This PDF is a selection from an out-of-print volume from the National

Bureau of Economic Research

Volume Title: Tax Policy and the Economy, Volume 14

Volume Author/Editor: James M. Poterba, editor

Volume Publisher: MIT Press

Volume ISBN: 0-262-66164-0

Volume URL: http://www.nber.org/books/pote00-2

Publication Date: January 2000

Chapter Title: Stock Market Reaction to Capital Gains Tax Changes:

Empirical Evidence from the 1997 and 1998 Tax Acts

Chapter Author: Douglas A. Shackelford

Chapter URL: http://www.nber.org/chapters/c10847

Chapter pages in book: (p. 67 - 92)

Stock Market Reaction to

Capital Gains Tax Changes:

Empirical Evidence from the

1997 and 1998 Tax Acts

Douglas A. Shackelford

University of North Carolina and NBER

EXECUTIVE SUMMARY

This paper analyzes the impact of changes in capital gains taxes on

equity values. Seven necessary conditions are outlined for stock prices to

be affected by a change in the taxation of long-term capital gains. Specifi-

cally, the marginal investor must be an individual, investing for the

requisite holding period, selling in a taxable disposition, and compliant.

His short-term capital gains from all investments equal or exceed short-

term capital losses, and his long-term capital gains from all investments

equal or exceed long-term capital losses. In addition, the capital gains tax

change must alter the investor's expectation of the taxes that wifi be

generated when he sells in the future, and inelasticities in the supply of

capital must prevent immediate economic readjustment.

The paper then reviews four studies that estimate the stock market

reaction to capital gains tax changes in the Taxpayer Relief Act of 1997

and the Internal Revenue Service Restructuring and Reform Act of 1998.

The recency of these legislative changes and the conditions under which

they were enacted provide useful settings for recalibrating the relation

between stock prices and capital gains taxation.

This paper has benefited from comments by Jennifer Blouin, Jim Poterba, and Jana Raedy.

68

Shackelford

Although evaluating different firms and event periods, the studies

generally find:

Stock prices react to changes in the capital gains tax policy.

Stock prices react quickly to information about tax legislation.

The stock price reaction is largely complete by public announcement

of the change.

The magnitude of the stock price reaction is material.

These findings join a growing literature documenting that capital gains

tax policy plays a role in establishing equity values.

1. INTRODUCTION

Capital gains tax policy has entered a new phase of legislative uncer-

tainty. From 1987 to 1997, individuals faced a maximum U.S. statutory

capital gains tax rate of 28 percent on investments held for more than

one year. Since then, Congress has reduced the long-term capital gains

tax rate and adjusted the holding period twice.

The Taxpayer Relief Act of 1997 (TRA 97), which became law on August

5, 1997, lowered the maximum statutory long-term capital gains tax rate

for individuals from 28 to 20 percent, effective May 7, 1997. After July 28,

1997, the lower rate was restricted to property held for more than 18

months. Investments held for more than 12 months, but not more than

18 months, faced the 28 percent tax rate. TRA 97 did not change the rate

applied to investments held for one year or less. They continued to be

taxed at the ordinary income tax rate, which caps at 39.6 percent.

The 18-month holding period was short-lived. On July 22, 1998, the

Internal Revenue Service Restructuring and Reform Act of 1998 (IRSREA

98) repealed the 18-month holding period, effective January 1, 1998.

Thus, investors currently enjoy a maximum 20 percent long-term capital

gains tax rate on all purchases held for more than a year.

This summer Congress attempted to reduce the long-term rate fur-

ther. On August 5, 1999, Congress passed the Taxpayer Reform and

Relief Act of 1999, which would have reduced the maximum individual

capital gains tax rate to 18 percent, effective January 1, 1999. Although

President Clinton vetoed the bifi on September 23, 1999, speculation

remains that a compromise bifi may materialize.

With each of these legislative initiatives, there has been no consensus

about the impact of the capital gains tax legislation on stock prices. For

example, in 1997, many predicted the reduction of the capital gains tax

rate would spur savings and investment, ultimately increasing stock val-

Reaction to Capital Gains Tax Changes

69

ues, though perhaps preceded by an initial sell-off. Some doubted the cut

could spur an already record-level stock market. Others foresaw disaster.

For example, columnist John Rothchild (Fortune, April 28, 1997,

p. 409)

called the rate reduction, "the worst thing to happen to the stock market

since Saddam Hussein invaded Kuwait." David Jones, analyst at Aubrey

G. Lanston, summarized the confusion: "There's a huge amount of uncer-

tainty about thishow much selling there wifi be, how much revenue

generated, what the effect wifi be on stocks" (Boston Globe, June 22, 1997,

p. E7). The same article quotes Brookings economist William C. Gale

stating, "I can't venture a guess" about whether the cut wifi increase or

decrease stock prices. A purpose of this paper is to sharpen forecasts of

the stock price effects of future capital gains tax changes on stock prices by

analyzing the conditions required for such changes to affect stock prices

and reviewing initial research evaluating the 1997 and 1998 Acts.

Before this recent flurry of legislative action, the previous two

changes in capital gains tax rates occurred in the Tax Reform Act of 1986

and the Economic Recovery Tax Act of 1981. Neither act provides a

powerful setting for evaluating the stock market reaction to capital gains

tax changes. Their development and complexity impede attempts to

isolate those responses. Both involved months of debate and substantial

restructuring of the tax system.

In contrast, the 1997 and 1998 changes to capital gains taxation poten-

tially provide unusually powerful settings to isolate price effects. Nei-

ther bifi was as comprehensive, as complex, or as controversial as the

1981 and 1986 Acts. With both bills, information about the capital gains

tax changes appear to have been conveyed to the equity markets during

a brief period, causing the stock market to adjust quickly its expectations

about the probability of a change. If so, this facilitates isolation of the

stock market reaction to capital gains tax changes, because prices should

have impounded the changes during a narrow window.

An additional advantage of examining the recent Acts is that economic

and technological changes (e.g., reduced brokerage fees and expanded

use of stock options) since the 1980s have potentially altered the benefits

of favorable long-term capital gains treatment for the stock markets. In

particular, more individuals (the sole group benefiting from favorable

long-term capital gains tax rates) now invest in equity, and their hold-

ings are greater. As a result of the bull market, many shares are highly

appreciated, subject to substantial capital gains taxes. Consequently,

personal capital gains taxation may be more important in equity price

formation now than in the past.

Recognizing the opportunity to recalibrate the relation between share

prices and capital gains tax changes, four studies have assessed the stock

70

Shackelford

market reaction to the 1997 and 1998 Acts. Each analysis

employs event

study methodology. Firm-level price reactions are examined using

research

designs that assess differences in share price responses across

firms. The

tests control for indirect macroeconomic factors that

affect all sectors.

Three studies evaluate share price responses during the development

of TRA 97 and following its enactment. Lang and Shackelford

(2000) find

that when Congress and the White House agreed to cut the

capital gains

tax rate in May 1997 (three months before the

bill's passage), returns on

high-dividend-yield stocks were lower than those on stocks with lower

dividend yields. They interpret these findings as evidence that investors

discriminated among companies based on the probability that share-

holder returns would be affected by the new capital gains tax rates.

Sinai and Gyourko (1999) test whether investors discriminated between

real estate investment trusts (REITs) organizational forms based on the

potential tax savings to individuals selling real estate. Consistent

with the

capital gains rate reduction lowering the cost of purchasing real estate,

they find that in 1997 traditional REITs outperformed acquisitive

UPREITs

(an organizational form that benefited less from the rate reduction).

Guenther (1999) also investigates TRA 97. He seeks to determine

whether individual shareholders deferred selling appreciated stock until

the effective date for the lower rate was finalized. Consistent

with a

sellers' strike, Guenther finds lower ex-dividend day returns

immedi-

ately preceding the effective date.

