SECTION I: INITIAL STATEMENT BY BANK OF AMERICA PURSUANT TO SECTION E.1.b OF THE BUREAU’S

POLICY ON NO-ACTION LETTERS

Bank of America, N.A. (“Bank of America”) hereby submits this application for a No-Action Letter

(“NAL”) based on an existing NAL Template approved by the Consumer Financial Protection Bureau

(“Bureau”). On May 22, 2020, the Bureau granted the Bank Policy Institute’s (“BPI”) application (the “BPI

Application”) for a NAL Template (the “BPI NAL Template”).

1

BPI sought a NAL Template that could serve

as the basis for NAL applications by BPI members and other deposit-taking institutions that intend to

offer certain small-dollar credit products. Bank of America, in its capacity as a deposit-taking institution,

hereby applies for such a NAL.

Section II of this application provides a description of the structure and features of Bank of

America’s small-dollar credit product, including the information required under the Information about

Features and Practices section of the BPI NAL Template. Section III of this application includes the

certifications set forth in the Guardrail Certifications section of the BPI NAL Template.

SECTION II: BANK OF AMERICA’S APPLICATION FOR A NO-ACTION LETTER PURSUANT TO SECTIONS A

AND E.1.b OF THE BUREAU’S POLICY ON NO-ACTION LETTERS

1. The identity of the entity applying for the No-Action Letter

Bank of America submits this application for a NAL (“Application”)

2

under sections A and E.1.b of

the Bureau’s Policy on No-Action Letters (“Policy”) and based on the BPI NAL Template.

3

Bank of

America submits this Application because it strongly agrees with BPI’s beliefs that (i) consumers would

benefit from the re-entry of deposit institutions such as Bank of America into the small-dollar product

space

4

; and (ii) the additional regulatory certainty provided by a NAL would facilitate Bank of America’s

ability to issue new and innovative small-dollar credit products.

2. A description of the consumer financial product or service in question, including (a) how

the product or service functions; (b) the terms on which it will be offered; and (c) the

manner in which it is offered or provided, including any consumer disclosures.

Bank of America has designed a small-dollar credit product, currently referred to as “Balance

Assist,” the structure and features of which would be consistent with each of the guardrails set forth in

the BPI NAL Template (“Product” or “Balance Assist”).

1

https://files.consumerfinance.gov/f/documents/cfpb_bpi_no-action-letter.pdf.

2

The Application includes the instant document as well as Appendix A (Product Terms and Conditions) and Appendix B (Digital

Marketing and Application Materials). Many of the features of the Product (defined in section II.2) detailed in the instant

document are also included or illustrated in Appendices A and B. Although Appendix A includes terms setting forth remedies

upon an event of default, Bank of America is not seeking to include its debt collection practices in connection with Balance

Assist within the scope of the requested No-Action Letter.

3

We note that, as an insured depository institution with total assets of more than $10,000,000,000, Bank of America is an

eligible “DI Applicant” for purposes of the BPI NAL Template.

4

See also Interagency Lending Principles for Offering Responsible Small-Dollar Loans, available at https://www.occ.gov/news-

issuances/news-releases/2020/nr-ia-2020-65a.pdf in which the Board of Governors of the Federal Reserve System, the Federal

Deposit Insurance Corporation, the National Credit Union Administration, and the Office of the Comptroller o f the Currency

state they are issuing the principles to encourage supervised banks to offer responsible small -dollar loans and recognize the

important role of such loans.

Balance Assist was designed for Bank of America checking account customers with the goals of

(i) providing an affordable banking solution for short term liquidity needs; (ii) providing a streamlined

digital only small-dollar credit product; and (iii) expanding consumer access to credit. Consistent with

the way Bank of America has developed other consumer products, Balance Assist was developed with

input from consumer advocates, other third parties, and our National Community Advisory Council

(“Council”). The Council, in place for more than a decade, is a forum for senior leaders from social

justice, consumer advocacy, community development, environmental, and research organizations to

provide external perspectives on our business policies, practices, and products, as well as the societal

challenges faced by our customers. Our Council members provide valuable insights that continue to

enhance the fairness and transparency of the products and services we provide to our customers.

Balance Assist aligns with Bank of America’s vision of delivering products and services that

improve its customer’s financial lives. The Product would complement Bank of America’s award-winning

mobile banking, spending and budgeting tools, and financial education program Better Money Habits

5

–

all of which can help customers better manage their money and improve their financial know-how so

they can achieve their goals.

Product Structure: Dollar Amount, Annual Percentage Rates (“APR”), Fees, and Collateral

The Product will be structured as a fixed term, amortizing small-dollar installment loan which

the customer will pay back in fixed minimum payments over the term of the loan, which will be three

months. The Product will be offered in increments of $100 up to $500. The customer will be charged a

$5 flat fee regardless of amount borrowed (“Product Fee”). This Product Fee will be clearly disclosed to

the customer, and will be included when calculating the Product’s APR.

