Summer 2023

CHEMICAL INSIGHTS

Current State of Chemicals and Materials M&A

Over the past quarter, news headlines have seemed skewed even more negative than usual: recessionary concerns, supply chain

disruptions, banking liquidity, inflation, rising interest rates, geopolitical uncertainty & conflicts, debt ceiling showdowns, and more.

Much has been written about these macroeconomic events, and we can concisely summarize them with a simple, obvious statement

– there is significant uncertainty in the market. That being said, buyers and sellers are successfully navigating the current

environment, and transactions are getting done. In this Summer 2023 newsletter, we share real-time insights from industry leaders

on the pricing and volume dynamics rippling through the industry. Importantly, we highlight what these dynamics mean for M&A.

Also, to preview upcoming publications from the Grace Matthews team, be on the lookout for an ‘Industry Highlights’ series, where

we will dive into various sectors across the chemical and material science value chain. Up next: a focus on composites.

Chemicals & Materials Industry Update: Volume Declines, Price Increases & the Impact on M&A

Outside of pure strategic acquisitions where products, technologies, markets, facility overlap, or other true synergistic factors are

dominant, financial trends and outlook are the primary value and buyer interest determinants. In the current environment, volume

headwinds have been at the forefront of M&A discussions. Are these driven by customers destocking material after months of

inventory building? Is it demand softness in core end markets? Is it a combination of both? What do volume trends mean for

pricing? When will the headwinds end?

In order to gain a better understanding of these trends and their impact on M&A, we did some digging. At Grace Matthews, we

track performance of ~100 public chemicals and materials companies in the Grace Matthews Index (see page 4 for 10-year EV/

EBITDA chart). We recently sampled the Q1 2023 earnings transcripts for 20 industry leaders spanning multiple sectors – from

commodity chemicals to specialty materials. It is no surprise that volume trends were a key focus across nearly all of the earnings

calls we reviewed. In 16 of those transcripts, industry executives referenced significant volume declines – in many cases, executives

noted double-digit percentage declines relative to last year. You’ll see excerpts from these transcripts scattered throughout this

publication. Interestingly, nearly all pointed to robust pricing largely offsetting revenue lost from volume declines. Furthermore,

companies seem to have more success maintaining price increases than in prior years given increased “stickiness” of their customer

base, reshuffling of global supply chains and higher service levels. We recognize that trends and drivers likely vary significantly

across the chemicals value chain. What we found interesting though were the similarities in both the challenges faced and the

strategies utilized to counter recent volume declines, regardless of end market or vertical. In other words, this is a universal theme in

that it spans the entire chemical value chain.

Grace Matthews Chemical Insights

1

Summer 2023

In light of these trends, the key question we are asked by clients is, “How does this impact the M&A process?” Let’s first revisit events

of the past two years:

Supply gets tight (2021-2022): Starting with COVID-19 and the subsequent Texas freeze, supply chain challenges became the norm.

This was compounded by a labor shortage, reshaping of the European energy market, and more cautious views on China, all of

which led to further squeezing of supply chains. It was commonplace for materials to be in limited supply (allocations were

common), and pricing in many cases spiked to all-time highs. Despite the increased cost, the reaction by many was to increase

inventory on hand to secure supply and attempt to pass through any price increases to customers. It was a bit of the wild west in

terms of stockpiling materials, and we often heard clients note “if we could get more inventory…we could sell it.” As companies

were faced with these challenges, elevated purchasing became typical, as executives valued stable supply to customers over

working capital efficiencies. It is no surprise that this strategy was frequently referenced in transcripts by multinational public

companies:

Patrick Joseph Winterlich (Executive VP, CFO & Acting Corporate Controller of Hexcel): “We deliberately allowed our

inventory to grow, recognizing some of the supply chain challenges and bringing in the materials. And we did that in order

to make sure that we didn't delay or impact our customers…”

Supply chain easing (H2 2022 – Current): In late 2022, as customers started transitioning away from excess stocking strategies,

suppliers began to anticipate declines in their sales volumes. Significant destocking occurred as companies found themselves

holding elevated levels of (and in many cases, high-priced) inventory. While it isn’t possible to quantify the exact impact and timing

of destocking throughout the value chain, the dynamic was very real (and in some cases, is still ongoing). This exacerbated inventory

management issues for many companies, as they had to deal with customers reducing or delaying orders to resolve their own

overstocking issues.