Blouin, Raedy, and Shackelford (1999b) evaluate the stock price effects

of the IRSRRA 98 reduction in the long-term capital gains holding pe-

riod. They find that appreciated firms whose initial public shareholders

met the 12-month holding period, but not the

18-month period, un-

derperformed during the conference committee's deliberations that first

proposed repeal of the 18-month period. They conclude that shortening

the holding period triggered a sell-off that depressed share prices.

Overall, the evidence in these studies is consistent with the personal

taxation of capital gains affecting individual firms' prices.

The results

imply that stock prices respond to capital gains tax changes as

though

equity values capitalized anticipated capital gains taxes. In

addition, the

response is large, quick, and often complete

by public announcement of

the change.

The next section reviews the taxation of capital gains and losses.

Section

3 outlines seven necessary conditions for capital gains taxes to

affect stock

prices. Section 4 models the stock-price effect of a change in

the capital

gains tax rate. Section 5 presents results from the three studies

of TRA 97.

Section 6 discusses results from the study of the IRSRRA 98.

Section 7

draws four inferences from the studies. Closing remarks follow.

Reaction to Capital Gains Tax Changes

71

2. INDIVIDUAL TAXATION OF CAPITAL GAINS

AND LOSSES

Individual investors are taxed differently on the sale of capital assets,

depending on the length of time that they hold the property. Gains and

losses from sales of property held longer than the specified holding

period are long-term. All other realizations are short-term. Table 1 shows

that over the last forty years, the holding period required for long-term

classification has ranged from 6 to 18 months. In all years, except 1998-

1990 (when no differential existed), long-term capital gains have been

tax-favored compared with short-term capital gains. From 1970 through

1986, short-term capital losses were tax-favored compared with the long-

term capital losses because investors could deduct only half of their long-

term capital losses.

Computation of the taxable income arising from capital transactions

involves two separate nettingsshort-term capital gains netted against

short-term capital losses, and long-term capital gains netted against

long-term capital losses. If short-term capital gains exceed short-term

capital losses and long-term capital gains exceed long-term capital

losses, no further computations are required. The applicable tax rate for

short-term capital gains applies to the net short-term capital gains (i.e.,

short-term capital gains less short-term capital losses), and the applica-

ble tax rate for long-term capital gains applies to the net long-term capital

gains (i.e., long-term capital gains less long-term capital losses).

Table 1, colunm (1), shows the change in marginal tax rates when

a

stock shifts from short-term to long-term, assuming the nettings yield

both net short-term capital gains and net long-term capital gains. For

example, under current law, if a one-dollar gain (loss) is recognized

on

property held one year or less, taxes increase (decrease) by 39.6 cents. If a

one-dollar gain (loss) is recognized on property held more than

one year,

taxes increase (decrease) by 20 cents. Thus, when the stock shifts from

short-term to long-term, the marginal tax rate applied to a realization

changes by 19.6 percentage points [bottom row of Table 1, column (1)1.1

Likewise, if the two nettings yield both net short-term capital losses and

net long-term capital losses, the applicable deduction rate for short-term

capital losses applies to the net short-term capital losses, and the applica-

ble deduction rate for long-term capital losses applies to the net long-term

The gain or loss from the potential realization is assumed not to alter the overall gain or

loss position. If the investment being evaluated would create sufficient gain or loss to alter

the overall position, the marginal tax rate calculation becomes endogenous to the decision,

and the analysis is beyond the scope of this paper.

TABLE 1

Change in Marginal Tax Rate for an Individual Investor in Highest Statutory Tax Rate when Stock Qualifies

for Long-Term Treatment

(1)

Statutory

(2)

(3)

(B)

Change in

marginal tax

rate when

stock goes

tax rate: Statutory

Effective

(A)

long-term:

(C)

Holding

short-term

tax rate:

tax rate: If LTGLTL

If LTGLTL

For all other

period

gain (STG)

long-term

long-term

and STGSTL:

and STGSTLO')

combinations of

Date of sale

(mo)

or loss (STL)

gain (LTG)

loss (LTL)(a)

(1) - (2)

(1) - (3)

LTG, LTL, STG, STL

1961-1963

6

91

45.5 91

45.5

0

0

1964

6

77

38.5

77

38.5

0

0

1965-1967

6

70

35

70

35

0

0

1968-1969

6

77

38.5

77

38.5

0

0

1970

6

71.75

35.875

35.875

35.875

35.875

0

1971-1976

6

70

35

35

35

35

0

1977

9

70

35

35

35

35

0

1/1/7'S-10/31/78

12

70

35

35

35

35

0

11/1/28-12/31/81

12

70

28

35

42

35

0

1/1/82-12/23/84

12

50

20

25

30

25

0

The effective rate for long-term losses is the statutory rate in all

years except 1970-1986, when only half of net long-term capital losses could be deducted. Thus, in

those years, the effective rate is half of the statutory rate.

The maximum annual capital-loss deduction for individuals is $2000 in 1977, $1000

in earlier years, and $3000 in later years. Additional capital losses are carried

forward indefinitely. Thus, if total capital losses less total capital gains exceed the annual limit

the marginal rate is reduced depending on the carryforward utilization

period, and altered depending on the applicable rate in the year of utilization.

The holding period shifted from 12 to 6 months, effective for assets purchased after June 22, 1984. Thus,

the holding period for property sold during this time period

varied depending on the acquisition date.

The holding period shifted from 6 to 12 months, effective for assets purchased after December 31, 1987.

Thus, the holding period for property sold during this time

period varied depending on the acquisition date.

The long-term tax rate on property held more than 12 months, but less than 18 months,

was 28 percent.

12/24/84-6/22/85

6 or 12(c)

50

20

25

30

25

0

6/23/85-12/31/86

6

50

20

25

30

25

0

1987

6

38.5

28

38.5

10.5

0

0

6 or 12'

28

28

28

0

0

0

1/2/-12/31/

12

28

28

28

0

0

0

1991-1992

12

31

28

31

3

0

0

1/1/93-5/6/W 12

39.6

28

39.6

11.6

0

0

5/7/W-7/28/97

12

39.6

20

39.6

19.6

0

0

7//W-i2/31/97

18

39.6

20(e)

39.6

19.6

0

0

1998-present

12

39.6

20

39.6

19.6

0

0

74

Shackelford

capital losses. Table 1, colunm (2), shows the change in

marginal tax rates

when a stock shifts from short-term to long-term,

assuming the nettings

yield both net short-term capital losses and net long-term

capital losses.

Because short-term and long-term losses provide

the same deduction

under current law, the marginal tax rate change is zero

when a stock

passes from short-term to long-term

[bottom row of Table 1, column (2)1.

Note that the marginal tax rate change is zero regardless

of whether the

specific stock being evaluated has appreciated or

depreciated.

If one netting yields net capital gains and the other netting

yields net

capital losses, a single income or deduction amount is

computed from the

difference in the two initial nettings. For example, assume

long-term

capital gains are 9, long-term capital losses are 4, short-term

capital losses

are 3, and short-term capital gains are

2. The initial nettings wifi yield net

long-term capital gains of 5(9-4) and net short-term

capital losses of 1 (3-

2). A final netting produces a single net long-term

capital gain of 4 (5-1).

Here, the only gain or loss included in the

individual's taxable income is

the net long-term capital gain of 4, which is taxed at

the long-term capital

gains tax rate.

If this additional netting is required, then taxes are

unaffected by

whether a gain is long-term or short-term or whether a loss is

long-term

or short-term. To illustrate, suppose

the individual in the preceding

example delays the sale of an appreciated property until it

qualifies for a

long-term gain. The long-term capital gains increase to

10, and the short-

term capital gains fall to 1. Net long-term

capital gains are now 6 (10-4),

and net short-term capital losses are now 2 (3-1). The

final single net

long-term capital gains is unchanged at 4 (6-2).