6

Other than the Product Fee,

there will be no other fees charged on the Product. The APR of the Product across the anticipated term

of the loan will in no case exceed 36%.

The customer will not be required to provide collateral or other security to obtain the Product.

Consistent with footnote 8 of the BPI NAL Template, Bank of America will maintain a right to setoff

consistent with applicable law and regulation and the Product terms and conditions (“Product Terms”).

7

By offering a small-dollar credit option at an APR below 36% with no late payment or

prepayment penalty fees, Bank of America would significantly improve the market options available to

customers facing short term liquidity needs as, according to sources cited in the BPI Application, many

payday loans currently available carry APRs of as much as 300% to 500%.

Eligibility and Underwriting

The Product will be offered and provided only to consumers who have a Bank of America

checking account (excluding Bank of America’s Advantage SafeBalance account).

8

The customer must

5

Better Money Habits is an easy-to-understand resource available on bettermoneyhabits.com in English and Spanish. It was

developed in partnership with nonprofit Khan Academy, a leader in online education, to provide individuals and families tools ,

videos, articles and infographics to help build financial know-how to achieve their goals.

6

The APR calculation is based on the borrowed amount and the Product fee. Example: a $300 loan with a $5 Product fee along

with a repayment term of three months will result in a 9.97% APR.

7

See Appendix A for additional information.

8

The SafeBalance product launched nationally in May 2014 and was designed to help customers spend only the money they

have available. Transactions are declined and returned unpaid when there are not sufficient funds available to the cover the

transaction. No overdraft or non-sufficient fees are charged on this account.

have a Bank of America checking account for a set period of time with inflows exceeding a pre-

determined threshold in order to be eligible for the Product. Bank of America’s underwriting and

eligibility criteria for the Product will consider the customer’s transaction activity in the customer’s Bank

of America deposit account(s) (e.g., amount of direct deposit and/or inflows, length of time customer

has held the Bank of America deposit account(s)). Additionally, Bank of America will obtain a full credit

bureau report on the consumer and will consider external factors (e.g., delinquencies, bankruptcies,

foreclosures, repossessions) in its underwriting. Bank of America will also obtain the consumer’s FICO

credit score, which must meet a minimum threshold. The digital nature of the product will generally

allow for customers to receive an application decision the same day.

9

Repayment Term and Structure

The Product’s repayment structure will be clearly disclosed. The customer will repay the amount

advanced plus the Product Fee in three substantially equal fixed minimum amount monthly installment

payments.

10

The repayment term will be three months, with the first payment due generally 30 days

after the loan funds are deposited in the consumer’s Bank of America deposit account. The payments

will be amortized on a straight-line basis across more than one payment.

The repayment amounts and payment schedule (“Repayment Information”) will be provided to

the customer in several ways. First, the Repayment Information will be presented to the customer in the

digital application flow before they accept the approved Balance Assist. Second, the Repayment

Information will be populated into the Product Terms presented to and accepted by the customer.

Third, information including first payment amount and due date will be provided to the customer in an

email. Finally, the customer can access the Repayment Information in mobile and online banking at any

time.

The Product design includes features to help customers make payments on time. When applying

for the Product, customers will be given the opportunity to set up automatic payments from a Bank of

America deposit account. Auto-payments would not be required, but would be offered as a feature to

make scheduling payments easier. Additionally, email alerts will be sent to customers when payments

are coming due or are past due.

If the customer attempts to make a payment on the Product from the customer’s Bank of

America checking or savings account, but the customer does not have sufficient funds in that account

(or in any applicable Overdraft Protection plan

11

) to make the payment, Bank of America will waive the

Overdraft Item Fee or NSF: Returned Item Fee that is incurred for the payment or attempted payment of

the Product.

12

The customer will remain responsible for making the payment. This will help towards

limiting a customer’s incremental indebtedness as a result of payments to this Product.

9

Exceptions may apply, such as customers who have placed a “freeze” on their credit file.

10

The installment payments may vary by $0.01 depending on the total loan amount.

11

Overdraft Protection is an optional service through which customers can link their eligible Bank of America checking account

to another Bank of America deposit, credit card, or line of credit account to help them avoid declined or returned transactions

and overdrafts. If a linked Overdraft Protection plan is utilized to cover a transaction, including a payment on the Product,

transfer fees may apply. Overdraft Protection transfers from a line of credit or credit card may be subject to additional fees and

accrue interest.

12

In the event such an Overdraft Item Fee or NSF: Returned Item Fee is not automatically waived, the fee will be refunded to

the impacted deposit account by Bank of America generally within 2 complete deposit account statement cycles.

There will be no late payment fees or prepayment penalty associated with the Product. By not

imposing any prepayment penalty fees, the Product design encourages repayment. As set forth in the

Product Terms, customers who prepay will not be entitled to a refund of a part of the Product Fee.

Rollovers and Re-borrowing Risk Mitigation

Rollovers will be prohibited. In addition, Bank of America will mitigate re-borrowing risk by

requiring the Balance Assist loan to be fully repaid before another Balance Assist loan can be obtained.

