.

Issues such as non-standard processes and technology applications and interfaces, and difficulties

in finding and retaining the right skill sets continue to slow progress in DoD achieving its FM

target state.

The five FM Functional Strategy goals and corresponding objectives as shown in Figure 5

provide a framework for how the financial community will achieve its data enabled target state.

Figure 5 – FM Functional Strategy Goals and Objectives

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

12

GOAL 1 – Enhance and implement financial policies and processes to improve, simplify,

and standardize the FM business and systems environment

Without continual improvement, achieving an unmodified audit opinion may not be efficient or

sustainable. Objectives 1.1 and 1.2 support the achievement of a standardized and simplified FM

business and systems environment. The first steps are to define and improve business processes

to conform to financial policies, then define the data environment, and, finally, implement the

technology. Advances in technologies such as process automation using robotics and big data,

and analytics will give DoD leaders real-time access to strategic data and allow the workforce to

focus more on analysis and less on transaction processing. Tone from the top must promote a

strong internal control program as a top priority from senior management.

Expected Business Outcomes: reduced reconciliation work to identify, cultivate, and

assemble data; supportable transactions; stronger internal controls; timely, accurate, and

reliable financial data and cost tracking; improved interoperability between systems; E2E

funds traceability between budget and expenditures; and cost effective business

environment

Objective 1.1 – Improve and standardize business processes and data for decision making

The complexity and differences in business processes and data across the Department make it

difficult for an auditor to understand DoD’s business and for a financial manager or program

manager to implement or execute those processes efficiently and effectively. The Department

must continue its drive toward a culture of continual improvement with a focus on standardizing

and simplifying E2E processes.

The lack of fully implemented data standards makes it difficult for the Department to be

interoperable and communicate effectively across the enterprise. The implementation and

enforcement of data standards and business rules will improve the timeliness, accuracy, and

reliability of financial data, allow for better decision making, and reduce costly reconciliation

work.

To meet this objective, the Department must:

• Develop, implement, and enforce data standards (e.g., United States Standard General

Ledger (USSGL), Standard Line of Accounting (SLOA), Standard Financial Information

Structure (SFIS), Purchase Request Data Standard (PRDS), and Procurement Data

Standard (PDS))

• Conduct standards assessment reviews on audit critical FM systems

• Focus on E2E process improvement and business process re-engineering

• Apply business best practices already implemented in the DoD

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

13

• Establish business performance metrics and action plans with focus on root cause

resolution

• Eliminate non-value added process steps

• Focus on continual process improvement

• Leverage data analytics technologies

• Use data to make critical, strategic, and operational business decisions

Related FM Enterprise Initiatives: USSGL/SLOA/SFIS compliance, PPBE standards, funds

distribution, Intragovernmental Transactions (IGT), ADVANA, Fund Balance with Treasury –

Cash Accountability and Traceability (FBWT – CASH), and cost management

Possible Success Indicators:

• Percent of systems compliant with USSGL/SLOA/SFIS

• Percent of SFIS elements available without any data transformation or crosswalk

• Percent of accounting systems compliant with PDS and PRDS

• Percent of entitlement systems compliant with PDS

• Percent of transactions compliant with SLOA using the SLOA validation service

• Percent of key data exchanges using the SLOA validation service

• Percent of DoD organizations that have implemented the DoD cost management

framework

• Percent of source system attributes that carry forward to accounting event

• Percent of appropriations that use Enterprise Funds Distribution (EFD) to track to the

lowest level of distribution by budget allotment line item identifier

Objective 1.2 – Simplify FM IT business systems and interface environment

The number and variety of DoD business and financial systems as well as the level of effort and

cost to achieve an unmodified audit opinion are significant. Systems material to audit include

DBSs, custom-built legacy systems, financial systems, micro-applications, and non-financial

feeder systems.

Systems also vary widely in technology and function. Financial systems include budget,

accounting, and finance systems, as well as business feeder systems, such as personnel, logistics,

and property systems where most financial transactions originate. Despite the progress made,

there are still dependencies on point-to-point interfaces multi-tiered interfaces, super feeders that

consolidate transactions, and legacy systems built prior to current data standards and laws,

regulations, and policies, such as FFMIA, USSGL, SFIS, and the Treasury Financial Manual.

It is difficult to reconcile financial statements to the specific business events due to the lack of

standard business processes; data exchange standards; use of non-accounting feeder system; and

reliance on point-to-point interfaces. These legacy systems and point-to-point interfaces often

lack controls as identified in DoD-wide recent and past DoD financial statement and systems

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

14

audit results. The complexity of DoD’s business systems environment has made the audit

challenging. Shared-common, standardized, brokered services streamlining data standards

compliance are key alternatives for the Department to leverage to fullest extent possible in lieu

of upgrading these applications to be compliant, which will be costly and time consuming.

Implementing standard business processes and data, big data and analytics technologies,

automation via robotics, reducing the number of legacy systems and point-to-point interfaces,

and utilizing existing compliant FM target systems will simplify the business environment.