Macroeconomic events certainly didn’t help the outlook, raising concerns of subdued demand moving forward. While demand and

outlook vary by sector, demand softness remains a large concern among industry executives.

Matthias Zachert (CEO & Chairman of the Board of Management of Lanxess): “We get feedback from customers that they

are still living from inventories that they built up in course of 2021, 2022 when supply chains were disrupted...”

Robert Patterson (CEO, Chairman & President of Avient): “From a destocking standpoint, it seems like many customers really

still feel like they've got a lot of inventory on hand. I know some of that's anecdotal. I can't tell you what percentage of

customers that is, but we certainly hear that routinely.”

Luis Rojo (Vice President and Chief Financial Officer at Stepan): “What you saw in Q1 was, we are still depleting high-cost

raw materials that we have in the system…And we believe we're going to need at least Q2 to finish the depletion of some of

these materials…”

Andrew Tometich (CEO, President & Director of Quaker): “Volumes continue to be impacted by a continuation of softer end

market conditions, primarily in the steel and industrial markets…We continue to see softer end market activity across all

regions and at varying degrees.”

Christian Kullmann (CEO & Chairman of the Executive Board of Evonik): “We do have a broad-based weak demand, which

is combined with continued destocking across most of our businesses...”

Ilham Kadri (CEO, Chairman of the Executive Committee & Non-Independent Director of Solvay): In February, “We shared

some insights on our early view of the first quarter, including our expectation that volumes would decline in a weak macro

demand environment as destocking effect from quarter 4 would linger into the first half of the year. We also said that pricing

would offset the volume decline, and we were confident in our team's ability to sustain profitability and margins. And this is

exactly what happened.”

It is impossible to separate the impact of destocking and soft demand on total volume declines, but one thing is clear – both would

generally be a value detractor in a sale process. However, in most instances, pricing power has remained strong and bolstered

financial performance across the industry. Inflationary pressures and corresponding margin enhancing strategies have driven price

increases over the past year; these increases generally held and currently are helping to mitigate the impact of volume declines.

Additionally, increased raw material availability is leading to lower raw material prices (for some products) and providing additional

bottom-line cushion from volume declines.

The outlook for pricing and volume trends is uncertain, and several key questions remain for the future: when will customers work

through inventory stockpiles, how will end market demand trend, and when will prices return to “normal levels”, if ever. While most

Grace Matthews Chemical Insights

2

Summer 2023

executives indicate that volume declines are ongoing, it does seem that demand softness and destocking may be starting to abate

in some markets. A review of all 20 transcripts suggests that the exact timing for destocking normalizing and/or increased end

market activity varies by sector (no surprise). While some companies saw easing in late 2022/early 2023, others are just now seeing

easing.

Albert Yuan Chao (CEO, President & Director of Westlake): “Results reflect significant improvement in volumes, margins and

earnings from the fourth quarter of 2022 as customer destocking activity moderated, end market demand improved...”

James Fitterling (CEO & Chairman of DOW): “While we expect near-term conditions to remain challenging through the

year, we continue to see positive underlying demand trends driving above GDP growth across our attractive market verticals

over the next few years...”

Timothy Knavish (CEO, President & Director of PPG): “…as availability of raw materials returns to pre-pandemic levels, we

expect our earnings to start benefiting from moderate deflation from recent historic inflation highs. As a reminder,

aggregate raw material inflation since early 2021 remains at historically high levels… the high-level statement is, we expect

to continue to see moderation as we move through the year…but hard to quantify the scale of that at this point because

there's still so many moving parts...”

Let’s now revisit the question: “How is this impacting a potential M&A process right now?” M&A deal volumes are down across the

global market; however, certain sectors and deal sizes have remained resilient. In particular, deals in the lower middle market (less

than roughly $30M in EBITDA) remain active as they are less dependent on financing sources that may be restricted in the current

capital market environment. Additionally, the chemical sector is viewed as resilient long-term – its products and services are critical

to the global economy and investors generally recognize that long-term success outweighs short-term volatility.