Likewise, if the individ-

ual accelerates a sale, increasing the short-term gain

and decreasing the

long-term gain, then the total taxes are unaffected.

Shifting losses be-

tween long-term and short-term status also

does not affect the individ-

ual's tax liability.

To restate using current rates, assume (1) short-term

capital losses ex-

ceed short-term capital gains, (2) long-term capital gains

exceed long-term

capital losses, and (3) total (short- plus long-term)

capital gains exceed

total capital losses. Under these facts, an additional

dollar of long-term

capital gains increases taxes by 20 cents, because net

long-term capital

gains have risen by 1 dollar. However, an

additional dollar of short-term

capital gains also increases taxes by 20 cents. The short-term

gain reduces

the amount by which the short-term losses exceed

the short-term gains.

Since short-term losses (net of short-term gains)

offset long-term gains,

the effect of an additional dollar of short-term

capital gain is to increase net

long-term capital gains by 1 dollar and taxes by 20 cents.

Reaction to Capital Gains Tax Changes

75

Similarly, an additional dollar of long-term capital losses reduces taxes

by 20 cents, because long-term capital gains, net of long-term capital

losses, have fallen by 1 dollar. An additional dollar of short-term capital

loss also decreases taxes by 20 cents. The short-term loss increases the

amount by which the short-term losses exceed the short-term gains by 1

dollar. Since short-term losses (net of short-term gains) offset long-term

gains, the effect of an additional dollar of short-term capital gain is to

decrease net long-term capital gains by 1 dollar and reduce taxes by 20

cents.

To summarize, the marginal tax rate associated with the sale of a stock

must be evaluated with a portfolio perspective where all other gains and

losses are considered. Under current law, if the investor's portfolio of

gains and losses creates either net long-term capital losses

or net short-

term capital losses, then the marginal tax rate for a particular stock does

not change when the stock passes the one-year holding period. The prefer-

ential long-term capital gains tax rate only affects individuals whose total

long-term capital gains equal or exceed long-term capital losses and

whose total short-term capital gains equal or exceed short-term capital

losses [Table 1, colunm (1)1. These conditions hold regardless of whether

the stock being evaluated has appreciated or depreciated. The only

excep-

tion to this rule, which footnote 1 assumes is not applicable, occurs if the

gain or loss from the stock being evaluated alters the overall portfolio gain

or loss position. In this case, the marginal tax rate becomes endogenous to

the decision to sell. Such analysis is beyond the scope of this

paper.

The netting provisions introduce a timing dimension to the investor

trading decision. Generally, investors maximize returns by realizing tax-

favored long-term capital gains and deductible capital losses in different

years (Constantinides,

1984).

Separation prevents the loss of tax-favored

treatment through the netting of long-term capital gains against capital

losses. Consistent with separation, Dhaliwhal and Trezevant

(1993) find

that January returns are greater for appreciated (depreciated) stock after

a year with a bull (bear) market. Their results are consistent with inves-

tors selling appreciated (depreciated) stock during the final days of De-

cember of bull (bear) market years, segregating long-term gains and

deductible losses between years.

Finally, the total deduction for capital losses, both long-term and

short-term, is currently limited to

$3000 annually for individuals. The

limit was $2000 in 1977

and $1000 in earlier years. Excess capital losses

are carried forward indefinitely, retaining their long-term and short-

term status. Thus, the marginal tax rate for a carried-forward deduction

is reduced for the time value of money.

76

Shackelford

3. NECESSARY CONDITIONS FOR CAPITAL

GAINS

TAXES TO AFFECT STOCK PRICES

At least seven conditions must hold for stock prices to be

affected by a

change in the long-term capital gains tax rate. These

factors are equally

applicable to a change in the holding period.

3.1 Condition 1: Individual as Marginal Investor

The marginal shareholder must be an individual or a

flow-through entity

(e.g., mutual fund, partnership, S corporation, limited

liability corpora-

tion) that passes capital gains to individual tax returns.

Other investors,

such as corporations, qualified plans (e.g., pensions), tax-exempt

organi-

zations, and foreign investors, face the same tax rate

regardless of the

duration the property is held. If the marginal shareholder

is not an

individual in a tax bracket where long-term capital gains are taxed

favor-

ably, changes in the capital gains tax rates should not

affect prices.

Extant studies (e.g., Mifier and Scholes, 1982) present

evidence consis-

tent with the marginal investor not being a

taxable individual investor.

3.2 Condition 2: Net Portfolio Gain Position

The long-term capital gains tax rate must apply to the

marginal investor's

realization after applying the netting provisions discussed

above. For

example, in Table 1, column (A), when the investor's portfolio

of short-

term capital gains exceeds or equals short-term

capital losses and long-

term capital gains exceed or equal long-term

capital losses, the long-term

capital gains tax rate applies to a realization. More generally,

long-term

capital gains must exceed long-term capital losses and the excess

of short-

term capital losses over short-term capital gains,

if any. Otherwise, the

investor's marginal tax rate is unaffected by a change in the

long-term

capital gains tax rate.

An effect of the netting provisions is to relax the link between

capital

gains tax changes and the pricing of specific stocks.

Instead of the appli-

cable tax rate being determined by the stock's price and the

investor's tax

basis, it depends on the investor's portfolio of gains and losses

through-

out the year. Moreover, determination of the

portfolio position is made

annually, so the applicable tax rate is uncertain before year-end.

3.3 Condition 3: Holding Period

The marginal investor must be willing to invest for the requisite

holding

period. The advantage of long-term capital gains treatment must

domi-

nate nontax incentives to sell earlier, e.g.,

portfolio rebalancing. Al-

Reaction to Capital Gains Tax Changes 77

though many shares are held for long periods, day traders and other

individuals with short investment horizons may find the inducement of

a lower tax rate insufficient to defer their sales.

To illustrate the coordination of taxes and market risk, let P(1 - T) + BT

equal the after-tax proceeds, where P is the sales price, B is the tax basis,

and T is the long-term capital gains tax rate. A change in the long-term

capital gains tax rate (LIT) leaves the after-tax proceeds unchanged if the

price falls by LIr (P - B)/(1 - T - LiT). For example, the benefit of IRA

97's 8-percentage-point decline in the long-term capital gains would

have been fully offset by a price decline equal to 10 percent of the share's

appreciation, i.e., P - B (see footnote 4 in Guenther, 1999, for a similar

analysis).

3.4 Condition 4: Taxable Disposition

The marginal investor must intend to dispose of the stock in a taxable

transactionspecifically, secondary market trades, share repurchases,

or corporate liquidation (Lang and Shackelford, 2000). Any other invest-

ment strategy (e.g., buy-and-hold or nontaxable disposition) renders

capital gains taxes irrelevant. Although each trading day provides ample

evidence that some individuals sell securities, many stocks likely are

intended to be held until death, avoiding all income taxation on their

appreciation. Some shares are intended to remain in family hands across

generations through inter vivos gifts. Others are intended to be contrib-

uted to charities, avoiding all taxation on appreciation. Still others are

intended to be exchanged for acquirer's stock in a tax-free reorganiza-

tion. To the extent investors anticipate never selling their property in a

taxable disposition, the influence of changes in the long-term capital

gains tax rate on prices is diminished.

A nontaxable disposition method discussed at length in theoretical

finance and public economics is the use of intricate deferral strategies

(e.g., equity swaps) that enable investors to diversify without triggering

a capital gain (see, e.g., Constantinides, 1983, 1984; Stiglitz, 1983;

Scholes and Wolfson, 1992; Shackelford, 2000). Whether perfect substi-

tutability among financial assets precludes the possibility of taxes affect-

ing equity prices is an empirical question (see Poterba's 1987a analysis).