To meet this objective, the Department must:

• Retire legacy systems, especially non-value added feeder systems that consolidate

transactional data

• Maximize the use and functional footprint of DBSs, when appropriate, to reduce the

number of systems, interfaces, handoffs, and customizations in order to leverage proven

existing controls

• Establish and enforce data standards and exchanges

• Utilize the GEX as a Standard Transaction Broker (STB) or Application Programming

Interfaces (APIs) to reduce point-to-point interfaces, improve interoperability between

systems, and strengthen interface controls

• Leverage process automation (e.g. robotics)

• Implement big data and analytics technologies

• Move toward DoD (federal, when appropriate) shared service solutions with standardized

systems, processes, and governance

• Leverage existing FM target system capabilities to consolidate systems with duplicative

and similar capabilities

Related FM Enterprise Initiatives: FM IT systems environment; USSGL/SLOA/SFIS

compliance; FBWT – CASH; PPBE standards; and IGT

Possible Success Indicators:

• Percent reduction of legacy FM business systems

• Percent of source business events entered directly into financial system

• Percent of USSGL, SLOA, and SFIS compliant systems

• Percent of accounting systems that have implemented PRDS/PDS

• Percent of entitlements systems that have implemented PDS

• Percent of accounting transactions that carry trading partner information

• Percent of duplicate master data for suppliers

• Percent of duplicate master data for customers

• Percent of interface exceptions based on historical reconciliations

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

15

• Percent of transactions entered by automated means via business event

• Evidence and proof of interface controls and audit reports

• Number of labor hours saved via automation

GOAL 2 – Develop and strengthen a well-trained financial workforce that has the

knowledge, skills, and abilities to support business reform and auditability in DoD.

1

People are an organization’s most important asset, and there must be a concerted effort to retain

and attract talented leaders and analysts to the DoD FM community.

Expected Business Outcomes: requisite knowledge, skills, and abilities to perform

effectively in all FM career series; closure of identified competency gaps; improved

analytic capability across the workforce; and improved audit and remediation

capabilities.

The DoD Financial Management (FM) Workforce

The DoD FM workforce is comprised of approximately 54K civilian and military personnel of

various FM disciplines. The FM workforce is broadly defined as DoD military and civilian

personnel who perform FM work and are assigned to FM positions. Personnel in FM positions

include military and civilians who perform, supervise, or manage work of a fiscal, financial

management, accounting, auditing, cost or budgetary nature, or work that requires the

performance of FM-related work. The Under Secretary of Defense (Comptroller) (USD(C)) is

responsible for the professional development of the FM workforce. The Financial Management

Office of the Secretary of Defense Functional Community Manager (OFCM) serves as principal

advisor to the USD(C) on workforce development matters and is assisted by the FM Component

Functional Community Managers (CFCM).

The Department has many FM workforce initiatives to further develop and sustain a well-trained

FM workforce that has the requisite FM knowledge, skills, and abilities to effectively meet the

Department’s FM workforce strategic objectives, which are captured in the FY 2019-2023 DoD

FM Strategic Workforce Plan (SWP). The FM workforce provides critical enabling support to

the Department’s FY 2018 National Defense Strategy (NDS) line of effort one (Rebuild military

readiness as we build a more lethal Joint Force), and line of effort three (Reform the

Department’s business practices for greater performance and affordability). The FY 2019-2023

FM SWP is aligned to both lines of effort. The FM workforce supports line of effort one of the

NDS through strategies and initiatives in the OUSD (P&R) Human Capital Operating Plan.

Additionally, the FM workforce supports the Department’s strategic objective 3.3 (Improve the

quality of the budgetary and financial information that is most valuable in managing the DoD).

1

Department of Defense Financial Management Workforce Strategic Workforce Plan FY 2019-2023

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

16

Key initiatives in the FM workforce portfolio align with the guidance in the President’s

Management Agenda (PMA) and the DoD Agency Reform Plan.

The FM workforce strategic initiatives include the FY 2019-2023 DoD FM SWP, an FM

competency gap assessment, a DoD FM Workforce Dashboard, a Department-wide FM focused

developmental assignment program, and the DoD FM Certification Program (DFMCP). These

initiatives are all designed to build and maintain the technical and leadership competence of

individual FM members.

• The FY 2019-2023 DoD FM SWP is a four-year, forward focused document that sets

forth the goals and objectives that will enable the FM Community to recruit, train,

develop, and retain a strong, agile, and responsive FM workforce ready to meet future

Department requirements. The FM SWP was developed collaboratively with FM and

human capital subject matter experts from across the DoD FM Community.

• OUSD (P&R), in collaboration with the DoD FM Community, conducted a

comprehensive competency gap assessment of the DoD FM competencies via the

Defense Competency Assessment Tool. The DoD community, in coordination with FM

subject matter experts, also conducted a revalidation of the DoD FM competencies. All

FM competencies were revalidated. Workforce competency gap assessments are

essential elements in workforce planning, and DoD FM competencies are the foundation

of the FM workforce portfolio. Results from the competency gap assessment indicated

no significant competency gaps in the FM workforce and will be used to inform future

workforce improvement strategies for FM personnel.

• The DoD FM workforce dashboard is a comprehensive visualization and analytical tool

that incorporates Department–wide FM workforce data (workforce demographics,

DFMCP, Federal Employee Viewpoint Survey results, Department-wide FM

training/course data, FM direct hire, and competency assessment data) from various

sources, and provides OUSD(C) and the Components with a decision making tool that

was not previously available. The FM workforce dashboard provides FM leaders with

automated, accessible and reliable data in a very short period of time.

• FM STARs, a developmental assignment program is designed to foster a Strong, Trained,

Agile and Ready (STAR) workforce. The purpose of the program is to provide

opportunities for members of the DoD FM civilian workforce to advance their breadth of

knowledge and experience through three to six month developmental assignments in

other DoD Components. A pilot was conducted in the 4th quarter of FY 2018 and

approval to proceed to a formal program was granted in FY 2019. FM STARs is also an

FM workforce retention tool.