On a more granular level, we wanted to share a few noteworthy M&A takeaways in the wake of recent trends.

1. Flight to Quality: The ability to achieve continued performance in today’s environment is a differentiator for businesses. As

a result, companies that can demonstrate strong performance, particularly as it relates to volume growth, are receiving

outsized market attention, as companies with a resilient business model are coveted in the current environment. Our recent

transactions have demonstrated this flight to quality.

2. Expect Increased Scrutiny During Diligence: More than in past years, we see buyers digging in on the quality of revenue,

volume and margin trends, with an emphasis on sustainability of current performance. Given heightened scrutiny on

granular performance drivers – buyers are often looking in-depth at customer and SKU-level trends – pre-process

preparation is as important as ever (see point #3).

3. Upfront Work to Quantify “Sustainable” Performance is Key: Trailing 12-month EBITDA is a key variable in M&A processes,

as it is widely viewed as one of the best metrics for gauging run-rate or sustainable performance. Given current market

variability, buyers are heavily scrutinizing near-term performance for acquisition targets. Doing the work to quantify go-

forward performance and craft a defensible story to support outlook ahead of a transaction process is critical. In periods of

strong economic activity, crafting a story is less important. However, given current economic uncertainty, the upfront work

we do to position our clients is critical, and we leverage the industry experience we’ve developed over the last 25 years to

most efficiently structure an opportunity for success.

4. Timing: In many instances, sellers may benefit from waiting to launch a sale process, allowing the company to demonstrate

continued performance (e.g., adding a quarter to demonstrate that price increases have taken hold and are sustainable, or

to demonstrate that a poor quarter of volume declines are a temporary blip due to destocking). We have shared this advice

with many clients over the past year, and suggest we use the extra time to work together to prepare for a sale process and

ensure the company is ready when we click “GO”. Pre-process preparation is critical (again, see point #3) and the timing for

a launch doesn’t inhibit important work ahead of time.

Because Grace Matthews is privately held, we are not dependent on transactions closing in a given quarter or year in order

to meet internal financial forecasts. As a matter of policy, we believe that what’s best for our clients is best for our firm –

sometimes, that means waiting to start a process until market conditions or business fundamentals are in the “right” place.

Performance trends are at the forefront of every conversation right now. How long the current dynamics will persist is hard to say,

but we know volume declines and price increases are having a material impact on the industry. These trends are driving an

emphasis on well-performing assets and leading to increased buyer scrutiny during financial diligence. If you are considering a

transaction, pre-process preparation is as important as ever. Doing the up-front work to “prove out” a story of sustainable

performance and growth is critical.

Grace Matthews Chemical Insights

3

Summer 2023

Grace Matthews Chemical Index: Enterprise Value / EBITDA (Last 10 Years)

Source: Grace Matthews and Capital IQ

The Grace Matthews Chemical Index tracks the Enterprise Value / EBITDA ratios (“EV / EBITDA multiples" or "EBITDA multiples") of

95 publicly traded chemical companies that span multiple sub-sectors and geographies. The Index aggregates the latest reported

financial data and stock prices, and tracks valuation trends and operating metrics across different industry sectors. Index averages

are equally weighted, as opposed to weighting by market capitalization.