Additionally, Bank of America will impose a cooling off period from the date of closure of one Balance

Assist loan to the approval for another Balance Assist loan.

13

These re-borrowing restrictions will be

communicated to customers in the Product overview page, and will be presented to and accepted by

the customers as part of the Product Terms.

Delivery Channels, Marketing and Servicing

The Product will only be available digitally. This will allow for quicker access to small-dollar

credit for consumers who rely on short-term small-dollar credit products to meet their short-term

liquidity needs and to pay for larger, unanticipated expenses. The Product will also expand access to

credit for all consumers, including the underbanked population, as customers will not be required to

visit financial centers. The digital-only nature of the Product will be a significant benefit for those

customers who may have difficulty accessing traditional banking channels or who have a greater need

for small-dollar credit. Customers who visit a Bank of America financial center or reach a Bank of

America contact center will be guided to apply for the Product digitally.

The Product will be marketed through Bank of America’s various digital channels.

14

It will be

featured on the Bank of America checking product online research pages in both the mobile and online

platforms. Information about the Product may be presented to customers during their authenticated

online experience.

The Product will be serviced by Bank of America, and not a third party servicer.

Application Process/Disbursement of Funds

A customer can apply for the Product via mobile or online banking through a digitally optimized

and streamlined application which will be available in English and Spanish.

15

The application will adhere

to Web Content Accessibility Guidelines (“WCAG”). Because the customer accesses the Product

application after being authenticated on the Bank of America mobile or online platform, the information

the customer must enter to apply for the product will be limited.

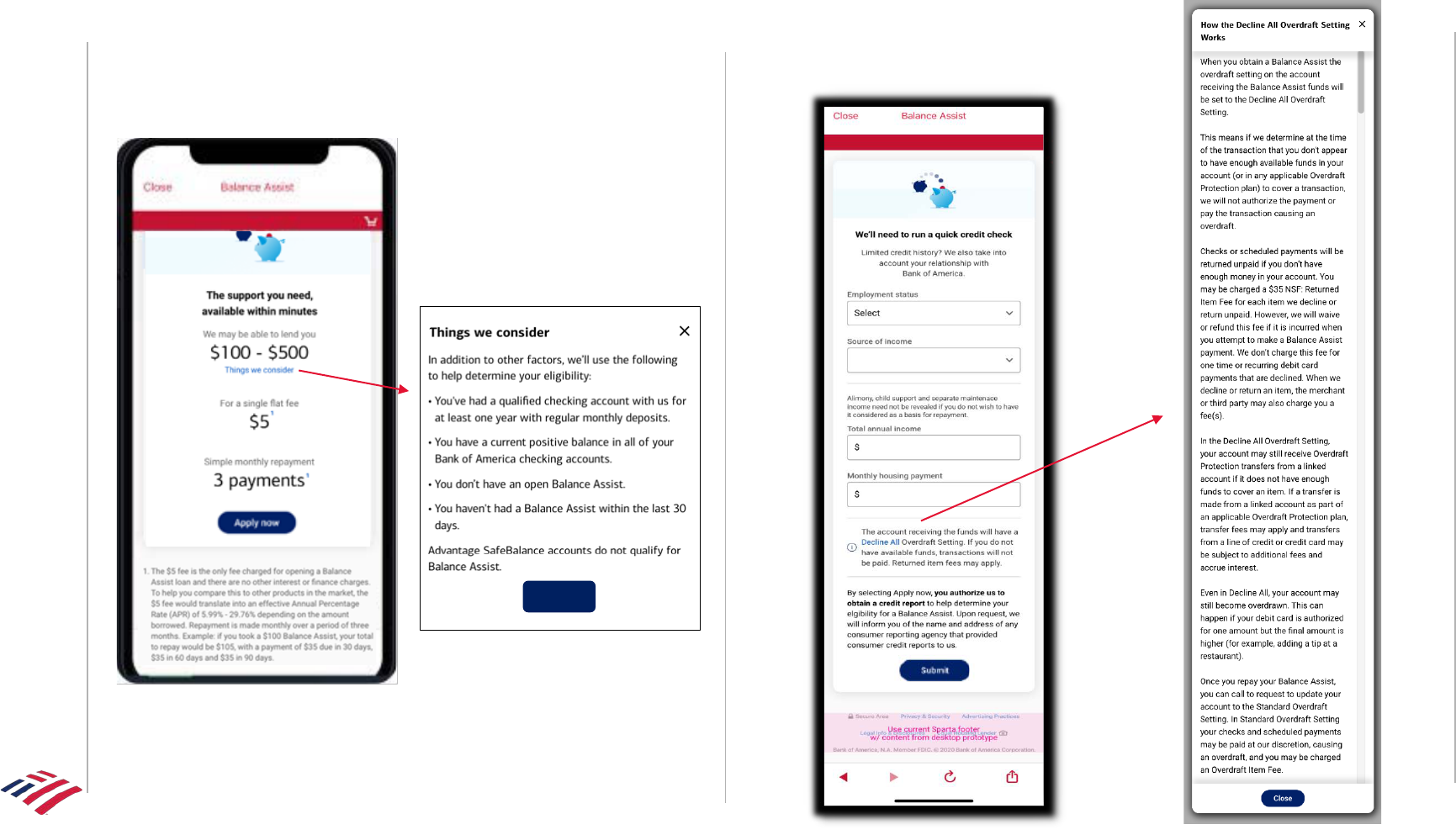

In the Product application flow, the customer will: (i) provide income and housing payment

information; (ii) authorize Bank of America to obtain the customer’s credit report; (iii) select the loan

amount (up to a maximum amount determined by Bank of America pursuant to its underwriting

criteria)