• The DoD FM Community published its first year-in-review, the DoD FM FY 2019 Year-

in-Review, which highlights the accomplishments of the FM Functional Community

relative to functions of the financial management community.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

17

The goal of the FM workforce portfolio is to improve DoD financial management capabilities

through training and development that is focused on DoD FM competencies, to include decision

support and analysis competencies.

The DoD FM Community published its first year-in-review, the DoD FM FY 2019 Year-in-

Review, which highlights the accomplishments of the FM Functional Community relative to

Objective 2.1 – Provide course-based FM training and developmental opportunities in

required FM competencies in support of the DoD FM Certification Program.

The Department has integrated multiple FM development efforts across the DoD into a

mandatory cohesive program that educates, trains, and certifies FM personnel (civilian and

military). The foundational framework consists of 24 enterprise-wide FM competencies, with

associated proficiency levels, and selected leadership competencies. A landmark initiative for

the DoD FM community, the program ensures that the FM workforce has course-based training

in the requisite FM and leadership competencies to prepare them to perform FM functions now

and in the future. This course-based program, known as the DoD FM Certification Program

(DFMCP), began as a pilot in 2013 and is now fully implemented and at steady state.

The DFMCP continues to be the mechanism to ensure that the FM workforce receives required

FM and leadership focused training and development.

Ensuring the FM community has a broad, enterprise-wide perspective, and standard body of

knowledge throughout the Department is important to overall FM workforce readiness. The

Department is working to execute its mission with fewer resources. Budgetary uncertainties

compound the Department’s fiscal challenges and have the potential to negatively affect mission

readiness. To respond to these challenges, the DoD emphasizes a more disciplined use of

resources and strong FM. The Department must make future choices based on timely, accurate,

and reliable data and is focused on preparing for the future by rebalancing defense efforts in a

period of increasing fiscal constraint. This focus, coupled with ongoing audit remediation and

process and data standardization efforts, informs key FM initiatives that seek to address

challenges and strengthen the FM workforce to produce better information for decision-making.

The DoD FM Certification Program:

• Guides FM professional development

• Provides a workforce with the right skill sets

• Establishes a mechanism to encourage key training in:

o DoD audit and remediation

o Decision support and analysis,

• Encourages career broadening and leadership

• Transitions the workforce to a more analytical orientation

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

18

To meet this objective, the Department must:

• Ensure the workforce has the continued opportunity to achieve the required certification

at the appropriate level

• Ensure adequate training sources are available

• Recruit and retain talented individuals for the FM workforce

Related FM Enterprise Initiatives: FM certification

Possible Success Indicators:

• Percent of FM Workforce Members in Good Standing. This metric represents the

percentage of FM members who are compliant in both initial certification and continuing

education training.

• Percent of FM civilian workforce retained

GOAL 3 – Develop a standardized PPBE process that enables E2E funds traceability and

data linkage between planning, budgeting, and execution

The DoD PPBE process determines which programs are funded to meet defense strategy

requirements. The DoD uses the PPBE process to prioritize and allocate resources in alignment

with carrying out the Department’s national security objectives. The FM community contributes

to the PPBE process by translating the Department’s priorities into fiscal requirement by way of

budget formulation and justification, on through apportionment and allocation, and obligation

and execution of monetary resources.

The Department cannot meet national defense objectives without adequate resources. The status

of resources, or lack thereof, directly impacts force development, mission capabilities, and

capacity. The FM community must plan, program, budget and execute prudent and justifiable

budgets that achieve U.S. national defense objectives. This goal ensures that the FM community

ensures adequate resources are available and funding requests do not exceed the minimum

amounts required to meet defense objectives within reasonable risk. The limited resources

entrusted to the FM community from the American taxpayer demands innovative budgetary and

financial stewardship.

Expected Business Outcomes: timely, accurate, and reliable financial data for decision

makers; supportable transactions; E2E funds traceability between budget and

expenditures; and cost effective business environment

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

19

Objective 3.1 – Establish clearer and closer links between prioritized requirements and

program execution

To ensure confidence in the institution’s budgeting system, the Department’s enterprise-wide

PPBE process will yield more transparency by linking expenditure, revenue, and related metrics.

This will facilitate execution reviews of past decisions and actions. Recommendations from

these reviews will be linked to decisions on future resource allocations.

To optimize funding, the DoD needs to develop clearer and closer ties between prioritized

requirements and mission execution. Clear traceability between the budget and execution will

provide critical insight to DoD decision makers when formulating budget requests. Timely,

accurate, and reliable budget and execution data is critical in making resource decisions.

The Department continues its effort toward a standard PPBE process with the implementation of

modern budget formulation systems, EFD, further exploration of the budget capabilities within

DBSs, cost management, and improved E2E procure-to-pay and budget-to-report capabilities to

provide enterprise-wide PPBE visibility.