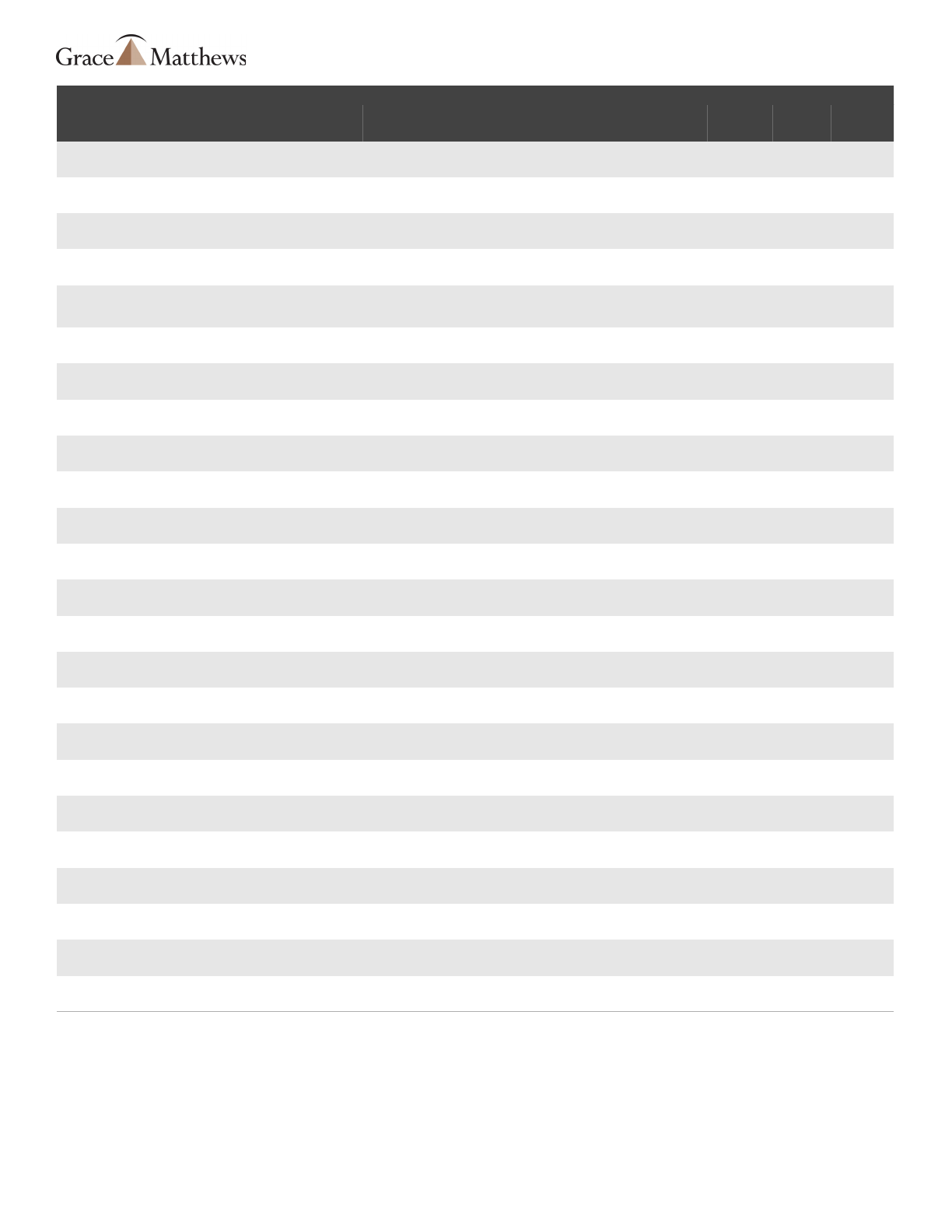

Select Industry Transactions

Transaction values in $US millions

Closed

Date

Acquirer / Target

Target Description

Enterprise

Value (EV)

EV /

Sales

EV /

EBITDA

Pending

Apollo Global Management / Univar

Solutions

Global chemical and ingredients distributor and provider of value-

added services

$8,165

0.7x

8.7x

Pending

Exponent Private Equity / IFF (Flavor

Specialty Ingredients Division)

Manufacturer of synthetic and natural aroma chemicals

$220

Pending

Gemini Coatings / Rudd Company

Manufacturer of wood coatings, stains, and finishes

Pending

Azelis / Gillco Ingredients

Distributor of ingredients, including antimicrobials, antioxidants,

chocolates, cocoa powder, among others

Pending

Akzo Nobel / Sherwin-Williams (China Paints

Division)

Chinese decorative paints division

Pending

International Chemical Investors Group

(ICIG) / Evonik (Cyanuric Chloride Division)

Cyanuric chloride division

Pending

LyondellBasell / Quality Circular Polymers

(QCP)

Develops circular polypropylene copolymers and polyethylene

compounds

Pending

Arkema / Polytec PT

Develops, manufactures, and distributes specialty adhesives

Pending

Fujifilm / Entegris (Electronics Chemicals

Division)