16

; (iv) select the Bank of America deposit account that will receive the loan funds (“Receiving

13

The imposed cooling off period will be 30 days.

14

See Appendix B for additional information.

15

See Appendix B for additional information.

16

For example, the customer may qualify for lower than the maximum loan amount of $500.

Account”)

17

; (v) learn how the Receiving Account will be set to the “Decline All” overdraft setting (as

further described below in the “Other Features and/or Practices” section); (vi) be presented with and

required to accept the Product Terms; and (vii) be presented with the option to set up automatic

payments.

Product Terms will be presented digitally and optimized for readability in the online and mobile

channels. The customer will have the ability to save and/or print the Product Terms, or access them

again at any time in the future.

Customers generally will receive a same day application decision.

18

Once the customer is

approved for the Product and accepts the Product Terms, the amount borrowed will be deposited to the

Bank of America deposit account selected by the customer in the application flow.

Credit Reporting

Customers who obtain the Product will have account status, payment, and non-payment history

reported to credit reporting agencies, which will provide customers with the opportunity to build their

credit scores through on-time repayment.

Other Features and/or Practices

To help customers avoid becoming over-extended and reduce default risk, the customer’s

overdraft setting on the Receiving Account will be set to “Decline All” as a condition to obtaining the

Product. With this overdraft setting, if the customer’s Receiving Account lacks sufficient available funds

in their account (or in any applicable Overdraft Protection plan) to cover a transaction, the transaction will

be returned unpaid and an NSF: Returned Item Fee may be charged.

19

Once the Product is paid in full,

the customer can request to have the overdraft setting on the Receiving Account changed to the

“Standard Setting” to allow for overdrafts at the Bank’s discretion; this change will not occur

automatically. These conditions will be communicated to and accepted by the customer in the Product

application flow and the Product Terms. A reminder will also be provided to the customer as part of an

email communication after the Product is paid in full.

3. An explanation of the potential consumer benefits associated with the product or service.

Bank of America notes that the explanation of the potential consumer benefits of the Product

for purposes of this Application is substantially identical to the explanation provided on this issue in the

BPI Application. Bank of America hereby incorporates that explanation by reference.

As noted in this Application, the Product was designed consistent with the guardrails set forth in

the BPI Application, and includes the additional specific features set forth above. Taken together, the

guardrail features and additional features of the Product are intended to provide the customer benefits

detailed in the BPI Application.

17

Loan funds must be deposited into a Bank of America account owned by the customer. Accounts eligible as “Receiving

Accounts” will be presented to the customer in the application flow for customer se lection. Bank of America Advantage

SafeBalance accounts will not be eligible as Receiving Accounts.

18

Exceptions may apply, such as customers who have placed a “freeze” on their credit file.

19

As described above, an Overdraft Item Fee or NSF: Returned Item Fee incurred specifically for the payment or attempted

payment of the Product will be waived or refunded.

Bank of America has a clear objective to make the financial lives of the customers we serve

better. We are committed to ensuring our policies, practices, programs, and products, including Balance

Assist, align with this purpose. When individuals feel financially secure and are able to achieve their

financial goals, communities are made stronger and we all benefit.

4. An explanation of the potential consumer risks associated with the product or service, and

how the applicant intends to mitigate such risks.

Bank of America notes that the explanation of the potential consumer risks posed by the

Product for purposes of this Application, and how those risks are managed and minimized, is

substantially identical to the explanation provided on this issue in the BPI Application. Bank of America

hereby incorporates that explanation by reference.

Furthermore, Bank of America notes that as set forth in the Product description herein the

Product design seeks to limit the three potential risks (Cycle of Debt, High Cost, and Risk of Default)

identified in the BPI Application in a number of specific ways as detailed in the Repayment and Payment

Structure; Re-borrowing Risk Mitigation; Eligibility and Underwriting; and Other Features and/or

Practices sections of this Application.

5. An identification of the statutory and/or regulatory provisions as to which the applicant

seeks a No-Action Letter and an explanation of why a No-Action Letter is needed, such as

uncertainty or ambiguity regarding the application of the identified statutory and/or

regulatory provisions to the product or service in question.

Bank of America notes that an identification of the statutory and/or regulatory provisions under

which Bank of America submits this Application and an explanation of why a NAL is needed are provided

in the BPI Application. Bank of America hereby incorporates that explanation by reference.