To meet this objective, the Department must:

• Develop, implement, and enforce data standards (e.g., USSGL/SLOA/SFIS, PRDS, PDS)

• Develop and implement a standard PPBE enterprise-wide process and system; these

include funds distribution, budget planning and submission, cost management

framework, and E2E procure-to-pay capabilities/standards

Related FM Enterprise Initiatives: USSGL/SLOA/SFIS compliance, PPBE standards, funds

distribution (e.g., EFD), cost management

Possible Success Indicators:

• Percent of systems compliant with USSGL/SLOA/SFIS

• Percent of appropriations that use EFD to track to the lowest level of distribution by

budget allotment line item identifier

• Percent of transactions that carry budgetary elements on all transactions without

transformation or crosswalk

• Percent of budget executed at component versus sub-allotted

• Run rate of budget execution across life of appropriation

• Percent of quarterly review variances that are not supported by normal business events

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

20

GOAL 4 – Achieve a sustainable unmodified audit opinion by improving financial

processes, controls, and information via audit remediation

FY 2019 was the second year of a department-wide, full-financial statements audit that included

the MILDEPs and ODOs. More than 24 stand-alone audits were completed, including of the

intelligence organizations, in addition to a consolidated audit of the Fourth Estate. DoD

Inspector General or external auditors issued 3,244 notices of findings and recommendations

(NFRs), including 1,767 NFRs that were repeated or reissued from FY 2018. During FY 2019,

the Department closed over 20 percent of the FY 2018 NFRs. The new, modified, or reissued

NFRs arose from continued or increased testing (in some cases, breadth and depth of testing

increased, while in others a shift from judgmental to statistical sampling occurred). NFRs were

also reissued or modified when CAPs were implemented too late for testing during the FY 2019

audit.

The Secretary of Defense provided strategic audit guidance for the FY 2019 audit to help

prioritize the NFRs and corresponding CAPs and address underlying causes of the disclaimers of

opinions issued for stand-alone audits and the consolidated audit. The FY 2019 audit priorities

include the four areas identified in FY 2018 Real Property, IT (Access Controls), Inventory and

Operating Materials & Supplies (OM&S), and Government Property in the Possession of

Contractors. The FY 2020 priorities added FBwT, Financial Reporting Internal Controls, the

Joint Strike Fighter Program, and Audit Opinion Progression. These areas were selected for

increased attention by the Services, ODOs, and at the consolidated level. As a result, leadership

across the Department involved with these eight areas are working to develop and implement

solutions with a focus on downgrading or removing material weaknesses.

To develop objectives and strategies for fiscal years 2020 through 2024, the Department assessed

the first two years of audit; the material weaknesses identified by the DoD IG, external auditors

and OUSD(C); and their root causes of the identified material weaknesses; and the steps required

across the enterprise to receive unqualified audit opinions by the Services and Components. The

Department is working toward an efficient, sustainable, and auditable business environment that

demonstrates good stewardship of taxpayer funds. Corrective actions that provide the most value

to the warfighter are the priority. For more information regarding the Department’s audit

strategy, please refer to the DoD Consolidated Audit Strategy

2

.

Expected Business Outcomes: auditable business environment; timely, accurate, and

reliable property, inventory, and financial data for decision makers; supportable

transactions (eliminations); reduced reconciliation work (daily FBWT reconciliation, JVs,

open obligations, etc.); improved interoperability between systems; stronger internal

2

http://comptroller.defense.gov/FIAR.aspx

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

21

controls; strengthened mission capabilities; enhanced stewardship and public trust; and

unmodified audit opinions.

Objective 4.1 – Achieve an unmodified financial statement audit opinion

The Department is marching toward achieving an unmodified full financial statement audit

opinion. The OUSD(C), MILDEPs and ODOs are prioritizing initiatives and resources as part of

audit remediation. The Department’s objective is to receive an unmodified audit opinion and

institute sound FM practices to safeguard taxpayer dollars and improve analytical capabilities.

To meet this objective, the Department must:

• Accurately account for all Real Property (buildings and structures) and Inventory as well

as Government-property in the possession of contractors and the Joint Strike Fighter

Program.

• Develop and reconcile a universe of transactions including sensitive activities

• Execute successful reconciliation of FBWT

• Support unsupported JVs as well as work toward eliminating system and manual JVs that

could be supported by transactional detail

• Comply with the USSGL, SLOA, and SFIS

3

to align with federal data standards and

controls to improve support of open obligations; existence, completeness, and rights and

obligation of assets; valuation of assets; and environmental and disposal liabilities

• Follow Generally Accepted Accounting Principles (GAAP)

• Implement U.S. Treasury’s IGT solution, G-Invoicing, to support eliminations

• Provide a capable and sustainable audit infrastructure

• Resolve material weaknesses and ensure effective implementation of CAPs

• Provide standard E2E business process documentation

Related FM Enterprise Initiatives: FM IT systems environment, FBWT – CASH, ADVANA,

property, JVs, sensitive activities guidance, and IGT

Possible Success Indicators that will increase the number of DoD organizations with

unmodified audit opinions:

• Percent of transactions are reconciled to general ledger systems

• Percent of transactions are reconciled from feeder source systems to the general ledger

• Percent of Component Trial Balances reconciled to Principal Financial Statements

• Decrease in percent of abnormal balances

• Increase in percent of dollars reconciled to Treasury (Statement of Differences and Cash

Management Report)

3

http://dcmo.defense.gov/Products-and-Services/Standard-Financial-Information-Structure/

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

22

• Decrease in percent of overaged undistributed transactions (in-transit and unmatched)