Manufactures, formulates, and distributes specialty chemicals and

performance materials

Pending

LyondellBasell / Mepol Group

Manufactures recycled and technical compounds

Pending

Solenis / Diversey

Provider of hygiene, infection prevention, and cleaning solutions

$4,516

1.6x

14.6x

Grace Matthews Chemical Insights

4

Current (as of May 2023): 10.1x

10 Year Average (as of May 2023): 11.0x

Enterprise Value / EBITDA

Summer 2023

Pending

IMCD / CPS Oil-Tech

Distributor of specialty chemicals to the petroleum, additive,

grease manufacturing and other industry related segments

Pending

Univar Solutions / Kale Kimya

Specialty chemicals distributor headquartered in Turkey

$143

May-23

Cinven Group / MBCC Group (Admixtures

Division)

Manufacturer of concrete admixtures, as well as other sustainable

solutions for the construction industry

May-23

Aimia / Bozzetto Group

Producer of textile, building, and performance chemicals

$244

1.0x

7.1x

May-23

H.B. Fuller / Beardow Adams

Manufactures hot melt adhesives for bookbinding, labeling,

packaging, and other applications

May-23

Foremark Performance Chemicals / NexGen

Chemical Technologies

Provider of consulting services and customized chemical solutions

to oil and gas industries

May-23

Canlak Coatings / Ceram-Traz

Develops and manufactures coatings and products for metal,

concrete, and wood markets

Apr-23

Harbour Group / Americo Chemical

Products

Provider of custom-blended chemical products for metal

fabrication, coil coating, plating, and wastewater treatment

Apr-23

AMSOIL / Benz Oil

Produces and sells lubricants and solutions for various industrial

applications

Apr-23

IMCD / ACM

Distributor of minerals and chemicals

Apr-23

Audax Private Equity / Krayden

Distributor of adhesives, sealants, coatings, soldering materials,

cleaners, and solvents

Mar-23

Hasa / Orenda Technologies

Manufactures and supplies specialty pool chemicals

Mar-23

Vertellus / Centauri Technologies

Manufactures specialty chemicals

Mar-23

Avery Dennison / Thermopatch

Manufactures heat seal machines, labels, direct imprint

equipment, mending material, and marking devices

$44

1.1x

Mar-23

RelaDyne / Allied Oil & Supply

Distributor of lubricant & lubricant related products

Mar-23

Stahl / ICP Group (Industrial Solutions

Division)

Offers a comprehensive portfolio of high-performance coatings

used primarily in packaging and labeling applications

$205

1.5x

Mar-23

RelaDyne / Sun Coast Resources

Distributor of fuels and lubricants

Mar-23

Corteva / The Stoller Group

Develops and distributes biologicals and crop health products

$1,200

12.0x

Feb-23

Archroma / Huntsman Corporation (Textile

Effects Division)

Manufactures dyes, chemicals and digital inks for the textile and

related industries

$718

0.9x

7.6x

Feb-23

Surteco / Synthomer (Laminates, Films and

Coated Fabrics Division)

Producer of laminates, foils and vinyl-coated fabrics for functional

and decorative surfaces

$255

1.0x

8.0x

Feb-23

ESCO Technologies / CMT Materials

Develops, manufactures, and supplies syntactic foam and other

tooling materials for the thermoforming industry

$18

1.2x

Jan-23

Grafe Polymer Solutions / Color Technik

Manufactures polymer-specific color and additive masterbatches

for thermoplastic materials and color compounds

Jan-23

Shrieve Chemical Company / Chem One

Distributor of industrial chemicals

Jan-23

Wind Point Partners / Hasa

Manufactures and distributes chemicals and ancillary products

used for critical sanitization and maintenance of water systems

Transaction values in $US millions

Closed

Date

Acquirer / Target

Target Description

Enterprise

Value (EV)

EV /

Sales

EV /

EBITDA

Grace Matthews Chemical Insights

5

Note: For transactions in which a less than 100% stake is acquired, enterprise value represents the implied EV as if a 100% stake were acquired. Enterprise values also

include contingent consideration.

Summer 2023

Grace Matthews: Select Chemical and Material Science Transactions!

Grace Matthews Chemical Insights

6

has sold its Menomonee Falls,

WI-based aerosol manufacturing

facility and related business to

has been recapitalized by

has been acquired by

has been acquired by

has been acquired by

has acquired the !