Consistent with the BPI NAL Template, Bank of America is seeking a NAL stating that unless or

until terminated by the Bureau (as described in section C.7 of the Policy), the Bureau will not make

supervisory findings or bring a supervisory or enforcement action against Bank of America under the

Bureau’s authority to prohibit unfair, deceptive, or abusive acts or practices predicated on Bank of

America’s offering or providing the described aspects of the Product set forth in the Application, i.e., the

product features and practices detailed in section II.2 above and section III below; and the information

provided to consumers as set forth in Appendix A and Appendix B.

6. If the applicant wishes to request confidential treatment under the Freedom of

Information Act (FOIA), the Bureau’s rule on Disclosure of Records and Information

(Disclosure Rule), or other applicable law, this request and the basis therefore should be

in a separate letter and submitted with the application. The applicant should specifically

identify the information for which confidential treatment is requested, and may reference

the Bureau’s intentions regarding confidentiality under section G of the Policy.

Confidential treatment has been requested by separate letter.

7. If the applicant wishes the Bureau to coordinate with other regulators, the applicant

should identify those regulators, including but not limited to those the applican t has

contacted about offering or providing the product or service in question

Bank of America wishes the Bureau to coordinate with the Office of the Comptroller of the

Currency.

SECTION III: GUARDRAIL CERTIFICATIONS PURSUANT TO THE BPI NAL TEMPLATE

Bank of America hereby certifies in support of its Application for a NAL that the Balance Assist

Product will meet the guardrail certifications outlined in the BPI NAL Template and set forth below.

1. Status

Bank of America is an insured depository institution with total assets greater than

$10,000,000,000.

2. Eligibility

Bank of America’s Product will be offered and provided only to customers who hold a deposit

account with Bank of America.

3. Product Structure

Bank of America’s Product will be structured as a fixed-term, amortizing small-dollar installment

loan, which the customer will pay back in fixed minimum payment amounts over the term of the loan.

4. Dollar Amount

Bank of America’s Product will not exceed $2,500.

20

5. Repayment Term and Structure

Bank of America’s Product will be structured as an installment loan, with a repayment term that

is more than 45 days and less than one year.

21

The payments will be amortized on a straight-line basis

across more than one payment.

6. No Balloon Payments

None of the required payments

22

under Bank of America’s Product will be more than twice as

large as any other required payment.

20

The Product will be offered in increments of $100 up to $500.

21

The Product repayment term will be 3 months.

22

“Required payments” refers only to payments under the Product’s payment schedule, and not to payments which are past

due. It is possible that a payment which includes past due amounts could be more than twice as large as a required payment,

solely because the customer had not paid the past due amounts according to the payment schedule.

7. Rollovers

Rollovers (i.e., the extension or renewal of a Balance Assist loan on which a scheduled payment

has not been made for an additional fee) will be prohibited. Nor would a borrower be eligible to receive

a new loan to repay an outstanding balance associated with a prior loan. Furthermore, a borrower with

an existing loan is not eligible to receive a new loan until the existing loan is fully repaid.

8. Underwriting

Underwriting for Bank of America’s Product will include the consumer’s transaction activity in

their deposit accounts with Bank of America, also known as “cash flow” underwriting.

9. Collateral

Borrowers will not be required to provide collateral or any other security to take out Bank of

America’s Product.

23

10. Costs and fees

No late payment fees or prepayment penalties will be charged with respect to Bank of America’s

Product.

11. Disbursement

Funds will be disbursed into the borrower’s deposit account with Bank America within three to

five business days after the borrower is approved for the Product.

24

12. Disclosures

Consumer disclosures and marketing materials associated with Bank of America’s Product will

be designed to meet the requirements of all applicable state and federal consumer financial protection

and other laws, and, where appropriate, will be shortened and modified for consumers’ ease of use and

readability for online and mobile channels.

13. Servicing

Bank of America’s Product will be serviced by Bank of America, not a third party servicer.

23

Bank of America will maintain the right to offset funds in the customer’s existing deposit accounts, to the extent authorized

by applicable laws and regulations.

24

Once the customer is approved for the Product and accepts the Product Terms, the amount borrowed will be deposited to

the Bank of America deposit account selected by the customer in the application flow.

Appendix A: Product Terms and Conditions

P

age 1 of 4 © Bank of America, N.A. Member FDIC. All rights reserved

Page |

1

Balance Assist

Loan Agreement

BORROWER:

(Throughout the remainder of this Agreement the borrower

listed above is referred to as "you," or your")

LENDER: Bank of America, N.A.

(Throughout the remainder of this Agreement the lender

listed above is referred to as "we," "us," or "our")

AGREEMENT DATE: 07/16/2020 LAST PAYMENT DUE DATE:

10/16/2020

LOAN NUMBER: 64008017014825

Payment Terms. For value received, you promise to pay to us the principal amount of $300.00, plus an additional finance

charge in the amount of $5.00. You agree to pay according to the payment schedule shown in the TRUTH IN LENDING

DISCLOSURES below. You also agree to the terms and conditions of this Bank of America Balance Assist Loan Agreement

("Agreement") governing your Balance Assist Loan ("Loan").