• Decrease in overaged transactions in suspense accounts

• Validation of deposit fund activity

• Improved distribution of aged payables

• Improved distribution of aged receivables

• Decrease in aging of unfilled customer order balances

• Decrease in aging of unliquidated obligation balances

• Decrease in percent of negative accounts payable

• Decrease in percent of unsupported JVs

• Increase in percent of journal voucher root cause analysis, followed by corrective actions

(i.e. correcting the posting logic)

• Increase in percent of supportable financial statement lines by compliant business process

versus journal adjustment

• Mission critical assets existence and completeness baseline for general equipment, real

property, internal use software, and inventory and operating material and supplies

• Reduction in dollar amount and percent of adjustments after physical inventory counts

• Increase in dollar amount and percent of inventory reconciled between DLA and the

Services

• Increase in percent of total dollar amount of supported eliminations

Objective 4.2 – Continually strengthen compliance with financial management laws,

regulations, policies, and internal controls

The Department is committed to responsible stewardship of its resources and continues to focus

efforts on strengthening processes to comply with FM laws, regulations, policies, and internal

controls. Senior leadership’s posture, also referred to as ‘tone at the top,’ toward internal

controls sets the tone throughout an organization and establishes a culture of awareness as to

how leadership views its mission and objectives. When senior leadership demonstrates that

strong internal controls are critical to the entity’s function and operation, this attitude permeates

throughout the organization. MILDEPs and ODOs must implement and maintain strong internal

controls. The following areas are critical and require management attention and accountability:

• Governance

• Policy and procedures

• Training

• Fraud risk assessment and prevention

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

23

• IT general controls (e.g., SSAE No. 18

4

and Federal Information System Controls Audit

Manual (FISCAM))

5

• NFR tracking

• Office of Management and Budget (OMB) Circular No. A-123

6

• OMB Circular A-136

• Chief Financial Officers Act of 1990

• Government Management Reform Act

• Government Performance and Results Act

• Statement of Assurance process

• USSGL, SFIS, and SLOA compliance

• Federal Financial Management Improvement Act of 1996 (FFMIA)

• E2E process documentation

• Digital Accountability and Transparency Act of 2014 (DATA Act) implementation

To meet this objective, the Department must:

• Focus upon achieving and sustaining a strong internal control program (without which

the Department will not be able to obtain and sustain an unqualified audit opinion)

• Tighten IT security measures so systems safeguard sensitive data from unauthorized

access and misuse

• Maintain complete, accurate, and up-to-date E2E process documentation Department-

wide and at individual reporting-entity levels

• Maintain documentation and adhere to controls that help auditors understand entity-level

controls, control environment, control objectives, and detailed business processes across

the Department

• Achieve and maintain unmodified SSAE 18 audit opinions

• Standardize and comply with DoD guidance, data standards, and business rules

• Resolve critical NFRs and complete CAPs

Related FM Enterprise Initiatives: USSGL/SLOA/SFIS compliance; sustaining an auditable IT

systems environment; and DATA Act.

4

SSAE No. 18 is an attestation standard put forth by the Auditing Standards Board (ASB) of the American Institute

of Certified Public Accountants that addresses engagements undertaken by a service auditor for reporting on

controls at organizations (i.e., service organizations) that provide services to user entities, for which a service

organization's controls are likely to be relevant to a user entities internal control over financial reporting.

5

The FISCAM presents a methodology for auditing information system controls in federal and other governmental

entities. This methodology is in accordance with professional standards.

6

OMB Circular No. A-123 defines management's responsibility for internal control in federal agencies. A

re-examination of the existing internal control requirements for federal agencies was initiated in light of the new

internal control requirements for publicly-traded companies contained in the Sarbanes-Oxley Act of 2002. Circular

A-123 and the statute it implements, the Federal Managers’ Financial Integrity Act of 1982, are at the center of the

existing federal requirements to improve internal control.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

24

Possible Success Indicators:

• Increase in the number of shared service providers with unmodified SSAE 18 opinions

• Increase in the number of accounting systems compliant with USSGL/SLOA/SFIS

• Increase in the number of accounting systems compliant with FFMIA

• Increase in the number of feeder systems compliant with USSGL/SLOA/SFIS

• Increase in the percent of obligations and outlays dollars submitted by object class and

program activity (DATA Act)

• Increase in the percent of obligation dollars submitted by award ID (DATA Act)

GOAL 5 - Maximize the use, extent, and performance of the Department’s Defense

Business System(s) capabilities where practicable and economically feasible; minimizing

the population of systems and resources required to satisfy the mission of the FM

community, to include increased cooperation and coordination among business system

owners to facilitate timely and effective transformation.

The Department’s FM information system technology landscape is one of significant complexity

and investment. The FM landscape is comprised of over 340 financially relevant accounting and

business systems representing a total spend of $16.2 Billion in the Fiscal Years Defense Plan

(FYDP) 2020-2024. At the same time accounting and feeder systems are undergoing planned

migrations, the Department is seeking to achieve a favorable audit opinion. Together, these

factors present the Department with an unprecedented opportunity to simultaneously address both

functional and IT requirements with potential cost avoidance and savings if an integrated and

collaborative business transformation approach is taken.

Expected Business Outcomes: optimized use of DBS FM functionality, shared services,

streamlined end-to-end processes and controls, reduced reliance upon non-DBS,

deployment of a federated master data management model.

Objective 5.1 – Define Accounting and Feeder System Target End State

The DoD spends a significant amount of money on its accounting and financially relevant

business systems, operations, and reporting. These systems account for numerous accounting

and control deficiencies which results in unreliable financial and operational information.