Industrial Solutions Group of

has been acquired by

has been acquired by H.I.G.

Capital's portfolio company

has sold its Colorado and !

New Mexico store locations to

has been acquired by

through its subsidiary, GEO

Specialty Chemicals, has sold

its DMPA business to

has acquired the kaolin !

minerals business of

through its subsidiary, Evans

Chemetics, has sold its

Thioester Business to!

has sold certain assets to!

!

!

has been recapitalized by

has been acquired by

a portfolio company of !

Audax Private Equity has been

acquired by"

Grace Matthews Client Listed First

has been acquired by Wind Point

Partners' portfolio company

has been acquired by Renovo

Capital and its portfolio company

has been acquired by

Summer 2023

Grace Matthews Overview

Grace Matthews is recognized globally as a leader in transaction advisory services for manufacturers and distributors throughout the

chemical and material science value chain. Grace Matthews’ clients include privately held businesses, private equity funds, and

large, multinational corporations.

Grace Matthews' practice is global in scope, and focuses on several areas: sell-side transactions and divestitures for private

companies, private equity holdings, and multinational corporations; buy-side work for large public companies, major multinationals,

and sponsor-backed platforms; leveraged transactions and recapitalizations, strategic advisory analysis, and transaction fairness

opinions. Areas of expertise include:

• Adhesives, Sealants, Tapes

• Catalysts, Petrochemicals

• Colorants, Additives

• Construction Chemicals, Building Products

• Contract Manufacturing, Custom Synthesis

• Distribution, Equipment, Infrastructure

• Environmental Services

• High Purity, Electronic Chemicals

• Industrial Minerals, Inorganic Chemicals

• Ingredients, Nutraceuticals, Flavors, Fragrances

• Intermediates, Industrial Chemicals

• Life Sciences

• Lubricants, Greases, Metalworking Fluids

• Oilfield & Water Treatment Chemicals

• Paints, Coatings, Inks

• Personal Care, Soaps, Medical Materials

• Plastics, Composites, Molded Materials

• Tolling, Private Label Products

• Additional Chemical Sectors

Grace Matthews is a privately held investment bank with successful chemical and material science industry transactions dating back

to the early 1990s. Grace Matthews principals have completed over 200 transactions involving global corporations. Our team

approach is unique in investment banking, with a combination of extensive industrial, financial and M&A experience."

"

"

Contact Our Team

John Beagle Kevin Yttre Ben Scharff

Chairman, Co-Founder President, Managing Director Managing Director

jbeagle@gracematthews.com kyttre@gracematthews.com bscharff@gracematthews.com

Andy Hinz Doug Mitman Bridget Spaulding

Managing Director Co-Founder, Senior Advisor CFO

Jon Glapa Andrew Cardona Eric Sabelhaus

Director Director Director

Tom Osborne Michelle Tveten Chris Hayes

Senior Executive Marketing Director Associate

Matt Stouder Kyle Tamboli Jack Chandler

Associate Associate Senior Analyst

Drew Gebhardt Jordan Boswell Gabby Caranto

Analyst Analyst Analyst

Katie Long Headquarters

Office Manager 833 East Michigan Avenue

Milwaukee, WI 53202

414.278.1120

Grace Matthews Chemical Insights

7

Summer 2023

www.gracematthews.com

Grace Matthews, Inc. (www.gracematthews.com) is an investment banking group providing merger, acquisition, and corporate finance advisory services for chemical companies both in the U.S. and

internationally. Grace Matthews is global in scope and well known for its strong track record of success dating back to the early 1990s.

The information and views contained in this report were prepared by Grace Matthews, Inc. It is not a research report, as such term is defined by applicable law and regulations, and is provided for

information purposes only. No part of this material may be copied or duplicated in any form or by any means, or redistributed, without Grace Matthews’ prior written consent.

Copyright (c) 2023 Grace Matthews, Inc. All rights reserved. Securities are offered through GM Securities, LLC, which is indirectly owned by Grace Matthews, Inc., and a registered broker dealer and

member of the Financial Industry Regulatory Authority and Securities Investor Protection Corporation. Check the background of this firm on FINRA's BrokerCheck.

Grace Matthews Chemical Insights

8