However, anecdotes in the business press (e.g., Estee Lauder's well-

publicized shorting-against-the-box) suggest that some investors at least

partially avoid capital gains taxes.

3.5 Condition 5: Compliance

The marginal investors must pay the capital gains tax generated at real-

ization. Noncompliance with the capital gains tax law would weaken

78

Shackelford

equity reactions to capital gains tax changes. Landsman, Shackelford,

and Yetman (1999) identify three reasons that capital gains noncom-

pliance may flourish. First, the transactions creating capital gains are

usually large, increasing the returns to evasion. Second, capital gains

transactions are irregular and infrequent, making it difficult for the tax-

ing authorities to establish baselines cross-temporally or across taxpay-

ers. Third, tax bases are not tracked by third-party reports, and unless

brokers are employed, no third-party reports are required to track sales

proceeds.

Unfortunately, too little is known about capital gains tax compliance

rates to assess their effect on the relation between capital gains taxes and

equity. The nearly sole source of information, Internal Revenue Service

estimates from the nine Taxpayer Compliance Measurement Program

(TCMP) surveys from 1965 to 1988, indicates that the percentage of

actual capital gains that appear on tax returns ranges from 61 percent in

1976 to 93 percent in 1988.2 This compares with 99-percent compliance

for wages and 98-percent compliance for interest in the 1988 TCMP

survey. Examining data from six TCMP surveys, Poterba

(198Th) adds

that capital gains tax compliance is decreasing in marginal tax rates.

3.6 Condition 6: Alteration of Expectations

The change in capital gains tax policy must alter the marginal investor's

expectations about the capital gains tax rate that wifi apply when the

stock is sold. Investors likely perceive that the life of any change in

capital gains tax policy is short. The taxation of capital gains and losses

has been controversial for decades, and policymakers continually ad-

vance proposals for change, including elimination. Unless selling is an-

ticipated in the immediate future, an investor likely relies little on a

change in current capital gains tax rates to forecast the relevant rate at

disposition. Thus, the impact of a change in capital gains taxes is dimin-

ishing in the individual's investment horizon.

3.7 Condition 7: Inelastic Supply

Inelasticities in the supply of capital must prevent immediate readjust-

ment throughout the economy following a change in the long-term capital

gains tax rate. For example, suppose reductions in long-term capital gains

tax rates attract individual investors. The surge of individuals wifi apply

upward price pressure and decrease equity returns to nonindividual in-

vestors. Lacking transaction costs, nonindividual investors would inune-

2

In his review of 1979 tax returns, Thompson (1987) notes that the capital gains tax

compliance rate for stocks is higher than for business property and personal residences.

diately shift from equities to investments less favorably taxed from

an

individual's perspective. The downward price pressure from nonindi-

viduals leaving the market could offset the upward price pressure from

individuals entering the market, leaving stock prices unaffected.

3.8 Summary

To summarize, all seven of the above conditions must hold for a change

in the long-term capital gains tax rate to affect prices. If any condition

does not hold, a firm's stock price will be unaffected by a change in

capital gains-tax policy, except through indirect macroeconomic shifts.

No direct link between the change and the firm's price wifi

occur. It

seems reasonable that for at least some companies, all seven conditions

wifi not hold. Thus, for at least those companies, a change in the capital

gains tax rate wifi not affect equity prices.

4. MODEL

Lang and Shackelford (2000) assume the seven conditions hold and

model the share-price effects of a change in the long-term capital gains

tax rate. Their model, reproduced below, provides a useful benchmark

for predicting the stock-price reaction to a change in the long-term rate.

They assume that the present value of a firm's future free cash flows (F

per period) and the present value of its shareholder distributions

(D1

is

the initial distribution) can be equated with a distribution growth rate

y.

F

D1(1

+

y)

n=1 (1

+

r)

n=1

(1

+

The share price at time t (Pr) equals the expected dividends at t

+

1,

after shareholder dividend taxes (T"), plus the anticipated sales price at

t

+

1 (P1), less shareholder capital gains taxes (T') on the change in

price, discounted at r:

P

=

E

+ D1

(1 - T1)

- (P+1 -

1+r

If T

=

TC and i-

T'1 for all t, current prices

P0

can be expressed as

Po

D1(1T')

Reaction to Capital Gains Tax Changes

79

r [Tc

+ (D1/F)

(1 - Tc)]

(1)

80

Shackelford

al)0

FD1

=PO

a1C (F_Di)Tc+Dl

The derivative implies that if a firm retains part of its internally gener-

ated cash flow, then a decrease in the capital gains tax rate increases its

stock prices and the rise in stock price increases with the cash retained.

To gauge the economic magnitude of the 1997 capital gains tax cut,

assume a firm is generating $25 of F, is paying $5

of D1, and has a 10-

percent discount rate. Evaluated at the maximum statutory tax rates

before the reduction, an unanticipated capital gains tax rate cut from 28

percent to 20 percent increases share prices by approximately 15 percent.

If the firm's dividend yield is one percentage point greater (less), then

prices rise by about 12 (20) percent, a 3- (5-)percentage point change in

returns. These estimates likely provide an upper bound for actual

stock

price reactions, because they assume all investors are affected by the rate

change, the rate change is fully unanticipated and immediately enacted,

dividend policies are immutable, and future distributions and taxes are

certain.

Klein (1999) shows that this model depends critically on the assump-

tion of no unrealized gains at the beginning of the investment period. If

investors have unrealized gains, a reduction in the capital gains tax rate

could actually reduce stock prices. This counterintuitive result occurs

because sellers now demand less compensation from buyers to trade.

Thus, the directional prediction associated with a change in the capital

gains tax rate depends on whether the stock's appreciation has occurred

in the past or is anticipated in the future.

Even if all seven conditions are met and the model correctly depicts

the effects of capital gains taxes on share prices, it remains an empirical

issue whether the price pressure applied by the capital gains tax policy

changes is sufficient to move stock prices. To make that assessment, four

empirical studies have recently analyzed TRA 97 and IRSRRA 98. Each

attempts to determine whether stock price movements around the

legis-

lative changes are consistent with capital gains taxes affecting equity

values. The next two sections provide a summary of each study's motiva-

tion, design, and findings.

5. TAXPAYER RELIEF ACT OF 1997

5.1 Summary of Lang and Shackelford (2000) (LS)

This study analyzes stock price reactions to the 1997 announcement that

capital gains tax rates would be reduced. Tax legislative information

(4)

Reaction to Capital Gains Tax Changes

81

usually leaks to the market over a long period as legislation slowly works

through Congress. With TRA 97, investors may have changed their

expectations about a capital gains tax rate change in a more compressed

period. On April 30, 1997, after months of uncertainty about capital

gains tax legislation, the Congressional Budget Office released an

un-

scheduled, favorable revenue estimate. The next morning, May 1, 1997,

the Wall Street Journal and the New York Times reported that the CBO

release had enabled negotiators to finalize the budget, including a capital

gains tax reduction.

The following day, May 2, 1997, the Clinton administration and

con-

gressional leaders announced general agreement on the fiscal 1998 bud-

get. Included in the accord was a commitment to an unspecified reduction

in the maximum statutory long-term capital gains tax rate for individuals,

which was eventually codified in TRA 97. The business press immediately

speculated that the capital gains tax reduction would shuffle individual

shareholdings and depress the market. For example, the Wall Street Jour-

nal (May 5, 1997) quoted an unnamed market strategist as predicting the

capital gains tax cut "would attract investor attention even more toward

stocks with a high probability of capital appreciation and away from divi-

dends" (p. C12). However, they warned that ".

.

.

, a

burst of selling may

hit the markets, strategists say. That could be the reaction, at least temp

o-

rarily, as investors with big long-term profits rush to lock in their gains"

(p. Cl).