Process-related system integration gaps and inconsistent implementation of financial data

standards (FDS), to include the SFIS, are inherent issues throughout the complex environment of

FM-related systems, along with an ineffective enterprise-wide governance structure.

The Department must define its accounting and feeder system target end state in order to

transform its complex systems and data environments into a target state that ultimately results in

reliable financial and operational information.

To meet this objective, the Department must:

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

25

• Establish an integrated, multidisciplinary work group team of Department stakeholders to

define a DoD-wide DBS target end state for FM capabilities that federates all DoD master

data and consumes transactional data to perform real-time data analytics and reporting.

• Define accounting and feeder systems target end state. Develop a target end state

operating model, promoting transitioning of accounting systems to designated DBS,

eliminating where practicable, the current population of 341 financially relevant business

feeder systems. The model must capture the common E2E capabilities of the six DBSs,

Treasury Shared Services, and the federated FM and master data management

capabilities.

• Take the approach feeder system transactions will orginate from the enduring DBSs,

except H2R prcess

• Designate a single-source DBS be utilized for all funds (General Fund, Working Capital

Fund, and Transactional fund)

• Mandate policy changes and BPR are implemented first before customizing a system

• Outsource where appropriate to a federally shared service provider (e.g. Treasury Shared

Services)

• Create data once and replicated it many times; establish one authoritative source for each

unique business master data source, and establish a single location for all transactional

data

• Implement enhanced tiered accountability structure/tiered data governance structure

• Refrain to the extent possible, customization in the current and future DBS

The target end state needs to reflect a simplified DBS landscape which leverages modern and

advanced technologies – facilitated through business, IT system, and vendor integration – to

deliver both functional and compliant system capabilities, managed by a robust cross functional

governance structure, leveraging the federated FM capabilities and master data approach.

Through integrated and enhanced business process reengineering (BPR), the consolidated system

landscape reduces the cost of compliance while also increasing enterprise visibility, reporting

and analytic capabilities.

Related FM Enterprise Initiatives: USSGL/SLOA/SFIS Compliance, FBWT, IGT, ADVANA,

Property, JVs, Financial Management Information Technology Systems Environment, Funds

Distribution, Cost Management, PPBE Standards (Procure-to-Pay), DATA Act, and TDD.

Possible Success Indicators:

• Percent reduction of systems within the Department FM mission portfolio(s);

identification of “savings/avoidance” contributing to organizational resource

management decisions

• Percent of FM-related functionality utilized in core DBSs

• Reduction of point-to-point interfaces, and related cost savings/avoidance

• Reduced number of system data configuration and control audit findings

• Reduced costs associated with auditing due to fewer systems

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

26

Technology Benefits

• Optimized IT staffing through reduced system footprint

• Simplified IT solution, by streamlining and/or standardizing business processes

• Visibility into data from MILDEPs and 4th Estate, enabled by single integrated enterprise

reporting and analytics capability

• Increased internal control quality and enforcement of authoritative source master data

• Reduced extensive redundant systems and points of combatant access

Enterprise / Business Benefits

• Master data harmonization; enablement of centralized process execution and reporting

• Right-time data reporting and analysis enabled by speed of in-memory processing

capability

• Reduced long-term costs associated with parallel and redundant systems to include

development, testing, operations & support, sustainment costs

• Ability to develop enterprise solutions for complying with Laws, Regulations, and

Policies (LRPs)

• Streamlined and/or standardized business processes

• Robust Governance Model with configuration control board accountability

• Resolved gaps and inconsistencies in the current stove-piped DoD business domains’

data standards

FM Benefits

• Improved traceability/internal controls by simplifying and consolidating business

processes and data flows

• Increased implementation of FDS; improving data quality in both core accounting &

feeder systems

• Improved decision support, enabled by OSD-owned enterprise BI capability

• Streamlined and standardized FM & business processes

• Lowered cost of financial / business operations and reduces footprint for IT/FM

remediation

• Reduction / elimination of system "handshakes" and required internal controls

• Lowered E2E business process complexity

• Reduced number of cross walks between systems

• Reduced number of supported and unsupported JVs

Objective 5.2 - Develop Defense Business Systems Financial Management Roadmap

The FM systems target end state requires a transformation roadmap (Figure 6) that captures the

prioritization of movements to transform the current governance structure, implementation of

Federated FM capabilities and the master data management approach, and transition of legacy

accounting and financially relevant business systems.

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

27

The DBS FM Roadmap, aka ‘enterprise roadmap,’ must embrace the collaborative opportunities

that this transformation journey presents. The enterprise roadmap will capture the enterprise-

focused target operating model, which leverages core capabilities, reducing costly customization.

The target operating model will include a transition phase for implementing courses of action.

Within every Chart of Account (CoA) series, the following components exist:

• Governance – Comprised of strategic and operational governance that sets the vision,

ensures value delivery, and aligns organizational and functional requirements, along

with IT services, to the DoD FM objectives. Also, identifies the specific controls that

are in place to manage the in-scope portfolio of systems, mitigate operational and

financial risks, and provide governance to manage data, processes and other assets.

• Process – For FM capabilities and systems, outlines how specific process steps are

related to system-specific OAs, organizational and functional roles and responsibilities.

• Technology – The foundational tools and capabilities that are at the core of the

transformation.