TRUTH IN LENDING DISCLOSURES

Itemization of the Amount Financed of $300.00

$300.00

Amount credited to your Bank of America account

# 000000000000254650988

$5.00

Finance Charges (fees) included in Total of Payments

$305.00

Total of Payments

Payments. Payments are due on or before the due date. We will apply each payment we receive to the finance charges and

unpaid principal in any order we choose.

ANNUAL PERCENTAGE

RATE

The cost of your credit as a

yearly rate.

9.97%

FINANCE CHARGE

The dollar amount the credit

will cost you.

$5.00

AMOUNT FINANCED

The amount of credit

provided to you or on your

behalf.

$300.00

TOTAL OF PAYMENTS

The amount you will have

paid when you have made

all scheduled payments.

$305.00

Your Payment Schedule will be:

Number of Payments

3

Amount of Payments

$101.68

When Payments Are Due

Monthly beginning

08/16/2020

Prepayment Charge. If you pay off your Loan early, you will not have to pay a penalty; and will not be

entitled to a refund of a part of the finance charge.

Additional Terms. You should refer to the following terms and conditions of this Agreement for information

about nonpayment, default, and our right to accelerate amounts due under this Agreement.

P

age 2 of 4 © Bank of America, N.A. Member FDIC. All rights reserved

Page |

2

If for any reason, one or more payments result in total payments on your Loan exceeding the Total of Payments set forth above

(including both principal amount and finance charges), we reserve the right to reject such payments either in part or in full, and

return the excess funds to you.

Automatic Payment Authorization. You authorize us to make your scheduled payments by automatically withdrawing such

amounts from your designated Bank of America, N.A. checking account # 000000000000254650988 on each payment due

date, or immediately after the scheduled payment due date, if the payment due date is on a Saturday, Sunday or legal holiday.

If you set up automatic payments, each automatic payment will occur on the due date, as long as there are sufficient funds to

cover the payment. If there are not enough funds to cover the payment on the due date, it will be cancelled and you are still

required to make the payment. If you make an additional payment before the scheduled automatic payment date, the automatic

payment will still occur on the due date, unless you cancel it in Online Banking. You agree that we may change or delete a

scheduled payment if the amount you authorized exceeds the amount you owe. To stop an upcoming automatic payment, you

can follow the directions in Online Banking or in our mobile app, or by contacting us at the telephone number listed on the front

of your checking account statement at least three (3) business days prior to the next scheduled payment due date. You

understand and acknowledge that you are not required to authorize automatic payments in order to obtain your Loan from us,

but are voluntarily providing your authorization.

Use of Electronic Records and Signatures. This is intended to be a digital-only Loan, which means all disclosures, documents,

account information or certain other information in connection with this Loan, or that you sign or agree to at our request

("Communications") may be presented, signed, delivered, and maintained in electronic form only. Your consent to our Online

Banking Electronic Communications Disclosure governs your consent to receive these Communications electronically. We

reserve the right, at our discretion, to send you Communications by mail. At the time Communications are presented, please

print or download and save a copy of the Communication to your device. You may, upon request, obtain a paper copy of this

Agreement within twenty-five (25) months of application by contacting the appropriate customer service unit listed on the front of

your checking account statement or visiting the "Contact Us" link on the Bank of America website.

Notices and Other Communications. We may provide Communications to you in English, even though we may have given you

account opening documents and disclosures in a language other than English. If you have questions about any of them or

difficulty reading English, please contact us at the telephone number listed on the front of your checking account statement.

Military Lending Act Disclosure. The following disclosure applies to persons covered by the Military Lending Act - other

governmental programs and laws may also govern or apply to this transaction but are not described in the following disclosure.

The following disclosure is required by the Military Lending Act.

Federal law provides important protections to members of the Armed Forces and their dependents relating to extensions of

consumer credit. In general, the cost of consumer credit to a member of the Armed Forces and his or her dependent may not

exceed an annual percentage rate of 36 percent. This rate must include, as applicable to the credit transaction or account: the

costs associated with credit insurance premiums; fees for ancillary products sold in connection with the credit transaction; any

application fee charged (other than certain application fees for specified credit transactions or accounts); and any participation

fee charged (other than certain participation fees for a credit card account).

Please call our dedicated Military Lending Act toll free number at 833.415.0072 with any questions or concerns (704.264.2615

for international collect calls).

Overdraft Setting, Overdraft Protection Service, and Fees. As a condition of entering into this Agreement, you agree to have

the overdraft setting for the Bank

of America, N.A. checking account you selected to receive the proceeds of this Loan ("your

checking account") set to the

Decline All Overdraft Setting. This setting is defined and described in the Deposit Agreement and

Disclosures governing your

checking account (“Deposit Agreement”). As such, if you do not have sufficient available funds in

your checking account (or any applicable Overdraft Protection plan) to cover a transaction, the transaction will be returned unpaid and

an NSF: Returned Item Fee may be charged. As set forth in the Payment Information section below, exceptions to the NSF:

Returned Item Fee may apply.