If the CBO release and the subsequent accord substantially changed

the probability that capital gains tax rates would be cut, then the market

response to the capital gains tax rate reduction should have been concen-

trated over a few days. LS hypothesize that stock returns during that

week were negatively correlated with dividend yields because the

prom-

ise of a lower capital gains tax rate was less relevant for firms paying

(large) dividends.3 Applying a market-model approach, they investigate

the stock-price reaction of dividend-paying and non-dividend-paying

stocks during the budget-accord week. The analysis is conducted

on the

2,000 largest U.S. corporations as reported by Datastream for the 129

weeks from January 1995 through the event week (239,296 observa-

LS note the similarity the spirit of their analysis and a Wall Street Journal (April 25, 1997)

report that Brian Wesbury, chief economist at the Chicago bond firm of Griffin, Kubik,

Stephens & Thompson, characterized the Nasdaq Composite as an indicator of the

mar-

ket's expectations of the future capital gains tax rate, "a little cap-gains futures contract."

Wesbury related movements in the Nasdaq since November 1996 to changes in the proba-

bility of a capital gains tax rate reduction. The IJJIA was termed less sensitive to capital

gains tax changes because its stocks "throw off a relatively heavy share of their profits in

dividends."

82 Shackelford

tions). Of the 1,975 sample firms with complete data, 1,247 (63 percent)

pay dividends.

LS find that the mean return during the accord week was 6.1 percent

for dividend-paying stocks and 12.9 percent for the non-dividend-

paying firms. Regression analysis is undertaken to control

for possible

nontax differences in return, such as risk. The regression summary

statistics in Table 2, panel A confirm that non-dividend-paying compa-

nies outperformed dividend-paying companies during the event

week.

The regression coefficient on the variable of interest is 4.3,

indicating

that, after controlling for risk, the returns of non-dividend-paying

stocks exceeded the returns of other firms by 4.3 percentage points, on

average.

Table 2, panel B shows results for a similar regression that substitutes

TABLE 2

Regression Coefficient Estimates

(t Statistics)

Panel A

Regression equation(t'):

returns1 =

dividend + /2 week + /33 dividend X week +

/3 S&P5OO + e

/33 = 4.3

statistic = 14.5

Sample: 2,000 largest U.S. corporations as reported by Datastream for which

complete data are available

Number of firms

1975

Number of observations

239,296

Panel B

Regression equation(b):

returns =

dividendyield + /2 weeks + /33 dividendyield X week +

f34

S&P5OO1 + e

/33 = 0.29

f-statistic = 5.1

Sample: Dividend-paying stocks from the 2,000 largest U.S. corporations as re-

ported by Datastream for which complete data are available

Number of firms

1247

Number of observations

157,055

Adapted from Lang and Shackelford (2000, Tables 2, 3). Dependent variable: weekly return.

returns = firm i's weekly return for the 129 weeks from January 1995 through

the week of the

budget accord; dividend1 = a categorical variable that equals one if firm i paid a dividend within the

prior year; week = a categorical variable that equals one if the budget accord occurred in

week I;

S&P5OO, = Standard & Poor's 500 index if firm i and week I, else zero; and dividendyield1 = firm i's

dividend yield.

Reaction to Capital Gains Tax Changes

83

dividend yields for the dividend categorical variable and examines ordy

dividend-paying stocks. The regression coefficient on the dividend

yield is significantly negative, indicating that current dividend yields

are correlated with stock-price performance during the budget recon-

ciliation week. The coefficient estimate is 0.29, indicating that a

one-percentage-point decrease in the dividend yield results in a 0.29-

percentage-point larger stock price increase on the announcement of

the budget agreement.

In short, LS infer from their findings that equity price responses to the

1997 announcement of a reduction in the capital gains tax rate cut were

decreasing in dividend yields. Contrary to some predictions, however,

they find no evidence of a market slump driven by a reduction in the

compensation for capital gains taxes that selling shareholders demand

from buyers. Evaluation of returns throughout the summer of 1997 fails

to find evidence of downward price pressure from selling shareholders.

5.2 Summary of Sinai and Gyourko (1999) (SG)

SG examine the same issue as LS, but with different firms and a different

perspective. They test whether buyers compensate sellers for the capital

gains taxes generated by sales. They examine the stock returns of pur-

chasers of real estate to assess whether TRA 97 changed the compensa-

tion that buyers provide sellers.

SC conduct their study by examining equity real estate investment

trusts (REITs), publicly-traded companies that own and operate real

estate. Umbrella partnership REITs (UPREITs) are similar to other REITs,

except that sellers of real estate to UPREITS can avoid immediate capital

gains taxation if they are paid in UPREIT equity interests rather than

cash. This nontaxable option is unavailable for traditional REITs. The

distinction between traditional REITS and UPREITs is analogous to the

distinction in the market for corporate control between taxable cash

acquisitions and tax-deferred stock acquisitions.

SC hypothesize that TRA 97's capital gains tax rate reduction bene-

fited traditional REITs more than UPREITs. All individuals selling to

REITS potentially benefit from the rate reduction, while only individuals

selling to UPREITs who receive cash (i.e., do not opt to receive tax-

deferred equity interests) could benefit from the change.

To test the impact of TRA 97, SC evaluate the 1996 and 1997 daily stock

prices for 129 traditional REITs and UPREITs. They predict that UPREITs

that derive their value more from future acquisitions underperformed

compared with similar traditional REITs in 1997. Their research design

enables them to distinguish between performance in the two organiza-

tional forms, between years, and between more and less acquisitive

Number of observations = 258

Adjusted R2 = 0.07

Adapted from Sinai and Gyourko (1999, Table 8). Dependent variable: natural logarithm of the

average share price in September less the natural logarithm of the average share

price in January.

Sample: 129 companies for 1996 and 1997.

LIPREIT is 1 if firm i is an UPREIT; Y1997, is 1 if period t is 1997; acquisition is 1 if firm i's rent-to-

value ratio is below the weighted median for the sample.

firms. Table 3 reports the results from estimating the regression. As

predicted, the regression results are consistent with TRA 97's capital

gains tax rate reduction being more beneficial to traditional REITs than to

UPREITs, conditional on the company's appetite for acquisitions.

A major distinction between SC's and LS's analyses of IRA 97 is the

event period. Unlike LS, who find evidence that prices for

the largest

U.S. companies responded to the capital gains tax cut within one week,

SG are unable to detect a response using a short window. Only when

they investigate long event periods, e.g., January 1997 to September

1997, do they find evidence that the cut affected REIT prices. As the

event period widens, the probability increases that it includes more

of

the period during which information moved prices. However, the proba-

bility also increases that the analysis is contaminated by other factors

that differentially affect traditional REITs and UPREITs.

An explanation for this difference in the studies is that LS's setting

provides more power. In their primary test, LS examine 239,296 firm

week price changes, while SG are limited to 258 firmyear price changes.

In addition, LS examine the largest, more widely traded, presumably

more efficiently priced U.S. equities, while SG evaluate an

unusual orga-

nizational form in a single sector of the economy. Nonetheless, regard-

less of the event period, both studies find evidence that TRA 97's capital

gains tax rate reduction impacted share prices in a predictable direction.