Figure 6 – “Notional” Defense Business Systems FM Transformation Roadmap

To meet this objective, the Department must:

• Collaboratively leverage, to the extent practicable, Department-wide opportunities

towards shared services environment, standardized data standards and systems

configuration, and governance themes as key contributing factors in developing the core

enterprise systems roadmap

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

28

• Maximize use of FM functionality inherent in core enterprise systems, hence, minimizing

a ‘need’ for non-core enterprise systems solutions

• Establish a transformation implementation governance structure to manage the enterprise

system roadmap

Related FM Enterprise Initiatives: USSGL/SLOA/SFIS Compliance, FBWT, IGT, ADVANA,

Property, JVs, FM Information Technology Systems Environment, Funds Distribution, Cost

Management, PPBE Standards (Procure-to-Pay), DATA Act, TDD

Possible Success Indicators:

• Approved Department enterprise business FM systems roadmap

• Percent reduction of systems within the Department FM mission portfolio(s)

• Actual dollars identified as “savings/avoidance” resulting in an approved resource

management decision

• Reduction of point-to-point interfaces and identification of associated fiscal resources

• Reduced number of system control audit findings

• Reduced costs associated with auditing fewer systems

Section 2. Financial Management Enterprise Initiatives

OUSD(C) developed 12 critical FM Enterprise Initiatives to achieve and sustain the target state.

These initiatives also directly support audit remediation and will evolve and be refined overtime.

FM Enterprise Initiatives:

• ADVANA (formerly, Universe of Transactions (UoT)

• USSGL/SLOA/SFIS Compliance (Reform Initiative)

• FBWT – Cash Accountability and Traceability

• IGT

• Property

• JVs

• Financial Management Information Technology Systems Environment

• Funds Distribution

• Cost Management

• Planning, Programming, Budgeting and Execution Process Standards

• DoD Financial Management Certification Program (DFMCP)

• DATA Act

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

29

The FM Functional Strategy Target Equation, as shown in Figure 7, is the framework used to

achieve the target FM environment and should be used when executing the FM strategic

initiatives. Each organization must optimize those variables most critical and material to them to

reach the target state. If the FM community performs business correctly, the outcome will be a

sustainable, data-driven, and auditable business environment.

Figure 7 – FM Target Equation

1. ADVANA (formerly, Universe of Transactions)

Due to the number of and complex amount of systems with the Department, it has been a

challenge to not only identify and define a complete population of transactions, but also

reconcile these transactions to the Department’s financial statements. This is necessary not only

to be in compliance with the DATA Act, but also to achieve auditable financial statements. To

overcome these challenges, the OUSD(C) DCFO developed the ADVANA platform. The

purpose of ADVANA is to create a central repository for the DoD’s vast FM data in order to

define a complete UoT and use this universe to inform FM decision making and remediation

efforts. As of the end of FY 2019, ADVANA is ingesting data from over 100 systems and

standardizing the data using a common data taxonomy.

To support a financial statement audit, the Department requires, at a minimum, the following

capabilities within the ADVANA platform:

• Proof of the existence of all data contained within the financial statement balances

• Proof of the completeness of all transactional data reported within the feeder systems

• Ability to extract a subset population bound by desired attribute(s) including the processes

and controls applicable to the subset population

• Ability to secure, maintain proper access, and protect the data within the ADVANA platform

To date, the ADVANA platform has been a successful undertaking and has demonstrated

measurable benefits, including:

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

30

• Standardized financial data across the DoD in order to complete reconciliations and perform

Department wide analytics

• Provide all audit workbook reconciliations for the TI-97 consolidated audit, as well as Tier 2

entities

• Provide an auditor the ability to sample TI-97 financial transactions across the entire

Department

• Undertaking the UoT solution for both the Army and Navy

• Develop Financial Statement Drilldown capability, to include Unadjusted to Adjusted Trial

Balance reconciliation for the Department

• Become the official TI 97 FBWT Reconciliation tool

• Deployed an enhanced obligations monitoring tool to identify accounts at risk of expiring

and cancelling in support of the new DAR-Q process

• Deployed the NFR and CAP database

• Improved analytic and root cause capabilities where users can move easily between

summarized balances and detailed transactions

• Develop FM monitoring dashboards and tracking metrics to include JVs, Tie Points and

Abnormal Balances

• Simplification of the analytic infrastructure, with fewer moving parts to configure and

manage

• Reduced development and analytic processing time

• Potential to reduce current financial reporting systems that leverage the same data set

Finally, by using the FM audit requirements as the gateway, ADVANA has further evolved into

the DoD enterprise analytics shared service provider with the mission of providing enterprise

business insights to include, budget, cost analysis, contracts, and more. By building the

capability on a standard open source platform, the solution is portable to the DoD cloud

architecture.