If a transfer is made from a linked account as part of an Overdraft Protection plan to cover a transaction, transfer fees may

apply. Overdraft Protection transfers from a line of credit or credit card may be subject to additional fees and accrue interest.

See the Deposit Agreement for related fees and terms.

The Decline All Overdraft Setting will remain in place on your checking account for as long as this Loan remains in effect. Once

the Loan is paid in full, you may contact us - at the telephone number listed on the front of your checking account statement or

by visiting your local financial center - to request a change to the overdraft setting on your checking account to the Standard

Overdraft Setting. Otherwise, your checking account will remain in the Decline All Overdraft Setting.

Additional Terms to Loan Agreement

This document, and any future changes to it, is your contract with us. This Agreement governs your Loan issued by Bank of

America, N.A.

Governing Law. This Agreement is made in North Carolina and we extend credit to you from North Carolina. This Agreement is

governed by the laws of the State of North Carolina (without regard to its conflict of laws principles) and by any applicable

federal laws.

Amendments. We reserve the right to amend this Agreement at any time, by adding, deleting, or changing provisions of this

Agreement. All amendments will comply with the applicable notice requirements of federal and North Carolina law that are in

P

age 3 of 4 © Bank of America, N.A. Member FDIC. All rights reserved

Page |

3

effect at that time.

Anti-Waiver. Our failure or delay in exercising any of our rights under this Agreement does not mean that we are unable to

exercise those rights later.

Loan Purpose. You may use your Loan for personal, family, or household purposes. You may not use your Loan for business or

commercial purposes. You may not use this Loan to make a payment on this or any other credit account with us or our affiliates.

Funds may not be used to purchase, carry or trade securities or repay debt incurred to purchase, carry or trade securities. You

may not use or permit your Loan to be used to make any illegal transaction. You may not use your Loan to conduct transactions

in any country or territory or with any individual or entity that is subject to, or for any purpose that violates, economic sanctions

administered and enforced by the U.S. Department of the Treasury's Office of Foreign Assets Control (OFAC).

Multiple Loans. Only one of these Loans can be outstanding at a time per customer. A 30-day waiting period is required between

each new approved Loan application. We reserve the right to limit the number of Loan applications within a twelve (12) month

period.

Payment Information. For your convenience, payments can be made electronically. We credit payments as of the date received,

if the payment is: (1) paid electronically using the payments and transfers tool online; or (2) paid via automatic payment.

Payments made online or by phone will be credited as of the date of receipt if made by 5 p.m local time. Payments received

after 5 p.m. local time on any day including the payment due date, but that otherwise meet the above requirements, will be

credited as of the next business day. Payments made through any other channel must be paid in U.S. funds.

If, pursuant to your payment instructions, we attempt to initiate a transfer of funds from your Bank of America N.A. checking or

savings account for your payment under this Agreement and such account lacks sufficient available funds (including in any

applicable Overdraft Protection plan) to cover the payment, we will either 1) not charge you an Overdraft Item Fee or NSF: Returned

Item Fee for that transfer or attempted transfer or 2) we will refund the Overdraft Item Fee or NSF: Returned Item Fee charged

for that transfer or attempted transfer. You will, however, remain liable for this payment and any subsequent payments.

Your account history, including monthly payments, can be viewed in Mobile or Online Banking.

Payment Conversions. Payments can be made electronically. Furthermore, we process most payment checks electronically. We

use the information on your check to create an electronic funds transfer. Each time you send a check, you authorize a one-time

electronic funds transfer. You also authorize us to process your check as a check or paper draft, as necessary.

Funds may be withdrawn from your account as soon as the same day we receive your payment. You will not receive your

cancelled check because we are required to destroy it. We will retain an electronic copy.

Attorneys' Fees and Costs. To the extent permitted by applicable law, if we hire an attorney other than our salaried employee to

collect what you owe or realize on any security, you agree to pay our reasonable attorney's fees, including any incurred in

connection with any bankruptcy or appellate proceeding, and any court costs and out of pocket expenses, whether or not the

suit is filed, plus interest on such sums at the highest rate allowed by law.

Default. Except as prohibited by law, you will be in default on this Agreement if any of the following occurs:

A)

You fail to make a payment in full when due.

B)

You fail to perform any obligation that you have undertaken in this Agreement.

C)

You provide us false or misleading information in connection with this Loan.

D)

You die, are declared incompetent, or become insolvent.

E)

You fail to pay or keep any other promise or any other loan or credit agreement you may have with us.

F)

Any creditor of yours attempts to collect any debt you owe through court proceedings, set-off or self-help repossession.

G)

Anything else happens that causes us to believe that we will have difficulty collecting the amount you owe us.