84

Shackelford

TABLE 3

Regression-Coefficient Estimates and Standard Errors(a)

Explanatory

Coefficient

Standard

variab1e11'

estimate

error

Y1997

0.017

0.042

UPREIT

0.067

0.037

acquisition

0.023

0.039

Y1997 x LIPREIT

0.016

0.053

Y1997 X acquisition

0.047

0.055

UPREIT X acquisition

0.009

0.052

Y1997 X UPREIT X acquisition

0.146

0.073

Reaction to Capital Gains Tax Changes

85

5.3 Summary of Guenther (1999)

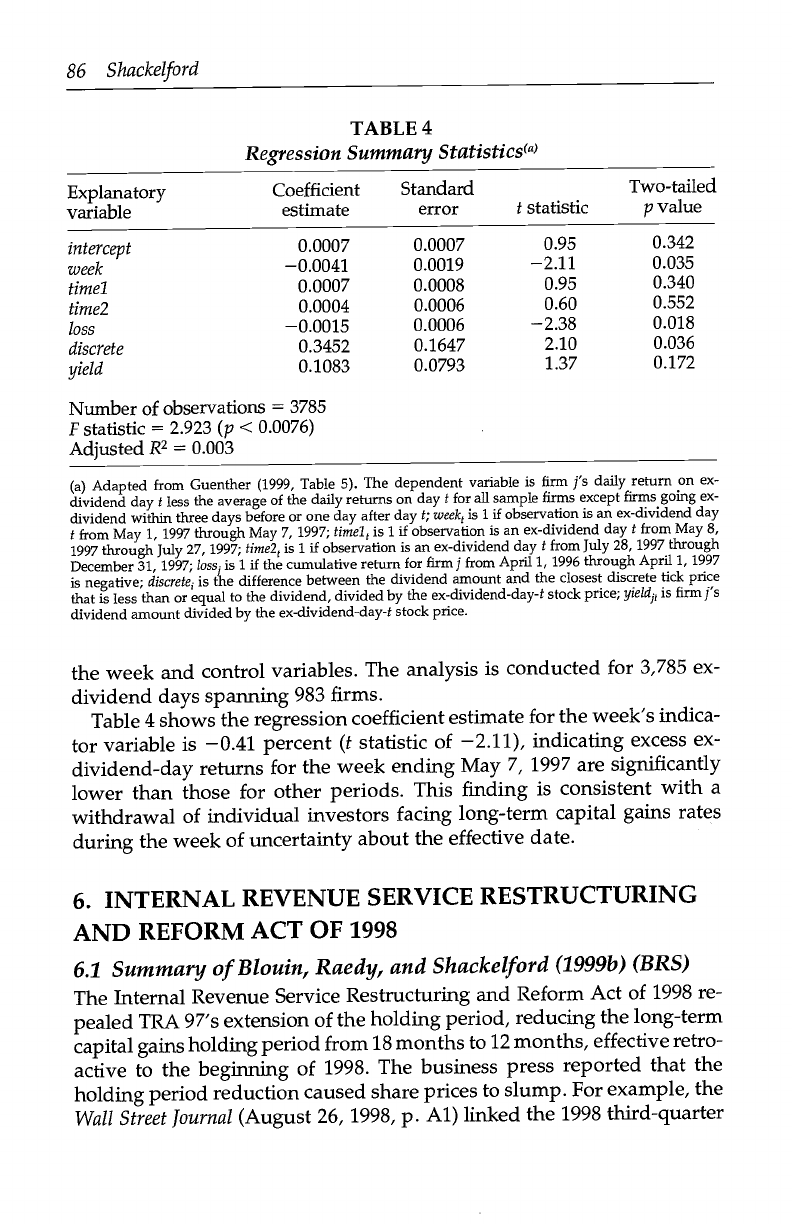

The May 2, 1997 announcement that the President and the Congress had

agreed to reduce the capital gains tax rate did not state

an effective date

for the rate change. The business press reported that individual inves-

tors withdrew from the market to await an effective date. For example,

the Wall Street Journal (May 5, 1997) reported ".

.

. a very noticeable

seller's strike." It quoted David Shulman, chief equity strategist at Salo-

mon Brothers in New York, stating, "'I would suspect that as long as

the effective date is in limbo, we would see delays in selling.' The worst

thing Washington can do is 'to let this thing drag on' without details.

'Then you create economic uncertainty, and you can get a bubble

on the

way up. You could stop a whole series of business transactions right

now in their tracks.' " The New York Times added that the reduction

should ". .

. in

the short term, keep investors from selling until they

know what the effective date of the tax cut wifi be." In

response to

purported market paralysis, Senate Finance Chairman Wiffiam Roth and

House Ways and Mean Chairman William Archer jointly announced

May 7, 1997 that the effective date for any capital gains tax cut would be

that day.

Guenther (1999) investigates whether shareholders delayed selling ap-

preciated stock in anticipation of the 1997 reduction in the capital gains

tax rate. He hypothesizes that if individuals withdrew from the market

following the CBO announcement on April 30, 1997, and reentered fol-

lowing the May 7 announcement, then ex-dividend day returns for the

week preceding the May 7, 1997 announcement should have been less

than usual.

Extant studies (e.g., Elton and Gruber, 1970) document that ex-

dividend days are marked by positive stock returns. This is consistent

with individuals selling appreciated shares before the ex-dividend date

at the favorable long-term capital gains tax rate, avoiding tax-disfavored

dividends, and sharing their tax savings (the difference between the

long-term capital gains rate and the ordinary tax rate) with other inves-

tors through upward price adjustments. However, if individuals await

the new reduced rate and withdraw from the market, then no tax

sav-

ings are available to share with remaining investors, eliminating the

typical upward price pressure characterized by ex-dividend day returns.

To test this proposition, Guenther compares ex-dividend-day excess

returns for the week ending May 7, 1997 (the day of the announcement

of the effective date) with ex-dividend-day returns for the rest of 1997.

Analyzing dividend-paying companies only, a pooled, cross-sectional,

time-series model regresses excess returns on a categorical variable for

86

Shackelford

Number of observations = 3785

F statistic = 2.923 (p < 0.0076)

Adjusted R2 = 0.003

TABLE 4

Regression Summary Statistics(a)

(a) Adapted from Guenther (1999, Table 5). The dependent variable is firm j's

daily return on ex-

dividend day t less the average of the daily returns on day t for all sample firms except firms going ex-

dividend within three days before or one day after day t; week is 1 if observation is an

ex-dividend day

from May 1, 1997 through May 7, 1997; time1 is 1 if observation is an ex-dividend day t

from May 8,

1997 through July 27, 1997; time2 is 1 if observation is an ex-dividend day t from July 28, 1997

through

December 31, 1997; loss is 1 if the cumulative return for firm) from April 1, 1996 through

April 1, 1997

is negative; discrete is the difference between the dividend amount and the closest

discrete tick price

that is less than or equal to the dividend, divided by the ex-dividend-day-t stock price; yieId1 is

firm )'s

dividend amount divided by the ex-dividend-day-t stock price.

the week and control variables. The analysis is conducted for 3,785 ex-

dividend days spanning 983 firms.

Table 4 shows the regression coefficient estimate for the week's indica-

tor variable is 0.41 percent (t statistic of 2.11),

indicating excess ex-

dividend-day returns for the week ending May 7, 1997 are significantly

lower than those for other periods. This finding is consistent

with a

withdrawal of individual investors facing long-term capital gains rates

during the week of uncertainty about the effective date.

6. INTERNAL REVENUE SERVICE

RESTRUCTURING

AND REFORM ACT OF 1998

6.1 Summary of Blouin, Raedy, and Shackelford

(1999b) (BRS)

The Internal Revenue Service Restructuring and Reform Act

of 1998 re-

pealed TRA 97's extension of the holding period, reducing the

long-term

capital gains holding period from 18 months to 12 months, effective retro-

active to the beginning of 1998. The business press

reported that the

holding period reduction caused share prices to slump. For

example, the

Wall Street Journal (August 26, 1998, p. Al) linked the 1998

third-quarter

Explanatory

variable

Coefficient

estimate

Standard

error

t statistic

Two-tailed

p value

intercept

0.0007

0.0007

0.95

0.342

week

0.0041

0.0019

2.11

0.035

timeTl

0.0007

0.0008

0.95

0.340

time2

0.0004

0.0006

0.60

0.552

loss

0.0015

0.0006

2.38

0.018

discrete

0.3452

0.1647

2.10

0.036

yield

0.1083

0.0793

1.37

0.172

Reaction to Capital Gains Tax Changes

87

stock market decline to selling pressure created by the reduction in the

holding period. Marshall Front of Trees Front Associates observed "a

much greater willingness" to sell among clients whose investments quali-

fied for long-term capital gains under a 12-month holding period, but

not

under an 18-month period. Terry Banet, a vice president and portfolio

manager at J.P. Morgan, cited the reduction in the holding period as

"accelerat[ing] the sale of many of the positions" in stocks that qualified

for long-term capital gains under the reduced holding period.