FY 2019 ACHIEVEMENTS

• Supported three FY2019 audits (SOCOM, DHP, and Tier 3 & 4)

• On boarded Army and Navy Financial Management offices to support the FY20 Audit

• Ingested over 11 billion transactions

• Added over 5,000 users

• On boarded all DoD to the NFR/CAP database

• Operationalized over 50 TI-97 Feeder Reconciliations

• Expanded the DAR-Q user base and enhanced functionality to support larger services such as the Navy and

Marine Corps

BUSINESS OUTCOMES

CHALLENGES

RISKS

• Consolidated audit portfolio

• Unmodified audit opinion

• E2E funds traceability between

budget and execution

• Timely, accurate, and reliable

data for decision makers

• Budget constraints increase risk

to audit remediation timelines

• System change requests need to

be developed/approved to

achieve capability

• Inability to gain clean audit

opinion on DoD financial

statements

• Inability to trace source

transaction to the USSGL

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

31

• Reduced reconciliation work

• Adoption of DoD-wide

ADVANA solution over

individual tools

MITIGATIONS

DEPENDENCIES

• Undergoing SSAE 18 audit in FY2020

• Utilize inherent DBS transaction traceability

wherever possible

• Non-compliant systems and data should utilize GEX

translation services

• USSGL/SLOA/SFIS system compliance

• Reduction in legacy systems

• Consolidation DoD accounting systems

Table 1 – ADVANA Overview

2. USSGL/SLOA/SFIS Compliance

The purpose of this initiative is to ensure all DoD FM systems comply with the DoD SCOA and

USSGL, which are the foundation for the DoD FM target environment. SFIS is the

Department’s common financial business language that standardizes data elements, business

rules, and the transaction posting logic used in DoD financial systems. To establish data

standards between trading-partner systems, the MILDEPs and ODOs are implementing a single

SLOA and accounting classification to all applicable transactions. In time, the use of SLOA will

improve interoperability between systems, and help reduce the need for systems interfaces via

use of the SLOA data exchange, leveraging the Standard Transaction Broker. This will improve

controls and assist financial managers and auditors with tracing transactions across multiple

systems. The OUSD(C) Office of the Deputy Chief Financial Officer (ODCFO) will assess key

FM systems and data exchanges to help ensure compliance with standards.

FY 2019 ACHIEVEMENTS

• Reviewed all audit NFRs to determine effect of SFIS / SLOA on Department financial statement auditability.

• Developed cost model to project likely future costs for Audit NFRs based on SFIS / SLOA non-compliance.

• Reviewed all SFIS compliance assessments to determine enterprise SFIS / SLOA compliance trends.

• Continued SFIS compliance assessment testing for select target accounting systems.

BUSINESS OUTCOMES

CHALLENGES

RISKS

• Unmodified audit opinion

• E2E funds traceability between

budget and execution

• Improved interoperability

between systems

• Timely, accurate, and reliable

data for decision makers

• Reduced reconciliation work

• Supportable transactions

• Legacy systems are antiquated

and it would be too costly to

upgrade them to

USSGL/SLOA/SFIS compliance

• Systems become compliant at

different times creating a

“hybrid” environment; this

degrades interoperability

between systems

• System change requests need to

be scheduled and developed to

achieve compliance

• Inability to transform legacy

data to be compliant

• Inability to gain clean audit

opinion on DoD financial

statements

• Insufficient accountability of

DoD resources

• Continued information system

control weaknesses

• Failure to implement common

business language resulting in

component-level financial

statements and/or DoD-level

financial statements to have

inconsistent data

• Systems may be recording

transactions incorrectly and

reporting incorrectly

MITIGATIONS

DEPENDENCIES

DoD Financial Management Functional Strategy for Fiscal Years 2020-2024

32

• OUSD(C) monitors FIAR activity to assess and migrate

risk to achieve unmodified audit opinion; using the FIAR

governance process as a mechanism to review solutions,

best practices, and other remedial actions

• Conduct business-process re-engineering to eliminate

legacy systems that are not capable of being

USSGL/SLOA/SFIS compliant

• For systems that are USSGL/SLOA/SFIS compliant,

ensure there is a plan to maintain compliance to

USSGL/SLOA/SFIS updates on at least an annual basis

• Resource material FM systems to be SFIS compliant

• Non-compliant systems and data should utilize GEX

translation services

• Utilize inherent DBS transaction traceability wherever

possible

• DoD-wide participation is needed to achieve

an unmodified audit opinion

• Proper planning between the FM community

and the system Program Management Offices

(PMO)

• GEX translation capabilities availability for

legacy systems and data

• Reduction of legacy systems

• Defense Repository for Common Enterprise

Data (ADVANA) for continuous compliance

monitoring.

• Treasury’s USSGL is updated annually; DoD

reporting CoAs and transaction library is

updated afterwards to ensure compliance

Table 2 - USSGL/SLOA/SFIS Overview

3. Fund Balance with Treasury – Cash Accountability and Traceability

FBWT is an asset account that shows the available budget spending authority of federal

agencies. Appropriation warrants (new budget authority generally received annually), non-

expenditure transfers (budget authority given from one agency to another), collections,

disbursements, and related adjustments reported to the Treasury may increase or decrease the

FBWT account balance. Treasury requires that agencies reconcile their FBWT account on a

regular and recurring basis to ensure the integrity and accuracy of their internal and government-

wide financial reporting data. The DoD Components must reconcile their records of available

budget spending authority to Treasury. Each reporting entity must be able to perform a detailed

reconciliation of the balances to the source systems and accounting records. These

reconciliations are essential to supporting the budget authority, outlays, and cash reported on

their Statement of Budgetary Resources and Balance Sheet. During the recent independent audit

of the DoD, the auditors noted several deficiencies in the design and operation of internal

controls for FBWT that resulted in a DoD-wide material weakness. Currently, the Department is

unable to ensure the completeness and accuracy of its FBWT account. Unreconciled variances

and unsupported adjustments to FBWT seriously undermine the integrity and reliability of

DoD’s financial statements. While important for audit, cash balance is more importantly the

foundation of good business practices.

3A Daily FBWT Activity – Cash Accountability and Traceability (CASH)