Failure to Pay or Keep Promises as Required. If you do not pay us as agreed or you are otherwise in default, or if an event

occurs which materially impairs your prospects to pay amounts due under this Agreement, we may, at our option, use any one

or more of the following remedies:

A)

Declare the entire unpaid principal amount and finance charges to be immediately due and owning.

B)

Use the right of set-off as explained below.

C)

Use any remedy we have under state or federal law.

Unless otherwise provided by law, by choosing any one or more of these remedies, we do not give up our right to use another

remedy later. By deciding not to use any remedy should you be in default, we do not give up our right to consider the event a

default if it happens again.

Set-off. You agree that, unless prohibited by law, we may set off any amount due and payable under this Agreement against

any right you have to receive money from us without prior notice or demand. "Right to receive money from us" means:

A)

Any deposit account balance you have with us or our affiliates (including, without limitation, joint accounts);

B)

Any money owed to you on an item presented to us or in our possession for collection or exchange; and

P

age 4 of 4 © Bank of America, N.A. Member FDIC. All rights reserved

Page |

4

C)

Any repurchase agreement or other non-deposit obligation.

"Any amount due and payable under this Agreement" means the total amount of which we are entitled to demand payment

under the terms of this Agreement at the time we set off. This total includes any balance the due date for which we properly

accelerate under this Agreement. If your right to receive money from us is also owned by someone who has not agreed to pay

this Agreement, our right of set-off will apply to your interest in the obligation and to any other amounts you could withdraw on

your sole request or endorsement. Our right of set-off does not apply to an account or other obligation where your rights arise

only in a representative capacity. It also does not apply to any Individual Retirement Account or other tax-deferred retirement

account.

We will not be liable for the dishonor of any transaction when the dishonor occurs because we set off this debt against any of

your accounts. You agree to hold us harmless from any such claims arising as a result of our exercise of our right of set-off.

Consent to Share Information. By entering into this Agreement, you authorize us to share information regarding this Loan with

any person named as a joint owner of the checking account used to accept proceeds of your Loan (as set forth in Page 1 of this

Agreement).

Change of address. You must notify us promptly when you change your address. We may also change your address if so

notified by the post office or others.

Credit Reporting. We will report information about your account to credit bureaus, which may provide customers with the

opportunity to build their credit history through on-time repayment. Payments made on time, late payments, missed payments, or

other defaults on your account will be reflected in your credit report.

If you believe we have furnished inaccurate or incomplete information about you or your account to a credit reporting agency,

write to us at: Bank of America, N.A., Credit Reporting Agencies, FL9-600-02-15, P.O. Box 45224, Jacksonville, FL 32232-

9743. Please include your name, address, home phone number, and account number, and explain what you believe is

inaccurate or incomplete.

Communicating with You. To the extent permitted by applicable law, and without limiting any other rights we may have, you

consent to our communicating with you, in connection with this Loan, using any telephone number, including a cellular

telephone number, or email address that you provided in your application, or using any telephone number, including a cellular

telephone number, email address, or other address or number that you provide in the future. You authorize us to communicate

with you using any current or future means of communication, including, but not limited to, automated telephone dialing

equipment, artificial or pre-recorded voice messages, SMS text messages, email directed to you at a mobile telephone service,

or email otherwise directed to you. WE MAY USE SUCH MEANS OF COMMUNICATION EVEN IF YOU WILL INCUR COSTS

TO RECEIVE SUCH COMMUNICATIONS.

Customer Identification Program (CIP). Pursuant to requirements of law, including the USA Patriot Act, Bank of America, N.A. is

obtaining information and will take necessary actions to verify your identity.

Integration and Severability. This document contains the entire Agreement between you and us. If any part of this document is

invalid, all other parts of the document will remain valid.

Appendix B: Digital Marketing and Application

Materials

1

Balance Assist | Customer Experience | Entry Points

Online Banking Online Banking and Mobile

2

Balance Assist | Customer Experience | Entry Points

Visit Open An Account > Advantage Plus/Advantage Relationship Section

3

Balance Assist | Customer Experience | Applying for Balance Assist | Mobile

1. Overview

2. Credit Check

Close

4

Balance Assist | Customer Experience | Applying for Balance Assist | Mobile

3. Approval

4. Confirm and Consent 5. Complete

Loan and Payment Amount are Illustrative

5

Balance Assist | Customer Experience | Digital Payments

Make a Payment Payment Confirmation

Loan and Payment Amount are Illustrative

6

Balance Assist | Customer Experience | Digital Servicing

Account Overview

Account Details

Account Balance, Loan and Payment Amount are Illustrative

In this example, customer had $4.47 in

their account before getting their Balance

Assist loan

This example reflects the third and final

payment that is due

7

Balance Assist | Customer Experience | Alerts | Application Results

Loan and Payment Amount are Illustrative

Account Open Overdraft Setting Changed Declined

in 4566

8

Balance Assist | Customer Experience | Alerts | Payments

Payment Due Soon

Payment Made Payment Past Due Paid in Full

Payment Amount is Illustrative

in 4566