BRS test whether sell-offs, such as those implied by the Wall Street

Journal, can be detected using conventional capital markets event study

methodology. To maximize the power of their tests, BRS focus

on the

returns of initial public offerings. IPOs offer three advantages: (1) indi-

vidual holdings are disproportionately large for IPOs, (2) the beginning

of the holding period for shareholders who bought at the fF0 is observ-

able, and (3) the tax basis for those shareholders is measurable (Reese,

1998). To concentrate on IPOs for which the long-term capital gains

tax

policy is most relevant, BLS limit the analysis to IPOs that have appreci-

ated since listing.

BRS's treatment group are IPOs whose initial public shareholders

met

the 12-month period, but not the 18-month period. The control

group

includes those same IPOs outside the event period and other IPOs

whose listing occurred from 6 to 12 months earlier and from 18

to 24

months earlier. The sample includes 823 IPOs from 1996, 1997, and 1998.

Specifying precisely the period during which the market received infor-

mation about the reduction in the holding period is difficult. Neither the

House of Representatives' nor the Senate's original bill contained

any

capital gains provisions. On June 24, 1998, the conference committee,

following closed sessions, produced the first bifi eliminating the 18-

month holding period.

However, information potentially leaked to the market at least three

times before the conference committee released its report. First, acting

seemingly independently of the tax-bill deliberations, the House Budget

Committee on June 5, 1998 issued its budget resolution for the fiscal

year

beginning October 1, 1998. The resolution assumed elimination of the

18-month holding period. Second, ten days later, on June 15, 1998,

Senate Majority Leader Trent Lott expressed disappointment that the

tax

bifi (then under consideration in the closed conference committee) did

not eliminate the 18-month holding period for long-term capital gains.

Third, the following day, House Speaker Newt Gingrich predicted that

in September 1998 the tax committees would construct

a bifi eliminating

the 18-month holding period. Because the event period cannot be speci-

fied precisely, BRS report the results for multiple event periods.

88

Shackelford

To test the effects of the holding-period reduction,

BRS regress daily

stock returns on categorical variables that indicate whether the IPO's

initial shareholders were affected by the change and that indicate the days

included in the event period. The key variable is an interaction of the two

indicator variables. The coefficient on the interaction indicates the mean

daily percentage difference in returns between the treatment and control

IPOs. BRS interpret a negative coefficient on the interaction as

evidence

that the treatment IPOs underperformed during the event

period.

Table 5 presents results using various event periods. The coefficient

on the interaction is most

significantly different from zero (0.05 level

TABLE 5

Regression Summary Statistics1

Regression model("): returns1 = I3o + J3 midJPO1 (1 + info) +

"Significant at the 5-percent level, one-tailed test.

'Significant at the LU-percent level, one-tailed test.

Adapted from Blouhi, Raedy, and Shackelford (1999b, Table

regressions.

Sample: 61,968 daily returns from 1996, 1997, and 1998 Initial

daily stock return for day t; inidJPO = categorical variable that

more than year, but no more than 18 months, before day t; info =

If day t is during the event period.

4. Adjusted R2 is 9 percent for all

public offerings. ret urns, = firm i's

equals one if firm i's IPO occurred

categorical variable than equals one

Test Period

Variables

midJPO

midJPO X info

Coefficient

statistic

Coefficient

()

statistic

Maximum t statistic

6/17-6/24

0.018

0.49

_0.292**

-1.71

Full period

6/5-7/

0.002

0.04

0.010

0.13

3 days beginning with

budget report

6/5-6/9

0.014

0.37

-0.202

-1.19

Budget to conference

6/5-6/24

0.021

0.54

_0.149*

-1.30

Lott comment to

conference

6/14-6/24

0.017

0.45

_0.198*

-1.33

AP report and

conference bifi

6/23-6/24

0.007

0.19

-0.166

-0.57

Conference report

6/24

0.008

0.21

-0.433

-1.05

Postconference

6/25-7/8

-0.009

-0.23

0.147

1.15

Reaction to Capital Gains Tax Changes

89

using a one-tailed test) for the period June 17, 1998 (the day following

Speaker Gingrich's prediction) to June 24, 1998 (the day the conference

committee released its bifi and one day after press reports that the hold-

ing period would revert to 12 months). The estimate implies that

over

the six days, IPOs with initial public shareholders affected by the hold-

ing period underperformed by a mean daily return of 0.29 percent.

No other subperiods find significance at conventional levels. No evi-

dence is produced consistent with the Wall Street Journal anecdote that

prices were falling in the third quarter in response to the holding period

change. The findings suggest that whatever price response occurred had

been completed by the beginning of the third quarter.

7. INFERENCES FROM TRA 97 AND

IRSRRA 98 STUDIES

As discussed above, the conditions under which TRA 97 and IRSRRA 98

modified capital gains tax policy provide unusually powerful settings for

estimating relations between share prices and capital gains taxes. The

four studies summarized above likely represent the first of many analy-

ses of the 1997 and 1998 legislation that wifi advance our understanding

of the effects of capital gains tax changes on stock prices. Together these

studies provide at least four initial inferences that may be useful as

Congress continues to revisit the appropriateness and level of capital

gains taxation.

One, capital gains tax changes affect stock prices. Although each

study analyzes a different sector of the stock market, all present evi-

dence that share prices responded to the 1997 and 1998 legislation. The

findings imply that the seven necessary conditions for capital gains taxes

to affect share prices, outlined above, held during enactment of TRA 97

and IRSRRA 98. This suggests that, at least during these tax changes,

individuals were the marginal shareholders for some firms.

Two, the stock market responds quickly to information about tax legis-

lation. Notwithstanding SG's inability to detect a response using a short

window (which is likely attributed to insufficient power), LS and BRS

show that the price response is completed within days. These studies

find no evidence of continuing tax effects, such as suggested by the Wall

Street Journal's link between the 1998 legislation and stock market

reac-

tions weeks later.

Three, much of the market reaction has been completed when changes

are publicly announced. For example, LS find prices moving before the

May 2, 1997 budget accord, and BRS find share-price adjustments had

completed their shift by the release of the conference committee's report.

90

Shackelford

Price movement preceding public release of information is consistent with

the adage that Wall Street "buys on the rumor and sells on the news."

Investors trading initially on the "news" (e.g., budget accord announce-

ment or the committee conference's release) would have missed much

of

the price reaction.

Four, the estimated stock-price responses to capital gains tax changes

are of economic significance. Consider the

annualized returns from the

estimates in these studies. LS's estimates suggest that during the accord

week, non-dividend-paying stocks outperformed other stocks by 350

percent using raw returns or 225 percent using risk-adjusted regression

estimates. Guenther's estimates show that excess returns on ex-divi-

dend days are normally 100 percent greater on an annual basis than

those experienced around the rate change. BRS's estimates imply the

holding-period change depressed the share prices of IPOs with affected

initial public shareholders by 75 percent on an annual basis. SG's re-

sults do not permit the same annualized translation; however, their

estimates imply that the capital gains rate reduction was borne fully by

acquisitive UPREITs.

Compare these estimates with the American Council for Capital For-

mation (ACCF)'s widely reported testimony to the House Ways and

Means Committee on June 23, 1999. Citing Wyss (1999), the ACCF stated

that the 1997 rate reduction accounted for one-quarter of the market's

subsequent 30-percent appreciation. During the week of the budget ac-

cord alone, LS find non-dividend-paying stocks outperformed dividend-

paying firms by nearly 7 percent. Thus, LS report an incremental boost

to non-dividend-paying stocks in one week that was almost as large as

the two-year increase that the ACCF trumpeted as evidence that the

stock market benefited from the 1997 rate reduction.

8. CLOSING REMARKS

In summary, the Taxpayer Relief Act of 1997 and the Internal Revenue

Service Restructuring and Reform Act of 1998 provide a useful setting for

reevaluating the effect of capital gains taxation on equity prices. Besides

their being the first change in capital gains tax policy in over a decade, the

market appears to have impounded information from both bills quickly,

enabling recalibration of the effect of capital gains taxes on share prices.

In general, the evidence in the initial studies of the 1997 and 1998

legislation suggests that the incentives provided by favorable long-term

capital gains taxation affect stock prices. Despite at least seven different

conditions that must hold for capital gains tax policy to affect share values,

the findings consistently show that stock prices capitalize capital gains

Reaction to Capital Gains Tax Changes

91

taxes. The stock market response to capital gains tax changes appears

rapid, complete by public announcement of the change, and material.

The results in these studies should interest tax and valuation scholars

and be useful to policymakers as they revise capital gains tax policy.

They contribute to a emerging literatureempirical (e.g., Guenther and

Willenborg, 1999; Blouin, Raedy, and Shackelford, 1999a; Poterba and

Weinsbrenner, 1998; Reese, 1998; Erickson, 1998; Landsman and Shackel-

ford, 1995; Amoako-Adu et al., 1992; Hayn, 1989) and theoretical (e.g.,

Klein, 1999; Collins and Kemsley, 1999; Shackelford and Verrecchia,

1999; Balcer and Judd, 1987)linking stock market reactions to capital

gains tax policy. The findings provide additional evidence that in at least

some situations the marginal investor is an individual whose marginal

tax rate changes when stocks cross from short-term to long-term classifi-

cation. He invests shares for the requisite holding period, intends to sell

in a taxable disposition, and complies with the capital gains tax law. His

expectation of the applicable tax rate when he sells in the future is

altered by the capital gains tax change, and supply inelasticities appar-

ently prevent immediate economic readjustment. Together these papers

raise doubts about prior assumptions that capital gains tax policy is of

little relevance for equity price formation.

REFERENCES

Amoako-Adu, B., M. Rashid, and M. Stebbins (1992). "Capital Gains Tax and

Equity Values: Empirical Test of Stock Price Reaction to the Introduction and

Reduction of Capital Gains Tax Exemption." Journal of Banking and Finance

16:275-287.

Balcer, Y., and K. Judd (1987). "Effects of Capital Gains Taxation on Life-Cycle

Investment and Portfolio Management." Journal of Finance 42:743-758.

Blouin, J., J. Raedy, and D. Shackelford (1999a). "Is the Marginal Shareholder an

Individual? Capital Gains Taxes and Stock Reactions to Public Disclosures."

Chapel Hill, NC: University of North Carolina. Working Paper.

(1999b). "Stock Prices and Capital Gains Taxes: Evidence from the 1998

Reduction in the Long-Term Capital Gains Holding Period." Chapel Hill, NC:

University of North Carolina. Working Paper.

Collins, J., and D. Kemsley (1999). "Capital Gains and Dividend Taxes in Firm

Valuation and Corporate Financial Policy." Chapel Hill, NC: University of

North Carolina. Working Paper.

Constantinides, G. (1983). "Capital Market Equilibrium with Personal Tax."

Econometrica 51(May): 611-636.

(1984). "Optimal Stock Trading with Personal Taxes: Implications for

Prices and the Abnormal January Returns." Journal of Financial Economics

13:65-89.

Dhaliwhal, D., and R. Trezevant (1993). "Capital Gains and Turn-of-the-Year

Stock Price Pressures." Advances in Quantitative Analysis of Finance and Account-

ing 2:139-154.

92

Shackelford

Elton, E., and M. Gruber (1970). "Marginal Stockholder Tax Rates and the Clien-

tele Effect." Review of Economics and Statistics 52:68-74.

Erickson, M. (1998). "The Effect of Taxes on the Structure of Corporate Acquisi-

tions." Journal of Accounting Research 36:279-298.

Guenther, D. (1999). "Investor Reaction to Anticipated 1997 Capital Gains Tax

Rate Reduction. Boulder, CO: University of Colorado. Working Paper.

Gunther, D., and M. Willenborg (1999). "Capital Gains Tax Rates and the Cost of

Capital for Small Business: Evidence from the IPO Market." Journal of Financial

Economics 53(3):385-408.

Hayn, C. (1989). "Tax Attributes as Determinants of Shareholder Gains in Corpo-

rate Acquisitions." Journal of Financial Economics 23:121-153.

Klein, P. (1999). "The Capital Gain Lock-in Effect and Equilibrium Returns."

Journal of Public Economics 71(3):355-378.

Landsman, W., and D. Shackelford (1995). "The Lock-in Effect of Capital Gains

Taxes: Evidence from the RJR Nabisco Leveraged Buyout." National Tax Journal

48:245-259.

Landsman, W., D. Shackelford, and R. Yetman (1999). "The Determinants of

Capital Gains Tax Compliance: Evidence from the RJR Nabisco Leveraged

Buyout." Chapel Hill, NC: University of North Carolina. Working Paper.

Lang, M., and D. Shackelford (2000). "Capitalization of Capital Gains Taxes:

Evidence from Stock Price Reactions to the 1997 Tax Reductions." Forthcoming

Journal of Public Economics.

Miller, M., and M. Scholes (1982). "Dividends and Taxes: Some Empirical Evi-

dence." Journal of Political Economy 90:1118-1141.

Poterba, J. (1987a). "How Burdensome Are Capital Gains Taxes?" Journal of Public

Economics 33:157-172.

(198Th). "Tax Evasion and Capital Gains Taxation." American Economic

Review 77(no. 2):234-239.

Poterba, J., and S. Weisbrenner (1998). "Capital Gains Tax Rules, Tax Loss

Trading, and Turn-of-the-Year Returns." Cambridge, MA: National Bureau of

Economic Research. Working Paper.

Reese, W. (1998). "Capital Gains Taxation and Stock Market Activity: Evidence

from IPOs." Journal of Finance 53:1799-1820.

Scholes, M., and M. Wolfson (1992). Taxes and Business Strategy: A Planning

Approach. Englewood Cliffs, NJ: Prentice-Hall.

Shackelford, D. (2000). "The Tax Environment Facing the Wealthy." Forthcom-

ing in Does Atlas Shrug? The Economic Consequences of Taxing the Rich, J. Slemrod

(ed.). Cambridge, MA: Harvard University and the Russell Sage Foundation.

Shackelford, D., and R. Verrecchia (1999). "Intertemporal Tax Discontinuities."

Chapel Hill, NC: University of North Carolina. Working Paper.

Sinai, T., and J. Gyourko (1999). "The Asset Price Incidence of Capital Gains

Taxes: Evidence from the Real Estate Industry and the Taxpayer Relief Act of

1997." Philadelphia: University of Pennsylvania. Working Paper.

Stiglitz, J. (1983). "Some Aspects of the Taxation of Capital Gains." Journal of

Public Economics 21(July):257-294.

Thompson, T. (1987). "1979 Individual Income Tax Capital Gains Income Report-

ing Noncompliance." In Trend Analyses and Related Statistics: 1987 Update. Wash-

ington: U.S. Department of the Treasury, Internal Revenue Service.

Wyss, D. (1999). "Capital Gains Taxes and the Economy: A Retrospective Look."

Lexington, MA: Standard & Poor's DRI. Working Paper.